Japan’s latest National Health Insurance (NHI) drug price revision for Fiscal Year 2026 (FY26) has officially taken effect, ushering in an average reduction of 4.02% in drug prices on a spending basis, impacting approximately 15,800 products. While this reduction is marginally lower than the 4.67% decrease observed in FY24, the FY26 revision is characterized by a more complex interplay of pricing mechanisms. These include the significant expansion of G1 repricing rules, adjustments to the Patent-Period Price Maintenance Program (PMP), and a broader inclusion of biologics within the price reduction frameworks. This analysis delves into the specifics of the FY26 price revision, comparing the NHI-driven adjustments with the observed price movements across the broader Japanese pharmaceutical market in April 2026.

Understanding Japan’s Biennial Price Adjustment System

Japan’s healthcare system, like many developed nations, faces the perpetual challenge of controlling rising healthcare expenditures. A cornerstone of its cost-containment strategy in the pharmaceutical sector is the implementation of scheduled biennial price adjustments. These adjustments, conducted every two years, aim to reduce the financial burden on the National Health Insurance system and, by extension, taxpayers, while also incentivizing the use of cost-effective treatments. The system is designed to reflect market dynamics, therapeutic value, and patent lifecycles.

The process typically involves extensive data collection and analysis by the Ministry of Health, Labour and Welfare (MHLW), which then negotiates with pharmaceutical manufacturers and distributors. Key mechanisms driving these price changes include:

- Market Price-Based Repricing: This mechanism adjusts drug prices based on their actual transaction prices in the market. Drugs with a significant gap between their NHI-listed price and their actual market price are subject to reductions.

- Generic and Biosimilar Competition: The introduction and uptake of generic drugs and biosimilars naturally exert downward pressure on the prices of originator products. Japan’s system has specific rules to manage this, including the G1 repricing.

- Patent Expiry and Lifecycle Management: Prices for innovative drugs are often protected during their patent period. However, as patents expire, mechanisms are in place to reduce prices, especially as generic alternatives become available.

- Therapeutic Value and Innovation Premiums: To encourage innovation, Japan also has mechanisms that can support the pricing of novel or therapeutically significant drugs, often through premiums that can offset some downward pressures.

The FY26 revision represents a significant evolution of these mechanisms, particularly concerning the G1 repricing and the treatment of biologics, signaling a more aggressive approach to managing costs for a wider array of products.

NHI Drug Price Revisions for FY26: A Snapshot of Market Impact

Data from GlobalData’s Price Intelligence (POLI) database reveals that in April 2026, a substantial 73% of pharmaceutical products in Japan experienced a price change. Within this segment, the trend was overwhelmingly downward, with 61% of products receiving price cuts and only 12% seeing price increases. This stark contrast underscores the prevailing deflationary pressure on drug prices within the Japanese market following the FY26 revision. The remaining 27% of products remained unchanged in price.

The significant proportion of drugs experiencing price reductions highlights the broad reach of the FY26 NHI adjustments. This widespread impact is attributed to the refined and expanded application of existing pricing mechanisms. The average reduction of 4.02% across roughly 15,800 products, while seemingly modest, translates into substantial savings for the healthcare system when aggregated across such a large volume of pharmaceuticals.

The Expanded Scope of G1 Repricing: A Key Driver of Reductions

A central pillar of the FY26 price revision is the substantial expansion of the G1 repricing framework. Historically, the G1 rule has been a critical tool for managing prices of off-patent drugs, particularly those with high generic substitution rates. However, under the FY26 framework, eligibility for G1 repricing has been significantly broadened, moving away from solely relying on substitution rates to a more comprehensive assessment of market exposure and competition over time.

The revised G1 framework now mandates that all long-listed, off-patent products (LLPs) that have passed their initial patent protection and replacement period will be subject to the G1 rule. Crucially, this applies irrespective of their current generic substitution rate. This change dramatically increases the number of LLPs exposed to potential price reductions. Furthermore, biologic originators are now also subject to the G1 rule if their biosimilar counterparts are listed on the NHI. This inclusion of biologics represents a significant shift, as biologics often command higher prices and have longer development cycles, making them a key area for potential cost savings.

Under these updated rules, LLPs face a heightened risk of substantial price reductions for a period of five years following the introduction of the first NHI-listed generic. This means that even if a generic has not yet achieved a high market share, the originator product’s price can be adjusted downwards. This proactive approach aims to align prices more closely with the cost-effectiveness of therapies as they mature in the market.

Impact on Different Drug Categories

The ramifications of the expanded G1 repricing are particularly pronounced among off-patent products. Analysis indicates that the pricing pressure is most intensely felt by these drugs, especially those that have been in the market for an extended period and have faced sustained competition.

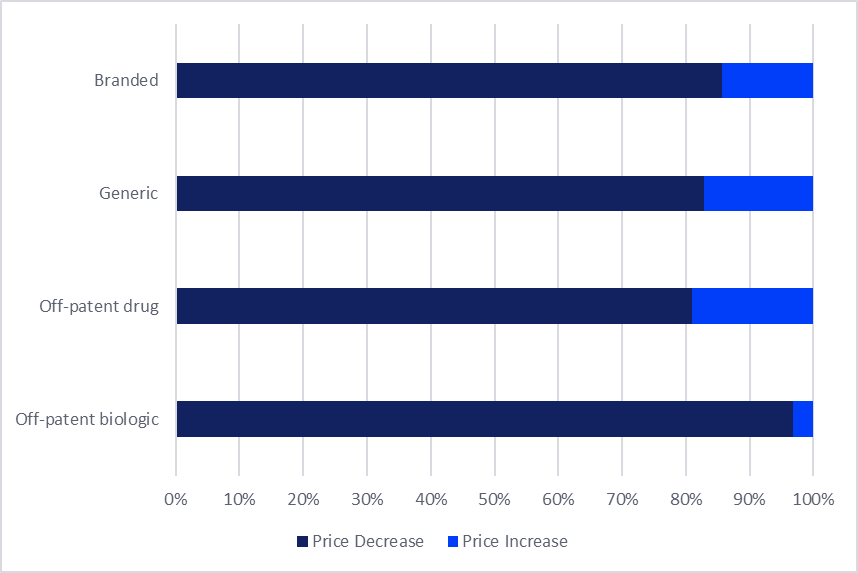

- Off-Patent Biologics: Among off-patent biologics, an overwhelming 95% experienced price reductions in April 2026. This reflects the direct impact of the expanded G1 rules on this high-value drug class.

- Off-Patent Small Molecules: Approximately 69% of off-patent originator small molecules also recorded a price decrease. This indicates that a significant majority of these established therapies have been affected by the downward price adjustments, a notable increase compared to the previous biennial revision in 2024, where only 57% of off-patent small molecules saw price reductions.

- Magnitude of Price Cuts: Beyond affecting a larger share of products, the FY26 revisions have also led to more substantial price cuts. A prime example is Roche’s anti-cancer biologic Avastin (bevacizumab), which saw an average price cut of 45% under the FY26 revision. Such significant reductions underscore the aggressive cost-containment objectives.

Figure 1: Price Adjustments in the Japanese Pharmaceutical Market (April 2026)

| Price Change Category | Percentage of Products |

|---|---|

| Price Reductions | 61% |

| Price Increases | 12% |

| No Price Change | 27% |

Source: GlobalData, Price Intelligence (POLI) database.

Figure 2: Percentage of Products Receiving Price Increases vs. Reductions by Drug Type (April 2026)

| Drug Type | Price Increases (%) | Price Reductions (%) |

|---|---|---|

| Off-Patent Biologics | N/A | 95% |

| Off-Patent Small Molecules | N/A | 69% |

| Overall Market | 12% | 61% |

Source: GlobalData, Price Intelligence (POLI) database.

Patent-Period Price Maintenance Program (PMP): Balancing Protection and Affordability

While the overarching trend is towards price reductions, the FY26 revision also includes measures to support the pricing of innovative and essential medicines. The Patent-Period Price Maintenance Premium (PMP) scheme, now renamed the Patent-Period Price Maintenance Program for Innovative Drugs, continues to play a crucial role. This program is designed to allow certain innovative, branded drugs to maintain their NHI-listed prices during their patent-protected period. This is a vital mechanism for incentivizing pharmaceutical R&D and ensuring that companies can recoup their investment in novel therapies.

The FY26 revision further enhances certain premium mechanisms, including the ability for eligible products to receive both marketability and pediatric premiums. These premiums can help offset some of the pricing pressures faced by innovative drugs, particularly those with limited market uptake or those addressing specific pediatric indications.

However, the PMP is not an absolute shield against price adjustments. The reform outlines that drugs exhibiting a significant gap between their NHI-listed price and their actual market price may still be subjected to downward adjustments. This provision ensures that even protected drugs are not immune to scrutiny if their listed prices appear disproportionately high compared to real-world transaction values.

Deferred Price Reductions and Their Impact

A notable feature of the FY26 revision is the increased visibility of deferred PMP repricing. This mechanism targets products that previously benefited from price protection during their patent period but are now subject to price cuts as that protection wanes or market dynamics shift. This effectively means that drugs that may have avoided earlier reductions are now facing them, often with significant consequences.

Several widely used therapies have been affected by these deferred reductions. In some instances, these price cuts have exceeded 20%, and in a few cases, have surpassed 30%. Notable examples include:

- AstraZeneca’s Forxiga (dapagliflozin): This medication experienced one of the most substantial price reductions, averaging 36% across all its formulations. Forxiga, a widely prescribed medication for type 2 diabetes and heart failure, now faces a significantly altered pricing landscape in Japan.

- Taiho Pharmaceutical’s Abraxane (paclitaxel): This chemotherapy drug also saw price reductions exceeding 30%. Abraxane, a critical treatment in oncology, now presents a case study in how established branded therapies are being re-evaluated under the revised pricing structure.

These deferred reductions highlight a strategic approach by the Japanese authorities to address the cumulative price erosion that may not have been fully captured in earlier revisions. It suggests a commitment to ensuring that pricing reflects the lifecycle stage and competitive environment of all drugs, not just new market entrants.

Figure 3: Manufacturer Price History (EUR) of Forxiga in Japan

(Visual representation of price trends for Forxiga, showing a significant dip post-FY26 revision)

Source: GlobalData, Price Intelligence (POLI) database.

Broader Implications for the Pharmaceutical Market

The FY26 NHI drug price revision in Japan carries significant implications for pharmaceutical manufacturers, healthcare providers, and patients:

- Increased Pressure on Profitability: The expanded scope of G1 repricing and the application of deferred reductions will undoubtedly place increased pressure on the profitability of pharmaceutical companies, particularly those with a large portfolio of off-patent products. Companies will need to adapt their pricing and market access strategies to account for these ongoing deflationary forces.

- Strategic Importance of Innovation: The continued, albeit conditional, support for innovative drugs through the PMP underscores the importance of bringing truly novel therapies to the Japanese market. Companies with strong R&D pipelines and products offering significant therapeutic advantages are likely to be better positioned to navigate the evolving pricing landscape.

- Shift Towards Value-Based Pricing: The emphasis on market price alignment and the broader inclusion of biologics in repricing mechanisms suggest a continued move towards value-based pricing principles. Prices will increasingly be scrutinized based on their correlation with actual market transactions and therapeutic outcomes.

- Focus on Supply Chain Stability: While cost containment is a primary objective, the inclusion of mechanisms to support unprofitable, supply-sensitive drugs demonstrates the MHLW’s commitment to maintaining a stable supply of essential medicines. This delicate balance between cost reduction and supply assurance will remain a key consideration.

- Data and Analytics as Critical Tools: The detailed analysis of price changes, as provided by sources like GlobalData’s POLI database, highlights the critical role of robust data and market intelligence for pharmaceutical stakeholders. Understanding the nuances of these revisions and their impact on specific products and therapeutic areas is essential for strategic decision-making.

In conclusion, Japan’s FY26 NHI drug price revision represents a comprehensive recalibration of its pharmaceutical pricing strategy. While the overall average price reduction may appear modest, the expansion of the G1 repricing framework, the inclusion of biologics, and the application of deferred price cuts signal a more aggressive and far-reaching approach to cost containment. This evolving landscape necessitates a strategic adaptation from pharmaceutical companies, emphasizing innovation, market intelligence, and a keen understanding of Japan’s dynamic healthcare policy. The dual approach of reducing prices for mature products while providing continued, albeit conditional, support for innovation aims to strike a balance between fiscal responsibility and the ongoing need for accessible, high-quality healthcare.

Leave a Reply