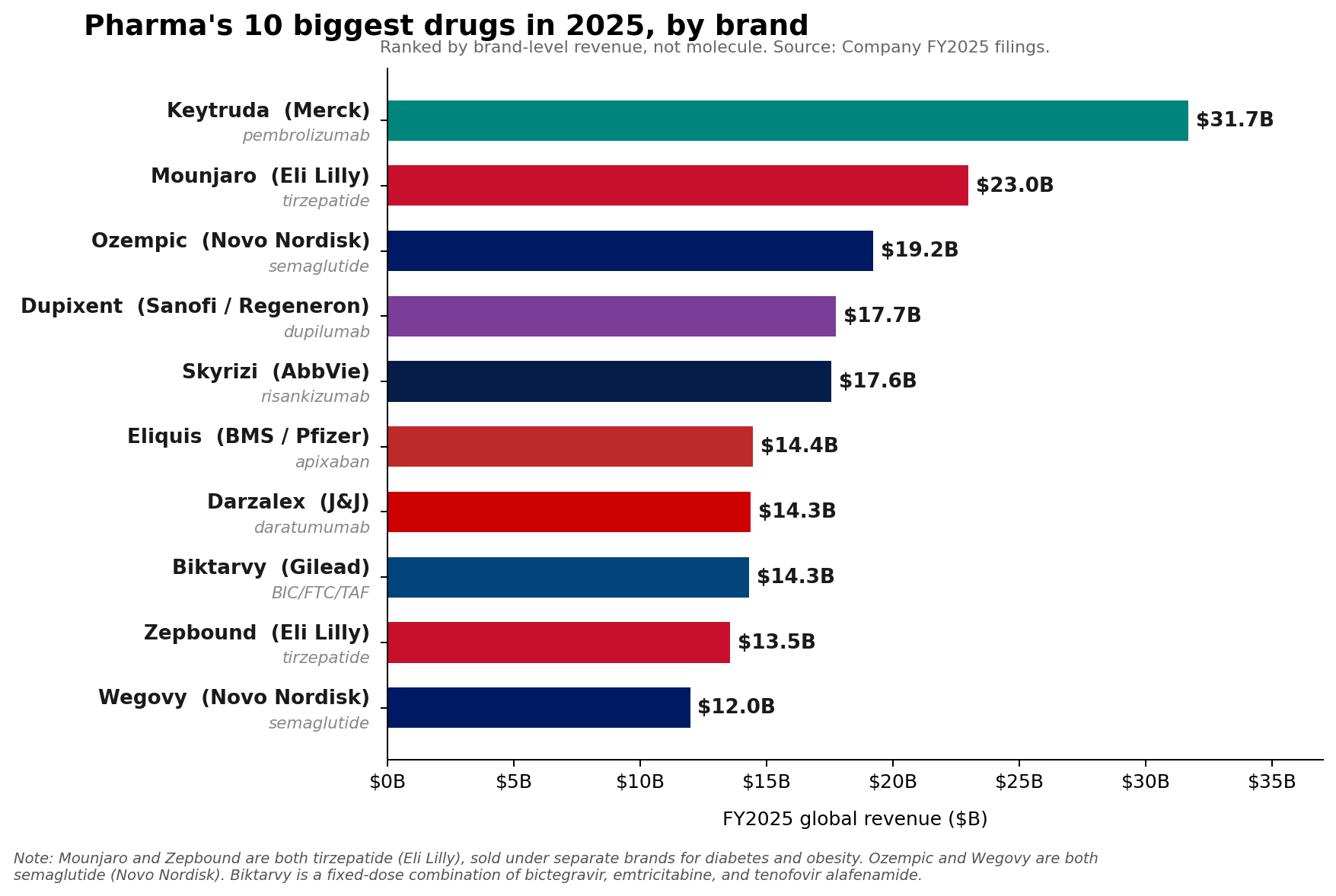

The pharmaceutical industry’s financial landscape is undergoing a significant transformation, marked by the continued brand dominance of Merck’s Keytruda (pembrolizumab) yet a decisive shift in molecular-level leadership towards a new generation of metabolic drugs. In fiscal year 2025, Keytruda, a cornerstone of cancer immunotherapy, maintained its position as the pharmaceutical sector’s top-selling brand, recording an impressive $31.7 billion in sales. However, a deeper look at aggregated molecular sales reveals a seismic shift, with Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide franchises collectively surpassing Keytruda’s revenue, signaling a new era driven by groundbreaking advancements in metabolic health.

The Shifting Sands of Pharmaceutical Supremacy: Keytruda’s Enduring Brand Power

Merck’s Keytruda, an anti-PD-1 therapy, has long been celebrated as a revolutionary treatment across a multitude of cancers. Its sustained growth, achieving a 7% increase in 2025 sales, underscores its critical role in oncology. Since its initial FDA approval in 2014 for advanced melanoma, Keytruda has expanded its indications to include non-small cell lung cancer, head and neck squamous cell carcinoma, classical Hodgkin lymphoma, and many others, establishing itself as a versatile and indispensable tool in the oncologist’s arsenal. This broad applicability, coupled with its efficacy in various treatment settings, has cemented its status as the pharmaceutical industry’s leading brand by individual product. The drug’s robust performance is a testament to Merck’s strategic lifecycle management, including the ongoing development of new indications and the introduction of patient-friendly formulations like subcutaneous Keytruda QLEX, designed to enhance convenience and adherence.

Despite this continued brand strength, the impending loss of exclusivity (LOE) for Keytruda in the coming years casts a long shadow over Merck’s future revenue projections. Patent expiration typically ushers in an era of generic competition, leading to significant price erosion and market share decline. Merck CEO Rob Davis has publicly addressed these concerns, describing the anticipated revenue drop-off as "more of a hill than a cliff," suggesting a managed decline rather than an abrupt collapse. This optimistic outlook likely hinges on the company’s robust pipeline and strategic diversification efforts. However, the market remains cautious; Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion reportedly fell below Wall Street expectations, reflecting investor apprehension regarding the post-Keytruda landscape. The challenge for Merck will be to successfully navigate this transition, leveraging its R&D capabilities to introduce new blockbusters that can offset the eventual decline of its oncology flagship. Historically, companies facing patent cliffs invest heavily in M&A and advanced pipeline assets to maintain growth trajectories. Merck’s strategy is likely to involve both, coupled with maximizing Keytruda’s remaining exclusivity period through new formulations and combination therapies.

GLP-1 Agonists Ascend: A New Era in Metabolic Health

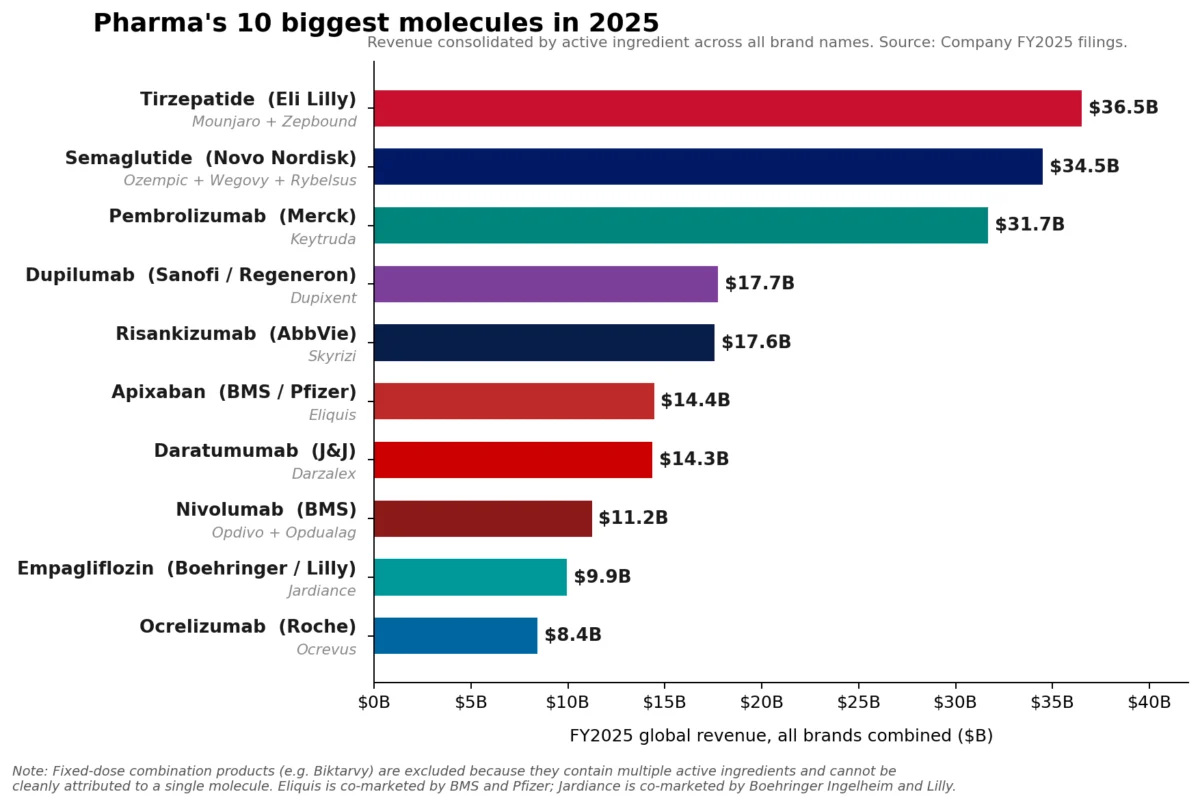

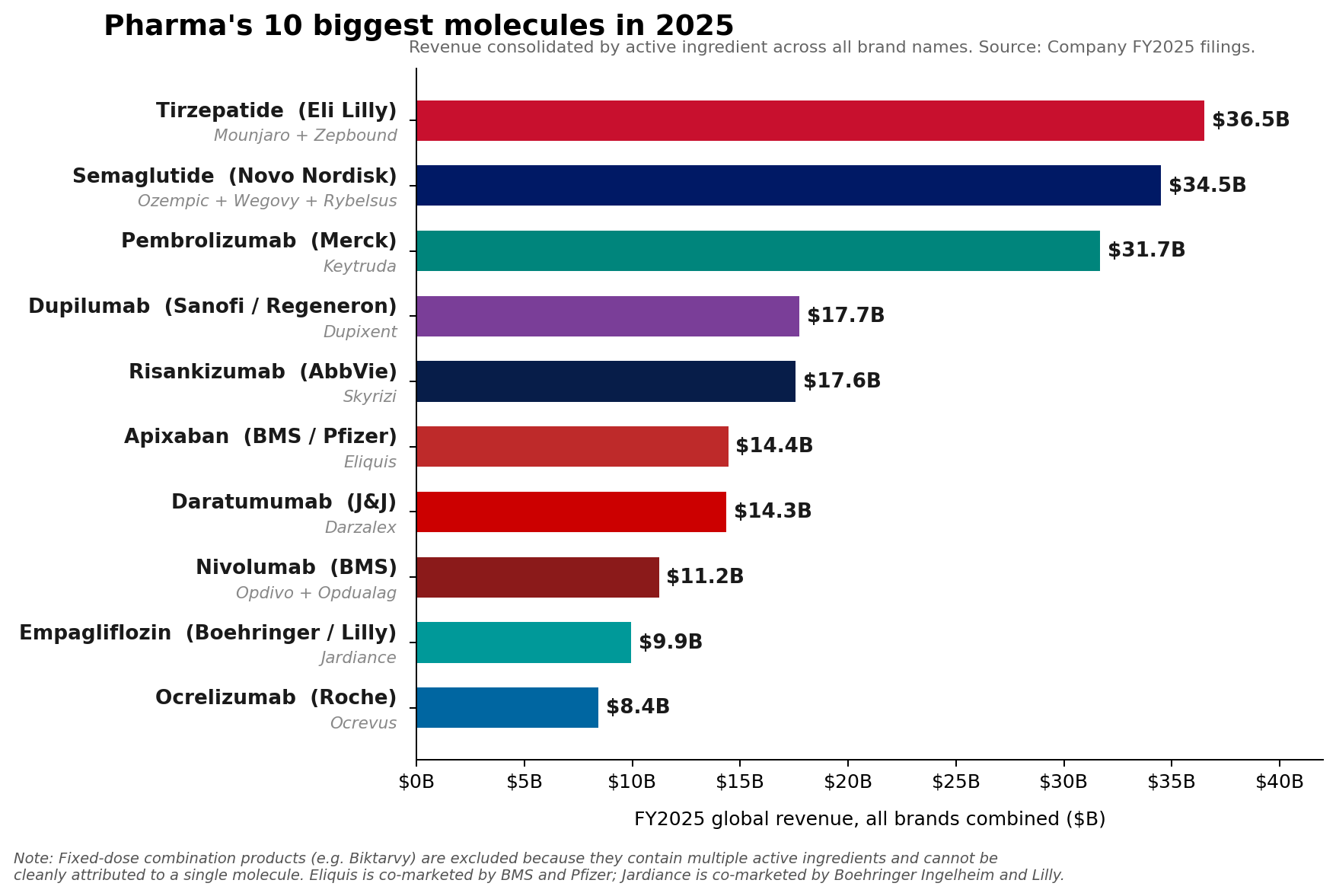

While Keytruda held the brand crown, the aggregated sales of GLP-1 receptor agonists have undeniably claimed the molecular throne. This dramatic shift highlights the immense market potential and rapid adoption of treatments for diabetes and obesity. Eli Lilly’s tirzepatide franchise, comprising the diabetes drug Mounjaro and the weight-loss medication Zepbound, achieved a combined revenue of approximately $36.5 billion in 2025. Mounjaro alone generated $22.965 billion, while Zepbound contributed an additional $13.542 billion. These figures are remarkable, especially considering Zepbound’s relatively recent market entry for obesity.

Similarly, Novo Nordisk’s semaglutide franchise, encompassing the diabetes treatment Ozempic, the weight-loss drug Wegovy, and the oral diabetes medication Rybelsus, collectively reached approximately $34.5 billion in sales. The success of both tirzepatide and semaglutide underscores a paradigm shift in the treatment of metabolic diseases. These drugs, by mimicking the action of glucagon-like peptide-1 (GLP-1), not only regulate blood sugar levels but also significantly promote weight loss, addressing two of the most pervasive and costly public health challenges globally. The unmet need in these therapeutic areas has fueled an unprecedented demand, leading to rapid market expansion and substantial revenue generation for their respective manufacturers.

Oral GLP-1s: The Game-Changer and Its Implications

The competitive landscape in the metabolic health market intensified further with the entry of Lilly’s oral GLP-1 receptor agonist, orforglipron, marketed as Foundayo. Approved by the FDA on April 1, 2026, and commercially available as of April 9, Foundayo represents a significant strategic development. Historically, GLP-1 agonists have primarily been injectable, posing a barrier for some patients due to needle aversion or inconvenience. An oral formulation, taken once daily, has the potential to dramatically expand patient access and adherence, potentially revolutionizing the market.

Analysts, while acknowledging orforglipron’s strategic importance, hold differing views on its immediate financial impact. Lilly’s 2026 revenue guidance of $80 billion to $83 billion was largely driven by the continued strong performance of Mounjaro and Zepbound, which entered 2026 with substantial sales bases ($22.965 billion and $13.542 billion, respectively). Given that Foundayo’s approval occurred after Q1 2026, its revenue contribution will primarily materialize in the latter half of the year. While it may not be the largest absolute dollar-growth engine for Lilly in 2026, its strategic significance is undeniable. It positions Lilly to capture a broader segment of the anti-obesity market, appealing to patients who prefer oral medications.

The broader market for anti-obesity treatments is experiencing explosive growth. According to Citeline’s 2026 Pharma R&D Annual Review, the anti-obesity pipeline surged by a "gut-busting 30.7%" to 588 active compounds, even as the overall pharmaceutical pipeline contracted. This expansion signals intense future competition and underscores the industry’s recognition of the vast commercial opportunity in weight management. Orforglipron’s entry, while behind Lilly’s own established injectables, Mounjaro and Zepbound, adds another powerful tool to the company’s metabolic arsenal and is a harbinger of a more diversified and accessible obesity treatment landscape.

Novo Nordisk is also active in the oral GLP-1 space. While its older oral semaglutide product, Rybelsus, saw a 2% decline at constant exchange rates (CER) in 2025, the company launched the newer Wegovy pill in January 2026. This oral Wegovy, along with plans for broader rollouts and the introduction of new doses (like the 7.2 mg dose in various countries and Wegovy HD in the U.S.), is reflected in Novo Nordisk’s 2026 outlook. However, Novo’s own 2026 guidance anticipates an adjusted sales growth of negative 5% to negative 13% at CER, citing pricing pressure, increasing competition, and U.S. access dynamics. This suggests that while oral semaglutide is strategically vital for market expansion and patient access, it may not immediately translate into significant revenue growth in a fiercely competitive and evolving market.

Beyond Metabolic: Enduring Strength in Immunology and Oncology

Beyond the headline-grabbing performances of Keytruda and the GLP-1 agonists, several other specialty brands demonstrated robust growth, highlighting the sustained strength and innovation within immunology and other areas of oncology. These established franchises continue to compound their value, proving that the pharmaceutical leaderboard is not becoming a "pure GLP-1 monoculture."

AbbVie’s immunology portfolio, in particular, showcased remarkable strength. Skyrizi (risankizumab) reached $17.562 billion in 2025 sales, while Rinvoq (upadacitinib) achieved $8.304 billion. Together, these two drugs generated $25.866 billion in 2025, accounting for approximately 42% of AbbVie’s total net revenue of $61.160 billion for the year. This impressive performance positions AbbVie with a powerful two-drug immunology engine that rivals the scale of the industry’s largest single brands. These treatments for inflammatory conditions like psoriasis, psoriatic arthritis, and rheumatoid arthritis benefit from chronic administration and ongoing unmet needs, ensuring durable revenue streams. AbbVie’s 2026 adjusted EPS guidance of $14.37 to $14.57 reflects confidence in the continued growth of these key assets.

Sanofi’s Dupixent (dupilumab), an innovative biologic for atopic dermatitis, asthma, and chronic rhinosinusitis with nasal polyps, also continued its ascent, rising to €15.714 billion (approximately $17 billion USD at prevailing exchange rates). This growth underscores the increasing acceptance and efficacy of targeted biologic therapies in chronic inflammatory diseases.

In oncology, Novartis’s Kisqali (ribociclib), a CDK4/6 inhibitor for breast cancer, climbed an impressive 58% to $4.783 billion. This significant growth highlights the continued innovation and demand for effective treatments in specific cancer subsets. Johnson & Johnson also reported strong performance in its Innovative Medicine sector, driven primarily by products such as Darzalex (daratumumab) for multiple myeloma and Tremfya (guselkumab) for psoriasis and psoriatic arthritis.

The commercial picture is further reinforced by Citeline’s 2026 R&D review, which indicated that immunologicals were one of the few large therapeutic areas that still expanded, rising 20.6%, even as the overall pipeline count dipped. This data suggests sustained investment and innovation in immunology, promising a continued stream of new and improved treatments that will contribute significantly to the industry’s top line. These durable franchises in immunology and oncology demonstrate that while GLP-1s are making headlines, established and growing segments continue to be crucial pillars of pharmaceutical revenue.

The Broader Pharmaceutical Landscape: Innovation, Competition, and Future Trajectories

The FY2025 financial results paint a vivid picture of a dynamic and intensely competitive pharmaceutical market. The shift in molecular leadership from oncology to metabolic diseases signifies a critical juncture, reflecting not only scientific breakthroughs but also evolving global health priorities. The unprecedented demand for GLP-1 agonists highlights the vast commercial opportunities in addressing widespread conditions like obesity and type 2 diabetes, which carry enormous societal and economic burdens.

This intense competition, particularly in the anti-obesity market, is set to drive further innovation. The rapid expansion of the anti-obesity pipeline, with hundreds of compounds in development, suggests that companies are aggressively pursuing novel mechanisms of action, improved efficacy, and more convenient formulations (like oral options) to capture market share. However, this competitive environment also brings challenges, including potential pricing pressures and complex access dynamics, as evidenced by Novo Nordisk’s cautious 2026 outlook for semaglutide. Payers and healthcare systems will face increasing pressure to manage the costs associated with these highly effective but expensive treatments.

For the pharmaceutical industry at large, the strategic implications are profound. Companies must balance investment in proven, growing therapeutic areas like immunology and oncology with aggressive pursuit of emerging, high-growth segments like metabolic health. The ability to successfully launch and scale new blockbusters, while also managing the lifecycle of mature products and navigating patent expirations, will be paramount. Merck’s challenge with Keytruda’s LOE serves as a stark reminder of the continuous need for robust R&D pipelines and strategic diversification.

In conclusion, FY2025 marked a pivotal year, where the established order of pharmaceutical leadership began to cede ground to a new wave of innovation. While Keytruda remains a formidable brand, the collective power of tirzepatide and semaglutide at the molecular level underscores a transformative era for metabolic medicine. Alongside this, the enduring strength of immunology and other oncology franchises demonstrates the diversified nature of pharmaceutical growth. The industry stands at the cusp of further dramatic shifts, driven by scientific advancement, intense competition, and the ever-present demand for groundbreaking therapies that address global health challenges.

Leave a Reply