The pharmaceutical industry witnessed a significant shift in its commercial landscape during Fiscal Year 2025, with Merck’s oncology powerhouse, Keytruda (pembrolizumab), retaining its position as the top-selling individual brand. However, a deeper analysis at the molecular level reveals a new hierarchy, where the combined sales of diabetes and obesity medications based on tirzepatide and semaglutide have collectively surpassed Keytruda’s impressive revenue. This realignment underscores the burgeoning influence of metabolic health treatments and the ongoing evolution of the global pharmaceutical market.

The Shifting Landscape of Pharmaceutical Dominance

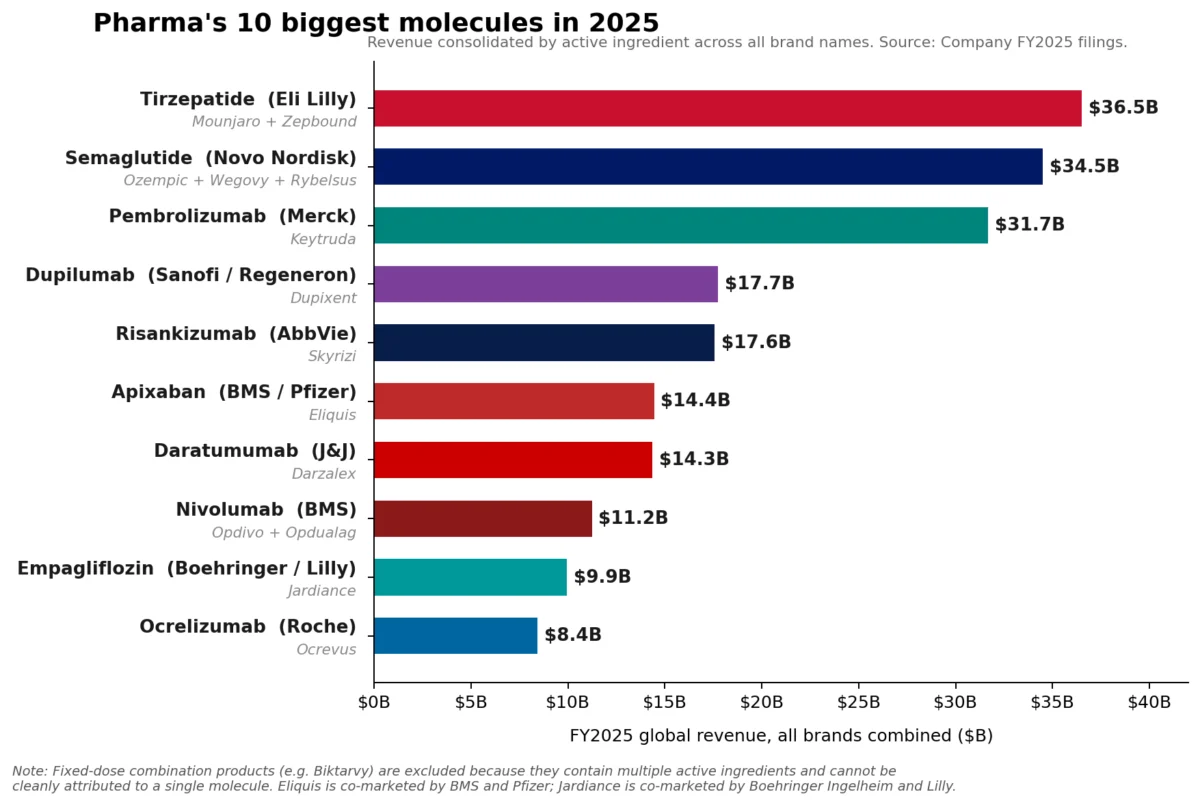

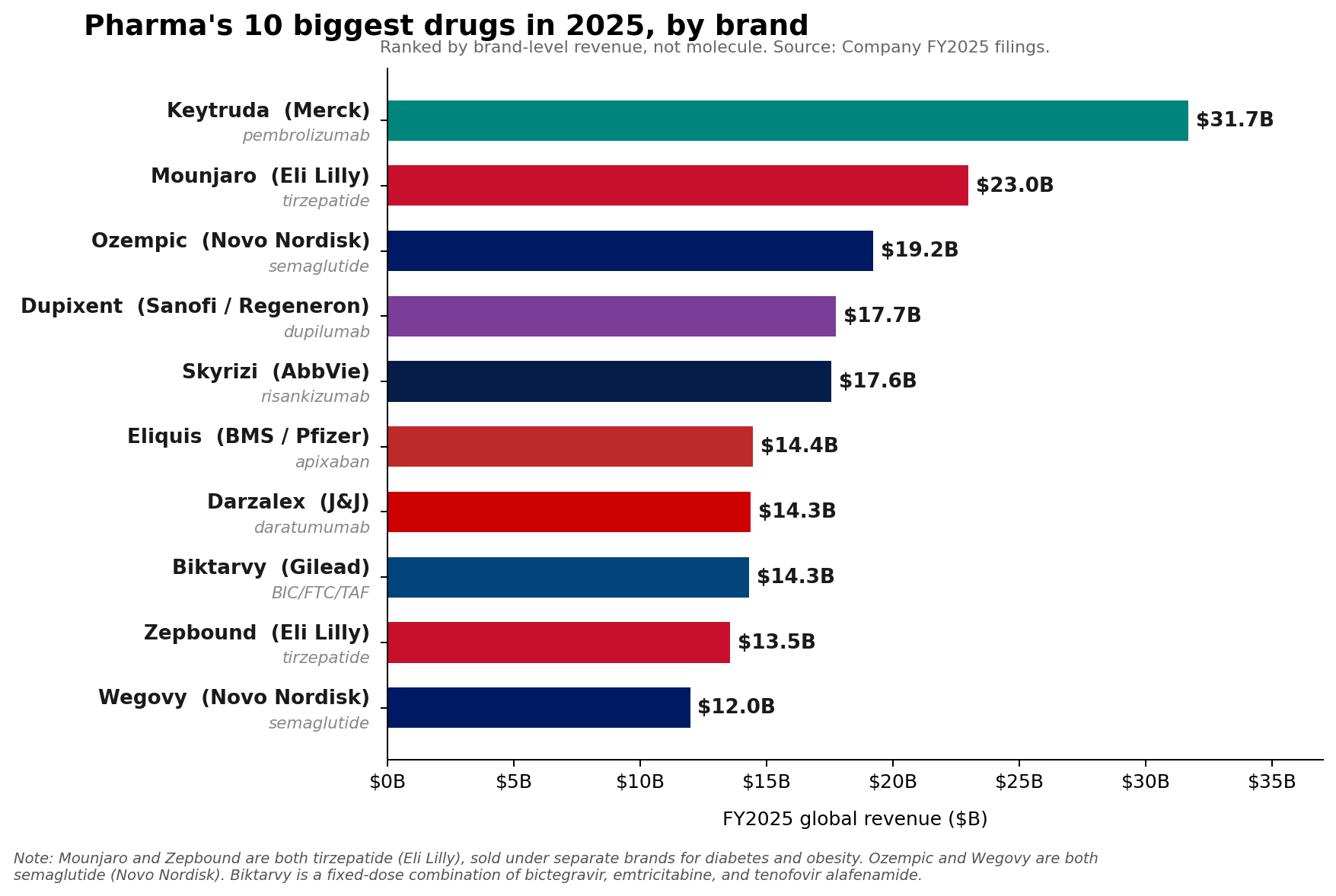

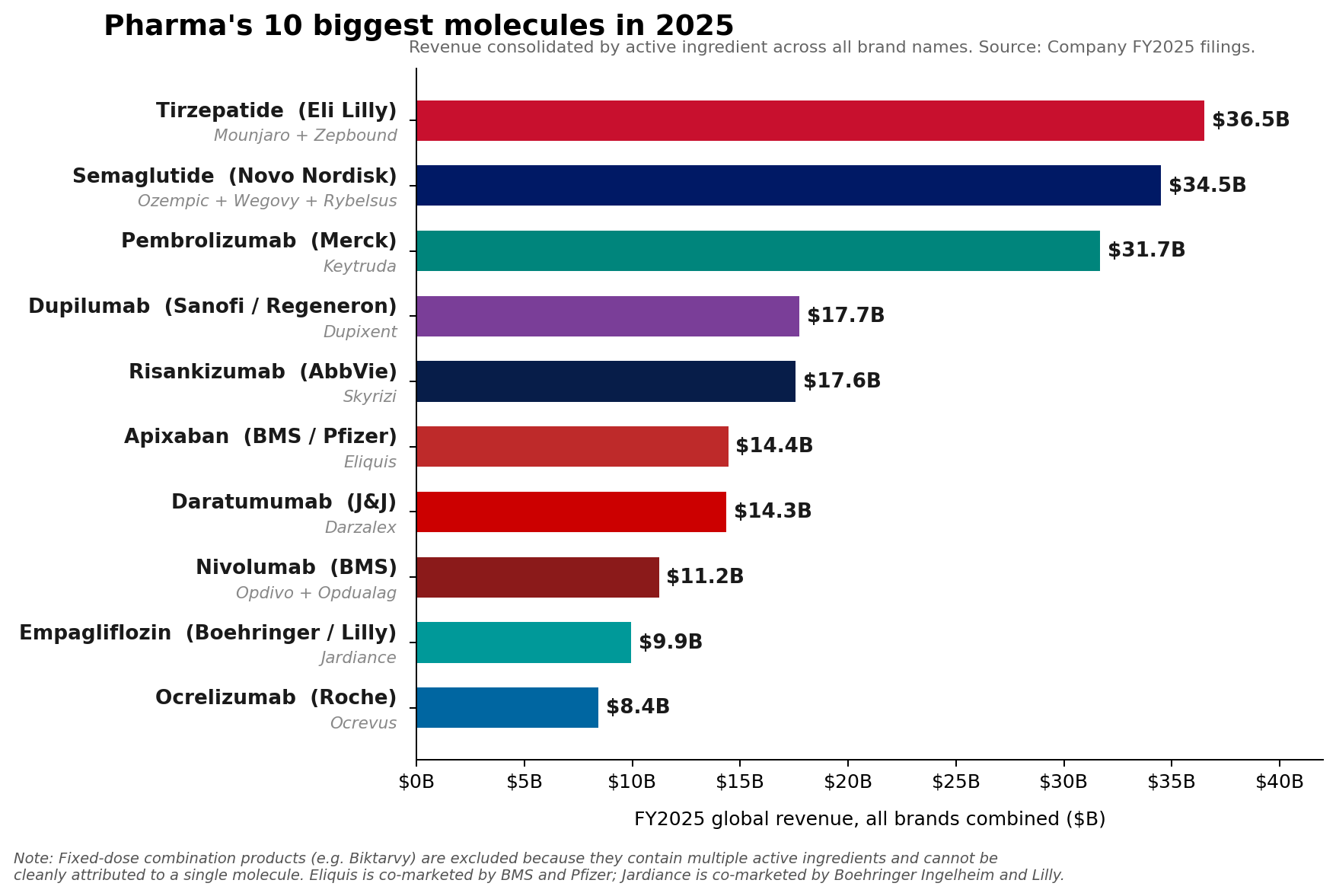

In FY2025, Merck’s Keytruda, a cornerstone of modern immuno-oncology, generated a formidable $31.7 billion in sales, solidifying its status as the world’s leading pharmaceutical brand. This continued dominance is a testament to its broad utility across numerous cancer indications and Merck’s strategic lifecycle management. However, the aggregate sales of two distinct glucagon-like peptide-1 (GLP-1) receptor agonist franchises—Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide—have collectively eclipsed Keytruda’s molecular-level leadership.

Lilly’s tirzepatide franchise, comprising the diabetes medication Mounjaro and the weight-loss drug Zepbound, achieved a combined revenue of approximately $36.5 billion in 2025. Mounjaro contributed $22.965 billion, while Zepbound, despite its more recent market entry, rapidly climbed to $13.542 billion. Similarly, Novo Nordisk’s semaglutide franchise, encompassing the diabetes treatments Ozempic and Rybelsus, and the weight-loss drug Wegovy, reached an estimated total of $34.5 billion. These figures highlight an unprecedented surge in demand for GLP-1 agonists, driven by the global epidemics of type 2 diabetes and obesity. The rapid ascent of these molecules signals a pivotal moment, challenging the long-held supremacy of oncology blockbusters.

Keytruda’s Enduring Strength and Looming Patent Cliff

Merck’s Keytruda, a monoclonal antibody that targets the programmed cell death protein 1 (PD-1), has revolutionized cancer treatment since its initial approval. Its mechanism of action, by blocking the PD-1 pathway, helps to restore the immune system’s ability to recognize and kill cancer cells. In 2025, Keytruda demonstrated robust growth of 7%, reflecting its continued expansion into new indications and earlier lines of therapy across a diverse range of cancers, including melanoma, non-small cell lung cancer, head and neck squamous cell carcinoma, and classical Hodgkin lymphoma.

Merck’s strategy to extend the franchise’s longevity beyond its patent expiration, expected in the coming years, involves continuous innovation. This includes pursuing new indications to broaden its patient base and developing alternative formulations, such as the subcutaneous Keytruda QLEX. Subcutaneous administration offers greater convenience for patients and healthcare providers, potentially extending the drug’s market exclusivity and mitigating the impact of biosimilar competition post-patent cliff.

Despite Keytruda’s strong performance, the impending loss of exclusivity remains a critical concern for Merck. CEO Rob Davis has characterized this future revenue decline as "more of a hill than a cliff," suggesting that strategic moves and a robust pipeline are in place to absorb the impact. However, the market’s reaction to Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion, which came in below Wall Street expectations, indicates lingering apprehension regarding the post-Keytruda era. Investors are closely monitoring Merck’s pipeline diversification efforts, particularly in oncology and other therapeutic areas, to ensure sustained growth. The company’s ability to successfully launch and scale new products before Keytruda’s patent expiry will be crucial in navigating this transition.

The Ascendancy of GLP-1 Agonists: A New Era in Metabolic Health

The explosive growth of tirzepatide and semaglutide marks a paradigm shift in pharmaceutical revenue drivers. Both molecules are synthetic analogues of incretin hormones, primarily glucagon-like peptide-1 (GLP-1), which play a crucial role in glucose-dependent insulin secretion, appetite regulation, and gastric emptying. Tirzepatide distinguishes itself as a dual GIP (glucose-dependent insulinotropic polypeptide) and GLP-1 receptor agonist, offering a potentially more potent mechanism for glycemic control and weight reduction compared to pure GLP-1 agonists.

Eli Lilly’s Mounjaro, initially approved for type 2 diabetes, quickly garnered attention for its significant weight-loss benefits, leading to the subsequent approval and launch of Zepbound specifically for chronic weight management. The combined sales figures underscore an unprecedented demand, with patients and physicians embracing these therapies for their efficacy in managing metabolic diseases. The rapid uptake of Zepbound, in particular, demonstrates the vast unmet need in the obesity market, which historically has lacked highly effective and well-tolerated pharmacological interventions.

Novo Nordisk’s semaglutide franchise has similarly capitalized on this demand. Ozempic, its injectable GLP-1 for type 2 diabetes, and Wegovy, the higher-dose version approved for weight management, have become household names. Rybelsus, the oral formulation of semaglutide for diabetes, further broadens the accessibility of this class of drugs. The success of these franchises is not just about sales figures; it reflects a profound impact on public health, offering effective tools to combat conditions that contribute to numerous comorbidities, including cardiovascular disease, kidney disease, and certain cancers.

However, this rapid growth has not been without challenges. Both Lilly and Novo Nordisk have faced significant supply constraints due to overwhelming demand, leading to manufacturing ramp-ups and strategic investments in production capacity. Pricing and market access also remain critical considerations, with ongoing discussions among payers, policymakers, and pharmaceutical companies about ensuring equitable access to these life-changing medications.

The Oral Revolution: Orforglipron’s Strategic Entry

The competitive landscape in the obesity market is intensifying rapidly, with Eli Lilly’s orforglipron (marketed as Foundayo) emerging as a significant new entrant. Approved by the FDA on April 1, 2026, and commercially available just days later on April 9, Foundayo represents a strategic milestone: it is an oral small-molecule GLP-1 receptor agonist. Unlike the injectable tirzepatide and semaglutide, orforglipron offers the convenience of a once-daily pill, a factor that could dramatically increase patient adherence and market penetration, especially for individuals hesitant about injectables.

Lilly licensed orforglipron from Chugai in 2018, recognizing the potential for an oral option in the burgeoning metabolic health space. While analysts currently present a mixed outlook on its immediate commercial potential, its strategic importance cannot be overstated. Lilly’s 2026 revenue guidance of $80 billion to $83 billion, largely driven by the continued growth of Mounjaro and Zepbound, already reflects high expectations. Foundayo’s approval after the first quarter ended means its impact will be more pronounced in the latter half of 2026, but its very presence reshapes market dynamics.

Citeline’s 2026 Pharma R&D Annual Review reinforces the significance of this development, noting a "gut-busting 30.7%" expansion in the anti-obesity pipeline, which now includes 588 active compounds. This surge in R&D activity, set against a backdrop of overall pipeline contraction, highlights the industry’s fervent pursuit of innovative solutions for weight management. Orforglipron, while entering a market already dominated by Lilly’s own blockbuster injectables, is positioned to capture a segment of patients who prioritize oral administration, potentially expanding the overall market rather than merely cannibalizing existing sales. Its launch signals a move towards broader accessibility and patient choice within the GLP-1 class.

Oral Semaglutide and Novo Nordisk’s Strategic Plays

Novo Nordisk is also actively pursuing the oral GLP-1 segment, with the newer Wegovy pill launching in January 2026. This oral formulation of semaglutide aims to mirror the success of its injectable counterpart and its oral diabetes drug, Rybelsus, which saw a 2% decline at constant exchange rates (CER) in 2025, indicating the shift in focus towards the newer weight-loss indications. Novo Nordisk’s plans include a broader rollout of oral Wegovy in 2026, along with the introduction of new doses, such as the 7.2 mg dose in various countries and the recent launch of Wegovy HD in the U.S.

Despite these strategic moves to expand the semaglutide franchise, Novo Nordisk’s 2026 adjusted sales growth guidance of negative 5% to negative 13% at CER reflects significant challenges. These include intense pricing pressure, increased competition from emerging players like Lilly, and complex U.S. market access dynamics. While oral semaglutide is strategically vital for widening the treatment funnel and improving patient access, it is not currently projected to be the primary driver of absolute revenue growth for Novo Nordisk in 2026. The company faces the delicate balance of maximizing market penetration while navigating a rapidly evolving and increasingly competitive landscape.

Beyond GLP-1s: Robust Growth in Immunology and Oncology

While the GLP-1 narrative dominates headlines, other specialty therapeutic areas, particularly immunology and oncology, continue to demonstrate robust growth and contribute significantly to the pharmaceutical leaderboard. These established franchises are showing remarkable resilience and continued expansion.

AbbVie’s immunology portfolio, anchored by Skyrizi (risankizumab) and Rinvoq (upadacitinib), exemplifies this trend. Skyrizi, an interleukin-23 (IL-23) inhibitor for conditions like psoriasis and psoriatic arthritis, reached $17.562 billion in 2025 sales. Rinvoq, a JAK inhibitor approved for various autoimmune diseases including rheumatoid arthritis, psoriatic arthritis, and atopic dermatitis, achieved $8.304 billion. Together, these two drugs generated $25.866 billion in 2025, accounting for approximately 42% of AbbVie’s total net revenue of $61.160 billion. This indicates that AbbVie has successfully built a powerful, two-drug immunology engine that is approaching the scale of the industry’s largest single brands. AbbVie’s guidance for 2026 adjusted EPS of $14.37 to $14.57 underscores confidence in the sustained growth of these assets.

Sanofi’s Dupixent (dupilumab), an IL-4 and IL-13 inhibitor for atopic dermatitis, asthma, and other inflammatory conditions, also continued its upward trajectory, rising to €15.714 billion (approximately $17.1 billion USD at average 2025 exchange rates). Novartis’ Kisqali (ribociclib), a CDK4/6 inhibitor for breast cancer, climbed an impressive 58% to $4.783 billion, demonstrating strong performance in the oncology space. Johnson & Johnson reported that its 2025 Innovative Medicine growth was primarily fueled by products such as Darzalex (daratumumab) for multiple myeloma and Tremfya (guselkumab) for psoriasis and psoriatic arthritis.

The continued expansion of these brands is supported by broader industry trends. Citeline’s 2026 R&D review highlighted that immunologicals were among the few large therapeutic categories that saw pipeline expansion, growing 20.6% even as the overall pipeline count experienced a slight dip. This indicates sustained investment and innovation in immunology, suggesting that the pharmaceutical leaderboard below Keytruda is not solely transforming into a GLP-1 monoculture. Instead, it is becoming increasingly diverse, crowded with large, durable franchises in immunology and oncology that are still compounding their growth through new indications, formulations, and market penetration.

Broader Market Implications and Future Outlook

The 2025 financial results and 2026 outlook paint a vivid picture of a pharmaceutical market in flux, characterized by intense competition and dynamic innovation. The emergence of GLP-1 agonists as molecular-level revenue leaders signifies a pivotal shift from oncology-centric dominance towards a broader therapeutic landscape where metabolic health holds immense commercial power. This shift is likely to influence future R&D investments, M&A strategies, and talent acquisition across the industry.

For pharmaceutical companies, the emphasis on lifecycle management, pipeline diversification, and strategic market entry for new formulations (like oral GLP-1s) will be paramount. Merck’s proactive measures to mitigate the Keytruda patent cliff, Lilly’s bold move with orforglipron, and Novo Nordisk’s expansion of oral semaglutide all underscore the imperative to adapt and innovate in the face of evolving market demands and competitive pressures.

The sustained growth of immunology and oncology franchises also reinforces the idea that blockbuster drugs can continue to deliver significant value through strategic expansion and addressing unmet needs within their respective therapeutic areas. The market’s ability to support multiple, multi-billion-dollar franchises across diverse fields suggests a robust and expanding global healthcare expenditure.

Ultimately, the narrative of the Pharma 50 in 2025 and beyond is one of relentless innovation and intense competition. While Keytruda maintains its brand supremacy, the collective might of tirzepatide and semaglutide heralds a new era, positioning metabolic health at the forefront of pharmaceutical growth. The industry’s ability to navigate patent expirations, manage supply chains, ensure patient access, and continue delivering groundbreaking therapies will define its trajectory in the years to come.

Leave a Reply