Eli Lilly and Company has officially claimed the top spot among global pharmaceutical companies by revenue, a monumental achievement underscored by its recent financial performance. This ascent coincides with a groundbreaking regulatory success: the U.S. Food and Drug Administration (FDA) on April 1 granted approval for Foundayo (orforglipron), Lilly’s innovative once-daily oral GLP-1 receptor agonist for obesity. Foundayo represents a significant advancement as the first oral small molecule GLP-1 approved for weight management, and its expedited review process, completed in a mere 50 days, marks it as the fastest new molecular entity approval since 2002. Despite these dual triumphs – a historic revenue milestone and a landmark approval – the market’s reaction has been surprisingly subdued, with Lilly’s stock experiencing a notable decline of nearly 14% since January 1. This perplexing divergence between corporate success and investor sentiment highlights the complex dynamics at play within the highly scrutinized pharmaceutical sector, particularly concerning the burgeoning and fiercely competitive GLP-1 market.

Lilly’s Ascendancy to Pharmaceutical Leadership

Lilly’s climb to the summit of the pharmaceutical industry is a testament to its strategic focus and robust pipeline execution, particularly within the metabolic disease landscape. For the fiscal year 2025, the Indianapolis-based pharmaceutical giant reported a staggering $65.18 billion in revenue, marking an impressive 44.7% year-over-year growth. This unprecedented growth rate not only secured its position as the fastest-growing among the top 20 pharmaceutical companies but also propelled it past long-standing industry titans.

The company’s financial results painted a clear picture of its new market dominance. Merck & Co., a formidable competitor, reported FY2025 revenue of $65.01 billion, with a modest 1.3% growth. Pfizer, once a pandemic-era revenue leader, posted $62.58 billion, experiencing a 1.7% decline. AbbVie followed with $61.16 billion, growing at 8.6%, and Johnson & Johnson recorded $60.40 billion, with a 5.8% increase. While the revenue margin separating Lilly from Merck was a tight $170 million, the stark difference in growth rates – Lilly’s 44.7% versus Merck’s 1.3% – underscores the profound shift in the competitive landscape and Lilly’s aggressive market penetration.

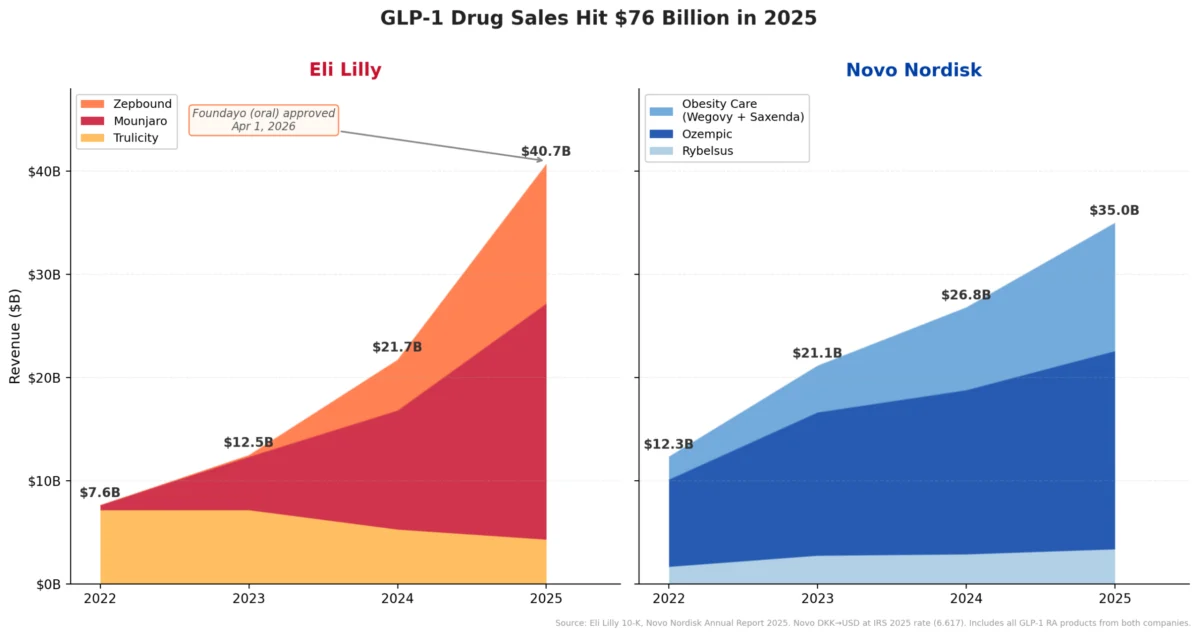

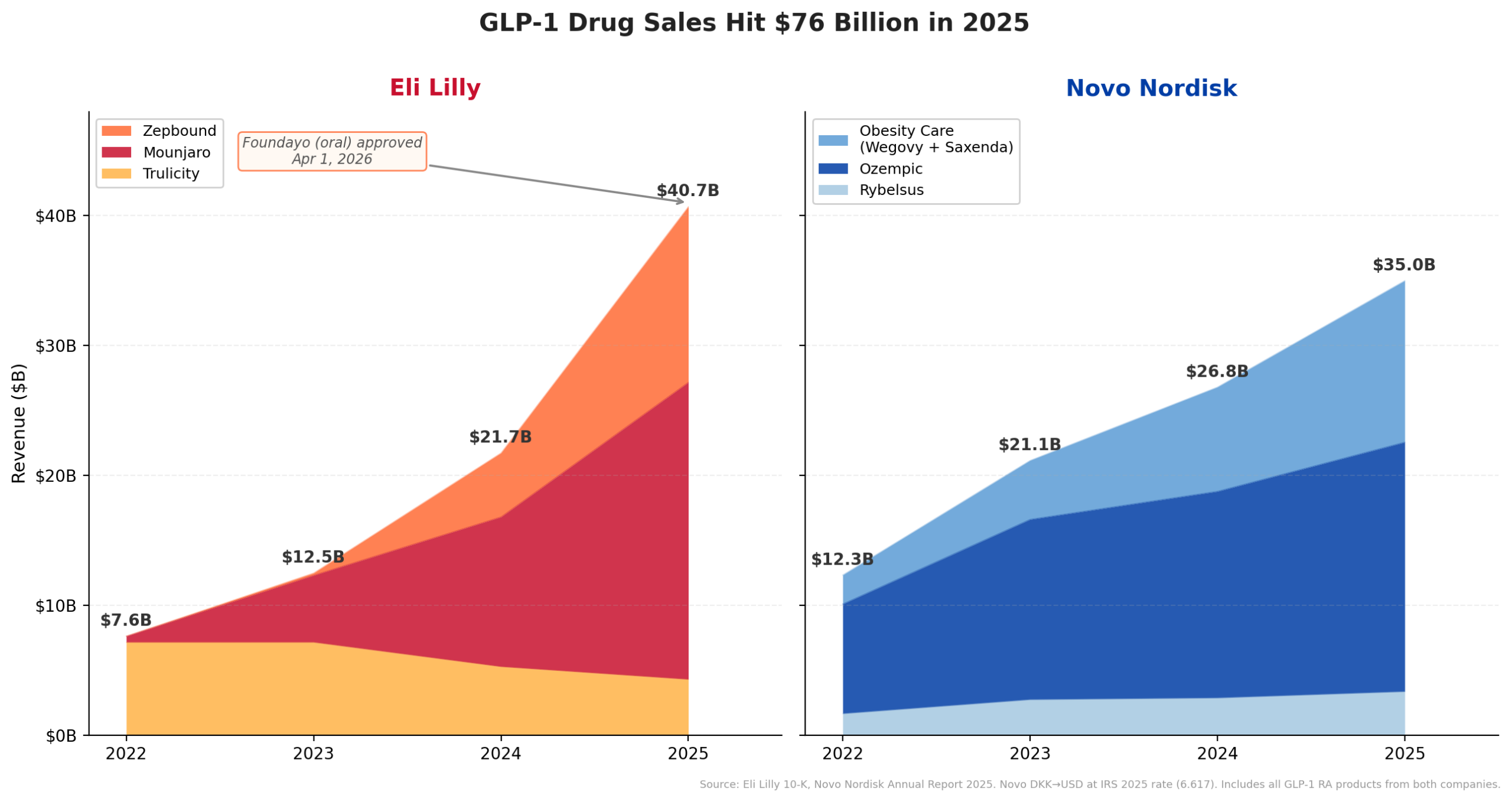

This financial surge is overwhelmingly attributed to the extraordinary performance of its glucagon-like peptide-1 (GLP-1) receptor agonist portfolio. Injectable GLP-1s have been the primary engine of Lilly’s growth. Mounjaro (tirzepatide), a dual GLP-1 and glucose-dependent insulinotropic polypeptide (GIP) receptor agonist, generated an astounding $9.0 billion in revenue in the first half of 2025 alone, demonstrating a remarkable 90% year-over-year increase. Its obesity-specific counterpart, Zepbound (tirzepatide), which was only launched in late 2023 and is now widely available in a convenient multi-dose KwikPen, contributed an additional $5.7 billion in H1 2025. Cumulatively, Lilly’s GLP-1 assets are on track to exceed an annualized revenue of $30 billion, solidifying their status as blockbuster drugs and the cornerstone of the company’s financial success.

The GLP-1 market itself has undergone a seismic expansion, evolving from a market valued under $12 billion in 2022 to an annualized run rate of approximately $65 billion by mid-2025. This rapid growth is fueled by the escalating global obesity epidemic and the increasing recognition of GLP-1s as highly effective pharmacological interventions for weight management and type 2 diabetes. These drugs mimic the action of natural gut hormones, promoting satiety, slowing gastric emptying, and improving insulin secretion, leading to significant weight loss and glycemic control.

Foundayo: A New Chapter in Oral Obesity Treatment

The approval of Foundayo (orforglipron) marks a pivotal moment in the treatment of obesity, offering a novel oral therapeutic option in a market predominantly dominated by injectable formulations. The FDA’s decision to approve Foundayo on April 1 came with remarkable speed, facilitated by its clearance under the Commissioner’s National Priority Voucher program. This program is designed to incentivize the development of drugs for serious and unmet medical needs, and its application resulted in Foundayo’s approval just 50 days after its filing, nearly 10 months ahead of its scheduled review date. This expedited process highlights the FDA’s recognition of the urgent need for accessible and effective obesity treatments.

Until recently, the landscape of blockbuster GLP-1s, including Novo Nordisk’s Ozempic and Wegovy, and Lilly’s Mounjaro and Zepbound, has been almost exclusively injectable, with the exception of Novo Nordisk’s Rybelsus (oral semaglutide for type 2 diabetes). While Novo Nordisk did receive approval for an oral version of Wegovy (also semaglutide) in December 2025 for obesity, Foundayo presents a distinct advantage. Novo Nordisk’s oral Wegovy is a peptide formulation that necessitates specific administration conditions, requiring patients to take it on an empty stomach with restricted water intake, which can be a barrier to adherence for some.

Foundayo, in contrast, is a small molecule GLP-1 receptor agonist. This chemical structure provides significant flexibility, allowing it to be taken at any time of day, with or without food or water restrictions. This ease of administration is a critical differentiator, potentially enhancing patient compliance and broadening the appeal of oral GLP-1 therapy. Lilly CEO Dave Ricks articulated this strategic positioning, noting that while Foundayo is "not more effective" than the company’s injectable Zepbound, it is "more accessible" and "easier to fit into your daily routine."

Clinical trials, specifically the ATTAIN-1 studies, demonstrated that patients receiving the highest dose of orforglipron achieved an average body weight loss of 12.4% over 72 weeks. While this is a clinically significant outcome, it is generally less than the 20%-plus weight loss typically observed with injectable tirzepatide (Zepbound). However, Ricks framed Foundayo not as a direct competitor to Zepbound, but as a complementary offering within Lilly’s diverse portfolio. His statement, "We want people to be on the medicine that meets their health goals. If it has Lilly on the box, that’s the goal we have," underscores the company’s strategy to capture various segments of the obesity market by offering a range of options tailored to different patient preferences and clinical needs. The ability of an oral option to significantly expand the addressable population for obesity treatment is substantial, considering the global prevalence of needle aversion and the desire for convenient dosing. Recognizing this potential, Lilly has already submitted orforglipron for approval in over 40 countries, signaling its global ambitions for this novel therapy. The drug’s journey began with Lilly licensing orforglipron from Japanese drugmaker Chugai in 2018 for an upfront payment of $50 million, a strategic investment that has now culminated in a landmark approval.

The Wall Street Conundrum: Analyzing Investor Sentiment

The juxtaposition of Lilly’s unprecedented revenue growth and a groundbreaking drug approval with a significant decline in its stock price presents a complex narrative for investors. The nearly 14% drop in Lilly’s stock since January 1, following a period of meteoric rises, indicates a cautious, if not skeptical, stance from Wall Street. Several factors likely contribute to this phenomenon, often described as "buy the rumor, sell the news."

Firstly, Valuation Concerns are paramount. Lilly’s stock had experienced an extraordinary rally leading up to these announcements, largely driven by the immense anticipation and projected sales for its GLP-1 portfolio. Many analysts and investors might have already "priced in" the success of Mounjaro and Zepbound, as well as the expected approval of oral GLP-1s. Consequently, the actual approval, while positive, might not have offered new information to justify further upward movement, leading to profit-taking.

Secondly, the intensifying Competitive Landscape within the GLP-1 market cannot be overlooked. While Lilly and Novo Nordisk currently dominate, a host of other pharmaceutical companies are aggressively pursuing their own GLP-1 programs and alternative weight-loss mechanisms. The market’s long-term growth potential is immense, but so is the potential for increased competition, which could exert pressure on pricing and market share. Investors may be factoring in the future dilution of Lilly’s dominant position as more players enter the fray.

Thirdly, Foundayo’s Efficacy Profile compared to its injectable counterparts might be a point of concern. While its convenience is a major advantage, the lower average weight loss (12.4% vs. 20%+) could limit its appeal for patients seeking maximum efficacy. Investors might question whether Foundayo will truly expand the market significantly enough or if it will primarily appeal to a niche segment, potentially cannibalizing some of Lilly’s higher-efficacy (and likely higher-priced) injectable sales. The balance between accessibility and efficacy will be crucial for its commercial success and market perception.

Fourthly, Pricing and Reimbursement Pressures are an ever-present concern in the pharmaceutical industry. As more oral GLP-1 options become available, payers (insurance companies and government health programs) may seek to negotiate lower prices, especially for drugs with less dramatic weight loss outcomes. The high cost of GLP-1 therapies is already a significant point of discussion, and the introduction of more accessible options might intensify this debate, potentially impacting future revenue streams.

Finally, there are Supply Chain and Manufacturing Challenges. The unprecedented demand for GLP-1 drugs has already led to intermittent shortages. Scaling up production for another high-demand product like Foundayo, particularly an oral formulation with its own manufacturing complexities, could present logistical hurdles. Investors might be wary of Lilly’s ability to consistently meet demand, which could impact sales forecasts and patient access.

Broader Impact and Future Outlook

The approval of Foundayo and Lilly’s ascent to the top revenue spot carry profound implications for the pharmaceutical industry, public health, and the future of obesity management.

Expanding Patient Access and Market Reach: The introduction of an oral small molecule GLP-1 like Foundayo is a game-changer for patient accessibility. A significant portion of the population is averse to injectable medications, creating a barrier to treatment even when highly effective options exist. Foundayo’s convenient oral dosing removes this barrier, potentially enabling millions more individuals to access effective weight management therapy. This expansion could dramatically increase the total addressable market for GLP-1s, driving further growth in a sector already experiencing explosive demand. Lilly’s global regulatory submissions for orforglipron in over 40 countries further underscore its commitment to making this accessible option available worldwide.

Shifting Competitive Dynamics: While Lilly and Novo Nordisk currently hold a near duopoly in the GLP-1 market, the emergence of differentiated oral options will intensify competition. Foundayo’s unique small molecule profile and flexible dosing regimen offer a distinct advantage over peptide-based oral GLP-1s. This innovation will likely spur other pharmaceutical companies to accelerate their own oral GLP-1 development programs, potentially leading to a more diverse and competitive market with a wider range of options for patients. This competitive pressure could ultimately drive innovation, improve drug profiles, and potentially influence pricing strategies.

Transformative Impact on Public Health: The global obesity epidemic poses one of the most significant public health challenges of our time, contributing to a host of chronic conditions including type 2 diabetes, cardiovascular disease, and certain cancers. Highly effective and accessible treatments like Foundayo have the potential to transform the management of obesity, moving it beyond traditional diet and exercise alone. By offering a convenient pharmacological option, healthcare providers can better address the complex physiological aspects of weight management, leading to improved health outcomes for millions. This shift will, however, also necessitate ongoing discussions about healthcare infrastructure, insurance coverage, and public education to ensure equitable access and appropriate utilization of these powerful new therapies.

Lilly’s Strategic Dominance: With a robust portfolio that includes both the leading injectable dual agonist (Zepbound/Mounjaro) and a pioneering oral small molecule GLP-1 (Foundayo), Eli Lilly has solidified an unparalleled strategic position in the metabolic disease space. This comprehensive approach allows the company to cater to a broad spectrum of patient needs and preferences, from those seeking maximal efficacy with injectables to those prioritizing convenience with oral medications. This diversified portfolio reduces the risk associated with over-reliance on a single product or delivery method, providing a strong foundation for sustained long-term growth and market leadership.

In conclusion, Eli Lilly’s current standing is a testament to its audacious innovation and strategic foresight, culminating in both the highest revenue in the pharmaceutical industry and the approval of a groundbreaking oral GLP-1 for obesity. The paradox of these monumental successes being met with a declining stock price reflects the intricate interplay of high valuation, market expectations, competitive pressures, and investor psychology that defines the modern pharmaceutical landscape. While short-term market reactions may be complex, the long-term implications of Lilly’s strategic moves, particularly in expanding access to effective obesity treatments, are undeniably profound for both the company’s future trajectory and global public health.

Leave a Reply