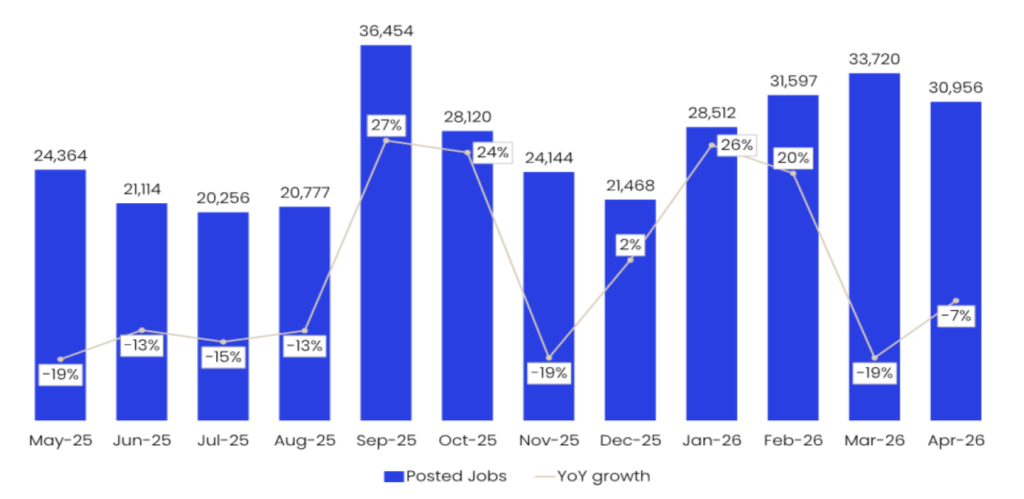

Global semiconductor job postings experienced a notable decline of 6.58% month-on-month in April 2026, settling at 30,956. This marks the second consecutive monthly decrease following a significant acceleration in hiring during January and February of the same year. While this pullback indicates a cooling in momentum, overall posting levels remain elevated compared to the lows observed in December 2025, suggesting a higher baseline run-rate for the industry. This shift in hiring patterns offers crucial insights for business leaders, serving as an early warning system for performance, skill erosion, and strategic investment opportunities long before financial results become apparent.

The semiconductor industry, a cornerstone of the global digital economy, has been a dynamic landscape of intense competition and rapid technological advancement. The period leading up to April 2026 saw a surge in demand for talent, fueled by a confluence of factors including the burgeoning artificial intelligence (AI) revolution, the ongoing expansion of cloud infrastructure, and the persistent drive for digital transformation across all sectors. Companies were actively investing in their workforces to secure the specialized skills needed to develop next-generation chips, enhance processing power, and integrate advanced functionalities into a wide array of devices and services. This intense hiring activity in late 2025 and early 2026 reflected a strategic imperative for companies to maintain their competitive edge and capitalize on emerging market opportunities.

However, the hiring landscape is inherently fluid. The current deceleration in job postings, particularly in April 2026, suggests a recalibration of investment strategies and potentially a more cautious approach to workforce expansion. Understanding these shifts is paramount for corporate leaders aiming to make informed decisions regarding capital allocation, cost management, and competitive positioning. The window of opportunity to act on these hiring signals is typically narrow, estimated at one to three months, meaning that by the time broader market consensus begins to acknowledge these trends, the underlying data will have already evolved. Therefore, granular analysis of job posting data, as provided by platforms like GlobalData Jobs Analytics, becomes indispensable for proactive strategic planning.

Analyzing the April 2026 Semiconductor Job Posting Landscape

The recent data reveals a complex picture of the semiconductor sector’s hiring priorities. Despite the overall monthly decline, the sector’s resilience is evident when compared to the trough levels of mid-2025. The volatile pattern observed over the past 12 months, with notable upticks in September 2025 and again in January-February 2026, followed by the recent retrenchment, underscores the dynamic nature of this industry. This ebb and flow in hiring activity can be attributed to a multitude of factors, including fluctuating consumer demand for electronics, geopolitical influences on supply chains, and the cyclical nature of semiconductor product development and manufacturing.

AI and Cloud Remain Dominant Themes in Semiconductor Hiring

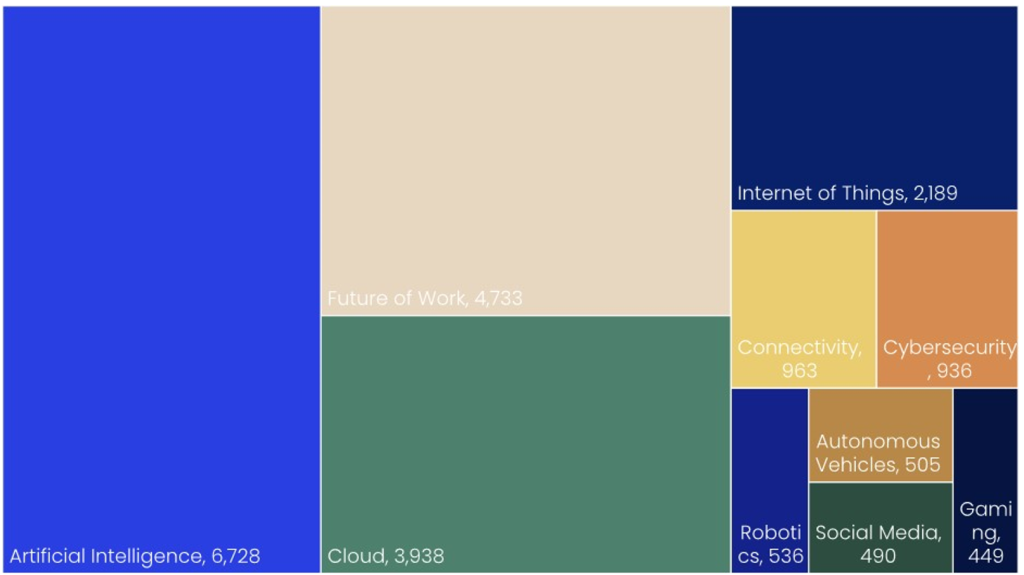

A deep dive into the thematic distribution of semiconductor job postings in April 2026 highlights a clear concentration of demand in Artificial Intelligence (AI) and the Future of Work (FOW). AI-related roles accounted for a significant 6,728 postings, underscoring the industry’s commitment to developing advanced AI chips and solutions. The FOW theme, with 4,733 postings, reflects the ongoing integration of technology into work processes, necessitating skilled professionals in areas like automation, remote collaboration tools, and advanced analytics.

Cloud computing, a foundational element of modern digital infrastructure, also remains a critical area of focus, generating 3,938 job postings. This indicates continued investment in the hardware and software components that power cloud services. Beyond these top three themes, other areas such as the Internet of Things (IoT) and connectivity garnered substantial interest, with 2,189 and 963 postings respectively. However, the volume of postings for these secondary themes drops off significantly, suggesting a more focused investment strategy within the semiconductor sector. Niche but rapidly developing areas like robotics, autonomous vehicles, and gaming, while important, currently represent a smaller portion of the overall hiring demand within the semiconductor job market. This thematic concentration signals where companies are placing their strategic bets for future growth and innovation.

US Continues as the Primary Hub for Semiconductor Talent

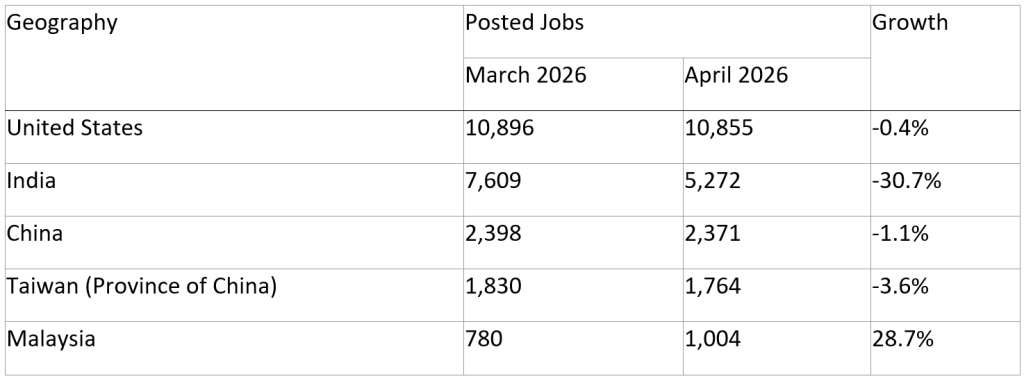

Geographically, the United States maintained its position as the largest market for semiconductor hiring in April 2026, with postings remaining relatively stable, showing a marginal decrease of 0.4% compared to March. This stability in the largest market is a key indicator of ongoing, albeit perhaps more measured, investment.

However, the global landscape presented a more varied picture. India experienced the most significant month-on-month contraction in semiconductor job postings, with a steep decline of 30.7%, representing the largest negative swing among the top hiring geographies. China and Taiwan, also crucial players in the global semiconductor ecosystem, saw modest decreases of 1.1% and 3.6% respectively.

In contrast, Malaysia emerged as a standout performer, demonstrating robust growth with a 28.7% increase in job postings, reaching 1,004. This upward trend in Malaysia suggests a potential diversification of manufacturing and R&D capabilities within the region, or perhaps a strategic move to leverage specific regional advantages. Overall, the April geographic hiring profile for semiconductors points to a stable dominant market accompanied by a dispersion of growth rates across other key regions, hinting at evolving global supply chain dynamics and investment strategies.

Mixed Hiring Momentum Among Top Semiconductor Employers

The hiring momentum among the leading employers in the semiconductor sector in April 2026 was decidedly mixed, reflecting varied strategic priorities and operational adjustments. IBM, despite remaining the largest single job poster with 4,248 positions, experienced a significant decline from its peak in February 2026, when it posted 9,517 roles. Its March figures also stood at a higher 6,952. This substantial drop contributes to a broader trend of softening momentum among the top-tier employers.

Hitachi, on the other hand, demonstrated relative stability, maintaining an elevated level of hiring with 2,300 postings in April, closely mirroring its March figure of 2,317. Several other prominent companies, including Qualcomm and Huawei, posted moderate increases in April, with Qualcomm reaching 1,203 postings and Huawei 917. This suggests continued, albeit perhaps more targeted, recruitment efforts.

Conversely, some major players saw a decrease in their hiring activity. Jabil’s job postings declined to 1,360, and Applied Materials also saw a reduction to 904. A noteworthy development was the entry of Infineon Technologies into the top employer list in April, with 751 postings. This is particularly significant given that Infineon had zero postings recorded in January, February, and March of 2026, indicating a substantial and sudden shift in its recruitment strategy within this specific month. This entry signals a potential re-prioritization or a strategic initiative that requires immediate talent acquisition.

Demand for Advanced Technical Skills Remains High

The technical skills in demand within the semiconductor sector in April 2026 underscore a continued emphasis on sophisticated engineering and development capabilities. Application Platforms and Containers emerged as the most sought-after technical skill set, with 4,960 job postings. This highlights the critical need for professionals adept at building, deploying, and managing complex software applications and containerized environments, essential for modern chip design and testing.

Systems Design and Integration followed closely, with 3,637 postings, indicating a strong demand for engineers who can architect and implement intricate systems and ensure seamless integration of various components. Operating Systems also ranked highly, with 3,408 postings, reinforcing the need for expertise in foundational software infrastructure and embedded systems development.

Beyond these core technical areas, the demand extended to enterprise application domains. Roles related to Application Lifecycle Management (ALM) and the support of HR/payroll applications were also prominent. This suggests a broader requirement for IT professionals who can manage the entire software development lifecycle and ensure the efficient operation of business-critical systems, demonstrating that technical recruitment in semiconductors extends beyond core chip design to encompass the entire value chain and operational support.

Implications for Leaders and Investors

The patterns observed in semiconductor job postings from April 2026 provide invaluable foresight for leaders and investors across all sectors. Hiring data serves as a leading indicator, offering insights into where investment, capacity, and competitive risks are truly shifting, often months before these trends are reflected in financial statements or market consensus.

For corporate leaders, understanding these dynamics is crucial for making sharper, more informed decisions. This includes identifying areas ripe for growth investment, recognizing segments where retrenchment might be necessary, and anticipating competitive moves. The ability to analyze how roles, skills, and geographic concentrations are evolving allows for proactive strategy formulation. For instance, a decline in postings for certain advanced skills might signal a need for internal upskilling initiatives or strategic partnerships, while a surge in demand for specific technologies could indicate an opportunity for market entry or acquisition.

Investors can leverage this granular data to refine their investment theses and identify undervalued or overvalued companies. Job postings often lead earnings revisions by a lead time of one to three months. Therefore, by monitoring these early signals, investors can position themselves ahead of market shifts and potentially achieve superior returns. The strategic implications are far-reaching, impacting not only the semiconductor industry itself but also the myriad sectors that rely on its innovations, from automotive and aerospace to healthcare and consumer electronics.

GlobalData Jobs Analytics, by providing point-in-time postings directly from company career pages and meticulously tagging them by company, sector, and theme, offers a powerful tool for translating complex hiring patterns into actionable intelligence. This data empowers leaders to move beyond reactive decision-making and embrace a more proactive, data-driven approach to strategic planning and investment. The ability to anticipate future workforce needs and technological trends is no longer a competitive advantage; it is a fundamental requirement for survival and success in today’s rapidly evolving global marketplace. Those who can effectively interpret and act upon these early indicators will be best positioned to navigate the complexities of the coming years and capitalize on emerging opportunities.