On May 12, 2025, a significant executive order signed by then-US President Donald Trump mandated the US Department of Health and Human Services (HHS) to pursue Most Favored Nation (MFN) pricing for prescription medicines. This policy fundamentally aimed to align US drug prices with those in select comparator countries through International Reference Pricing (IRP). The framework proposed three distinct IRP models: GENEROUS (GENErating cost Reductions fOr US Medicaid), GLOBE (Global Benchmark for Efficient Drug Pricing), and GUARD (Guarding US Medicare Against Rising Drug Costs). Each model incorporated a curated basket of international reference markets, with a substantial number of these being European nations. The potential for these US-centric pricing policies to create significant spillover effects in global pharmaceutical markets, particularly in Europe, has become a focal point of analysis.

A comprehensive review of pharmaceutical launch and withdrawal trends across Europe, conducted by GlobalData using its Price Intelligence (POLI) database, reveals a discernible shift in industry behavior in the ten months following the MFN policy’s announcement, compared to the preceding decade. The analysis, which spanned from July 12, 2024, to March 12, 2026, offers early insights into how the MFN policy, with its reliance on European pricing benchmarks, may be influencing the strategic decisions of pharmaceutical manufacturers.

The MFN Policy and its European Nexus

The MFN policy’s core mechanism, International Reference Pricing, operates by pegging US drug prices to the average prices in a defined set of comparator countries. The inclusion of European markets within these reference baskets was a critical component, given the significant market size and influence of the United States in global pharmaceutical pricing. The GENEROUS model, for instance, included Denmark, France, Germany, Italy, Switzerland, and the United Kingdom. The GLOBE and GUARD models expanded this scope, referencing a broader array of 14 European nations, including Austria, Belgium, the Czech Republic, Denmark, France, Germany, Ireland, the Netherlands, Norway, Spain, Sweden, Switzerland, and the United Kingdom. The implicit assumption was that lower prices in these European markets would exert downward pressure on US drug costs. However, this approach inadvertently created a potential disincentive for manufacturers to prioritize or even launch products in these very same European countries, fearing that lower European prices could negatively impact their pricing power and profitability in the lucrative US market.

A Stark Decline in European Pharmaceutical Launches

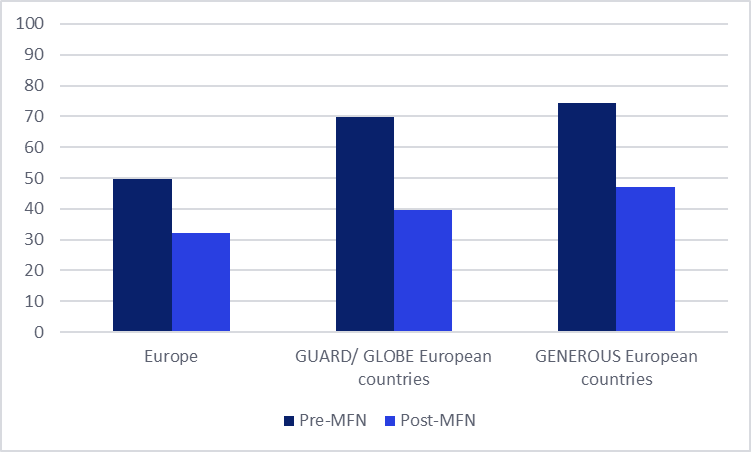

The GlobalData analysis indicates a pronounced contraction in the number of new pharmaceutical product launches across Europe in the ten months subsequent to the MFN policy’s introduction. The overall decline in European launches stood at an significant 35% when comparing the period after the policy’s announcement to the ten months prior. This aggregate figure masks more pronounced trends when examining countries specifically included in the US reference pricing baskets.

European markets designated for the GENEROUS model experienced a reduction in launches of 37%. More striking was the trend observed in the wider European countries referenced by the GLOBE and GUARD models. In these markets, which collectively represent a substantial portion of the European pharmaceutical landscape, the average number of launches saw a substantial decline of 43% in the post-MFN announcement period.

While acknowledging that numerous factors contribute to pharmaceutical launch rates—including regulatory approval timelines, complex pricing and reimbursement negotiations, clinical trial outcomes, and supply chain logistics—the observed trend presents a compelling early signal. This sharp decrease suggests that the MFN policy’s pricing mechanism is already acting as a deterrent. Pharmaceutical companies, faced with the prospect of lower prices in benchmarked European markets potentially influencing US pricing, appear to be strategically delaying or reconsidering their launch sequences. This cautious approach is further exacerbated by reports of US biotech firms becoming hesitant to enter into licensing agreements with European partners, fearing inadvertent triggers of MFN provisions that could erode their pricing power in the United States. The resulting uncertainty is likely a significant driver behind the observed strategic delays in European market entry.

Figure 1: Average Number of Innovative Medicines Launches Within Europe Before and After MFN Executive Order Announcement

(Insert Figure 1 visualization here, showing a clear downward trend in launches post-MFN announcement, with distinct bars for overall Europe, GENEROUS model countries, and GLOBE/GUARD model countries.)

Source: GlobalData, Price Intelligence (POLI) database.

Escalating Product Withdrawals Across the Continent

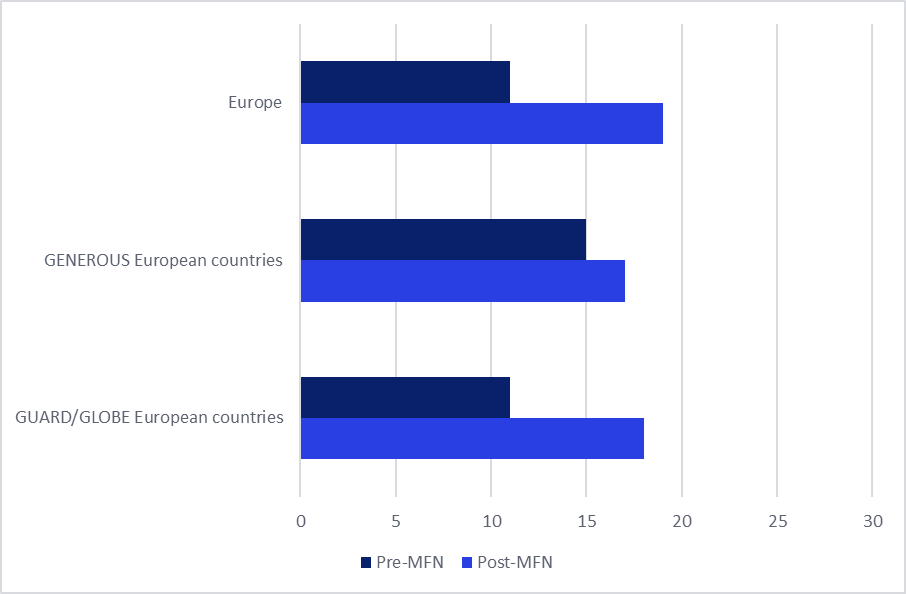

In parallel with the slowdown in new product introductions, GlobalData’s data reveals a significant uptick in the withdrawal rates of branded medicines across Europe. In the ten months following the MFN executive order, the number of pharmaceutical brands experiencing at least one pack withdrawal from the market surged by 43% across the continent.

This pattern is not uniform, with variations observed across different reference baskets. The core European countries within the GENEROUS basket saw a more moderate 10% increase in withdrawals. However, European markets listed in the GLOBE and GUARD model baskets experienced a more substantial 40% rise in withdrawal rates. This divergence suggests that the broader the inclusion of a European market in the MFN reference baskets, the more pronounced the impact on withdrawal activity.

The observed increase in withdrawal rates is logically consistent with the pressures imposed by the MFN pricing framework. Manufacturers are confronting a challenging calculus: either maintain market access in lower-priced European territories, where profitability may now be compromised, or safeguard pricing integrity in the lucrative US market. The data suggests that a growing number of companies are prioritizing the latter.

A pertinent example is Amgen’s PCSK9 inhibitor, Repatha (evolocumab), which was recently withdrawn from the Danish pharmaceutical market. Denmark is a country included in all three MFN reference baskets (GENEROUS, GLOBE, and GUARD). This withdrawal is likely linked to the low tender prices available in Denmark, which can create a conflict with a company’s efforts to maintain higher prices outside the US under MFN rules. This specific case may foreshadow a broader trend, where pharmaceutical companies unable to secure favorable pricing in certain European markets may opt for product withdrawal rather than jeopardize their US market pricing strategy under the MFN IRP system.

Furthermore, the evolving policy landscape within Europe itself adds another layer of complexity. Governments across the continent are increasingly focused on controlling pharmaceutical expenditures. For instance, Italy has recently implemented measures to curb rising medical costs and has signaled resistance to higher European drug prices that might be influenced by MFN expectations. This growing divergence between pricing pressures from international policies and national cost-containment objectives could further accelerate medicine withdrawals across Europe.

Figure 2: Average Number of Brand Withdrawals in Europe Before and After MFN Introduction

(Insert Figure 2 visualization here, depicting a clear upward trend in brand withdrawals post-MFN announcement, with comparative bars for overall Europe and specific model countries.)

Source: GlobalData, Price Intelligence (POLI) database.

The Shifting Global Launch Sequence: A US-Centric Trajectory?

While it is still relatively early to draw definitive conclusions about the long-term impact of MFN on product launch sequences, initial observations of products approved in 2025 indicate a continued preference for a US-first launch strategy. Approximately 92% of these products were initially introduced in the United States. Crucially, a staggering 97% of these US-launched products have yet to be introduced in any other market.

For the smaller subset of products that did launch outside the US, primarily in Europe, Germany emerged as the most frequent initial launch market, accounting for 60% of these instances. Notably, all of these products subsequently expanded into additional markets, with the US consistently being among them.

An illustrative example is CSL Group’s Andembry (garadacimab), a novel gene therapy for the rare disease Hereditary Angioedema. Andembry received its initial launch approval in Germany. From there, it expanded to thirteen other markets, with the United States being its fifth launch market. This trajectory suggests a pattern where European markets, particularly Germany, can serve as initial launchpads for products, with subsequent expansion into the US.

Overall, these early launch trends suggest a continuity in the established global launch pattern rather than a radical disruption. However, the observed limited and slower expansion into other markets following an initial US launch could hint at increasing caution among pharmaceutical companies. Whether this increased caution is directly attributable to the MFN policy pressures, or a confluence of other factors, remains to be definitively established.

Figure 3: Launch Sequence of Andembry (garadacimab)

(Insert Figure 3 visualization here, illustrating the chronological order of Andembry’s market launches, highlighting Germany as the initial launch country and the US as a subsequent market.)

Source: GlobalData, Price Intelligence (POLI) database.

Broader Implications and Future Outlook

While the MFN pricing policy was primarily conceived to address the high cost of medicines within the United States, the early trends analyzed by GlobalData suggest potentially far-reaching international consequences, particularly for the European pharmaceutical landscape. The observed reduction in new product launches and the escalating rates of product withdrawals in European markets may signify a strategic recalibration by pharmaceutical companies. This recalibration appears geared towards protecting their pricing power and profitability in the US market, potentially at the expense of timely patient access to new therapies in lower-priced European countries.

The continued US-first launch strategy, as evidenced by the 2025 cohort, coupled with a potentially slower expansion into other global markets, could indicate heightened risk aversion among pharmaceutical manufacturers operating under the shadow of MFN pricing pressures. While these early indicators are significant, it is crucial to emphasize that drawing firm, conclusive judgments at this juncture would be premature. The pharmaceutical market is dynamic, influenced by a multitude of interconnected factors.

The MFN policy’s intended success in moderating US drug prices raises a critical question about its broader impact on global patient access and the overall affordability of medicines. If withdrawal rates and supply chain constraints intensify across Europe, policymakers may face mounting pressure to re-evaluate pricing adjustments to ensure continued and equitable access to essential medications. The complex interplay between international pricing policies, national healthcare budgets, and the imperative of patient access will continue to be a defining challenge for the global pharmaceutical industry in the coming years.

The insights presented in this article are a product of GlobalData’s Price Intelligence (POLI) service, a leading global resource for pharmaceutical pricing, Health Technology Assessment (HTA), and market access intelligence. The POLI service is integrated with GlobalData’s extensive expertise in epidemiology, disease, clinical trials, and manufacturing, offering clients critical early warning signals and in-depth analysis of policy developments and market dynamics worldwide. For further information or to request a demonstration, interested parties are encouraged to contact GlobalData directly.

Leave a Reply