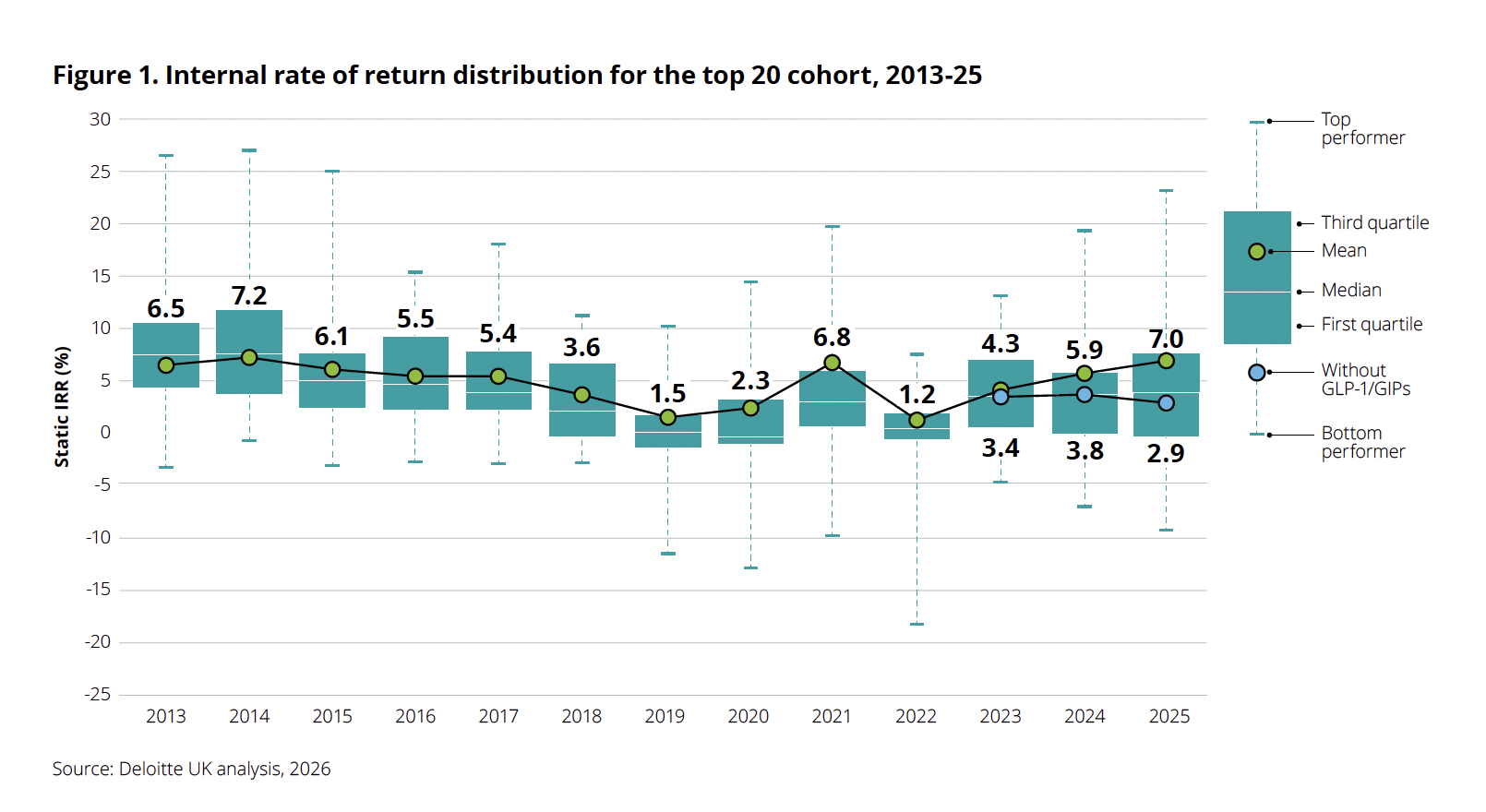

A new report from Deloitte, titled "Navigating the GLP-1 boom," indicates a significant resurgence in biopharma R&D productivity, with the projected internal rate of return (IRR) on late-stage pipeline assets reaching 7.0% in 2025. This marks a third consecutive year of growth, a notable improvement from 5.9% the previous year, signaling a potential thaw after a period of uneven post-pandemic expansion. However, the comprehensive 16th edition of Deloitte’s annual Measuring the Return from Pharmaceutical Innovation report underscores a critical caveat: this impressive recovery is overwhelmingly dependent on the performance of a single class of therapies, the GLP-1/GIP drugs targeting obesity and related metabolic conditions.

According to Kevin Dondarski, principal for life sciences strategy at Deloitte Consulting, the recent upward trend in R&D returns is "analytically unprecedented," especially following a prolonged period of decline, excluding the transient impact of the COVID-19 pandemic. This positive trajectory paints a seemingly vibrant picture for the biopharmaceutical sector, suggesting a transition from a challenging "winter" to a promising "spring." Yet, beneath the surface of this headline figure lies a more complex reality.

The GLP-1 Phenomenon: A Double-Edged Sword

The report highlights that GLP-1/GIP drugs account for an estimated 38% of all projected commercial inflows from the 2025 late-stage pipeline. The sheer magnitude of their contribution becomes starkly apparent when these therapies are excluded from the analysis: the headline internal rate of return plummets from 7.0% to a mere 2.9% for 2025. This contrasts sharply with 2024, when the overall IRR stood at 5.9%, reducing to 3.8% without GLP-1/GIP drugs. This year’s impact represents the most dramatic instance in the 16-year history of the Deloitte report where the removal of a single drug class has so significantly altered the overall IRR direction.

"There are two different messages here," Dondarski explained. "One, it’s certainly attractive, because the market is valuing the potential impact that those therapies can have on the public, which is great. But at the same time, it raises the question of sustainability. As those programs progress, is there going to continue to be that opportunity through the next generation and the next? It will create a responsibility for these companies to find the right assets to replace in the pipeline."

GLP-1 (Glucagon-like peptide-1 receptor) and GIP (glucose-dependent insulinotropic polypeptide) receptor agonists are a class of medications initially developed for type 2 diabetes but have shown remarkable efficacy in weight management. Their mechanism involves mimicking natural hormones that regulate blood sugar, slow gastric emptying, and promote feelings of fullness, leading to significant weight loss. The burgeoning global obesity epidemic, coupled with the profound health benefits associated with weight reduction, has fueled an unprecedented demand for these drugs, catapulting them into blockbuster status.

Market Concentration and Pipeline Dynamics

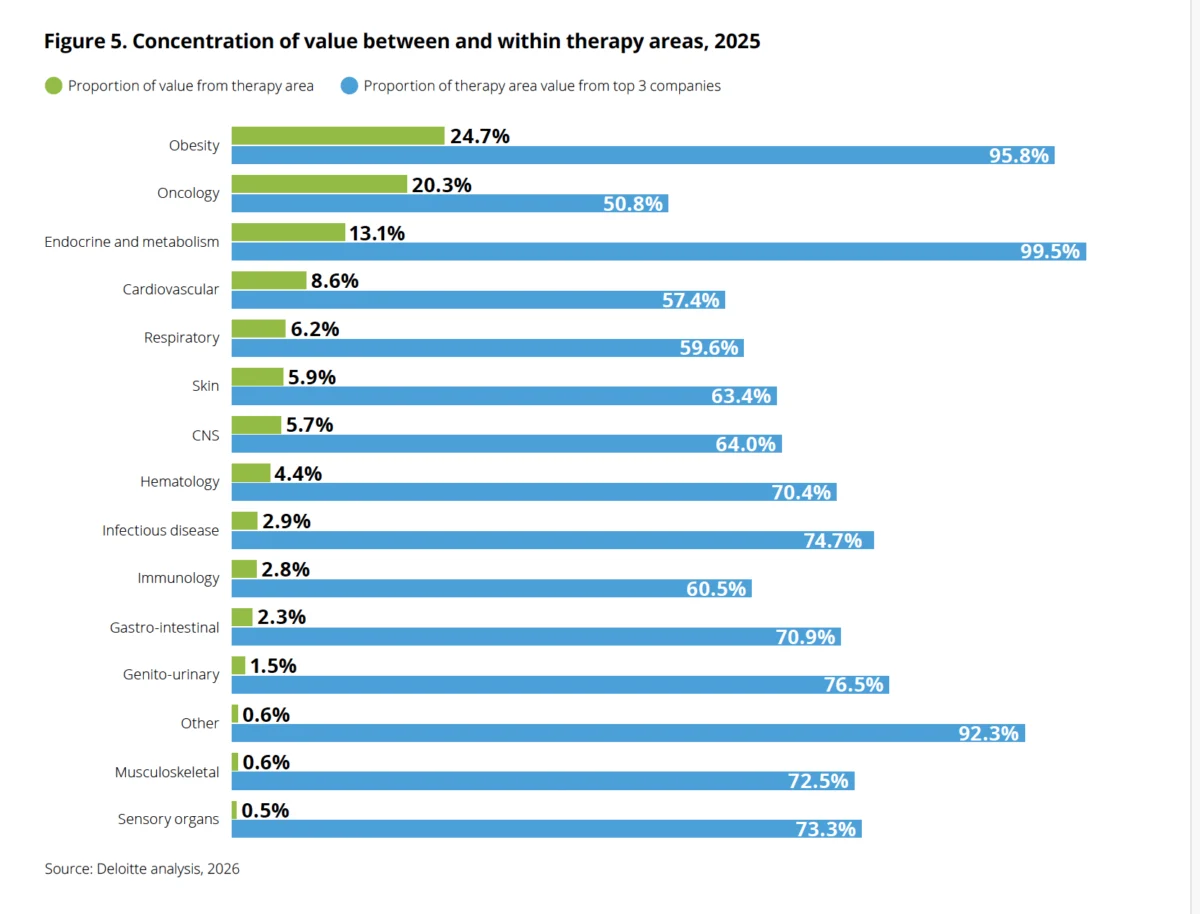

The transformative power of GLP-1s is further evidenced by their reordering of the therapeutic landscape. For the first time in the report’s 16-year history, obesity now commands the largest share of late-stage pipeline value, at 24.7%, surpassing oncology, which sits at 20.3%. This shift underscores a profound reallocation of research and development focus within the industry. However, this dominance is highly concentrated; nearly 96% of the value within the obesity segment is attributed to just three companies, primarily Eli Lilly and Novo Nordisk, highlighting a significant concentration of market power and innovation within a very narrow field.

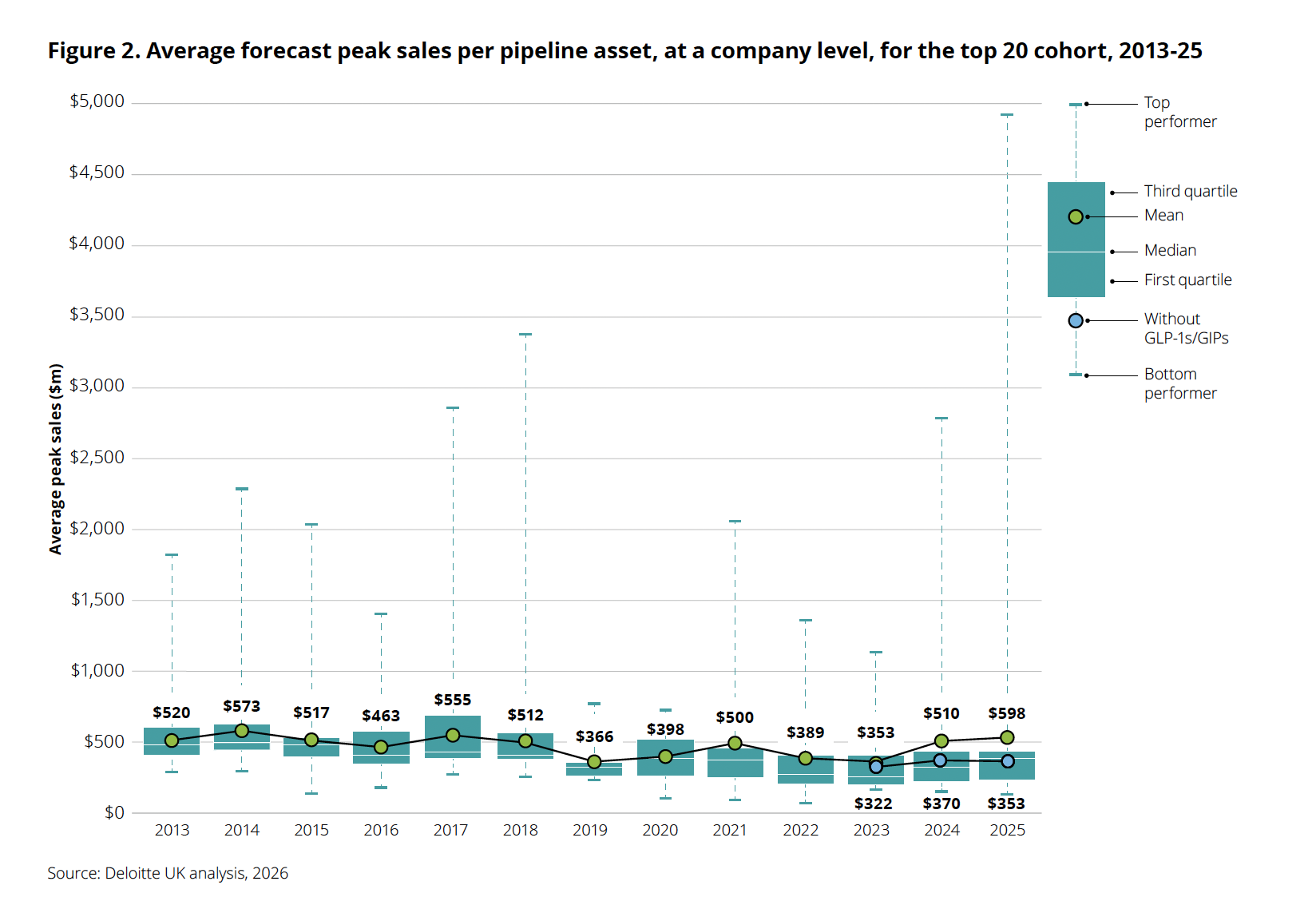

The average forecast peak sales per pipeline asset reflect this disparity. While the overall average jumped to $598 million in 2025, the underlying figures reveal a concerning trend. The top-performing assets, largely GLP-1s, are now approaching $5 billion in projected peak sales. In stark contrast, when GLP-1/GIP drugs are excluded, the average forecast peak sales per asset drop to $353 million, which is actually lower than the figure from the previous year. This indicates that without the stellar performance of obesity blockbusters, the underlying productivity of the broader pharmaceutical pipeline is, in fact, declining.

Turbulence Amidst the Boom: Company Performance and Market Signals

Despite the overarching narrative of surging returns, the market signals surrounding the GLP-1 boom have been mixed, particularly for the leading developers, Eli Lilly and Novo Nordisk. Investors have grappled with questions about the durability and sustainability of this rapid growth.

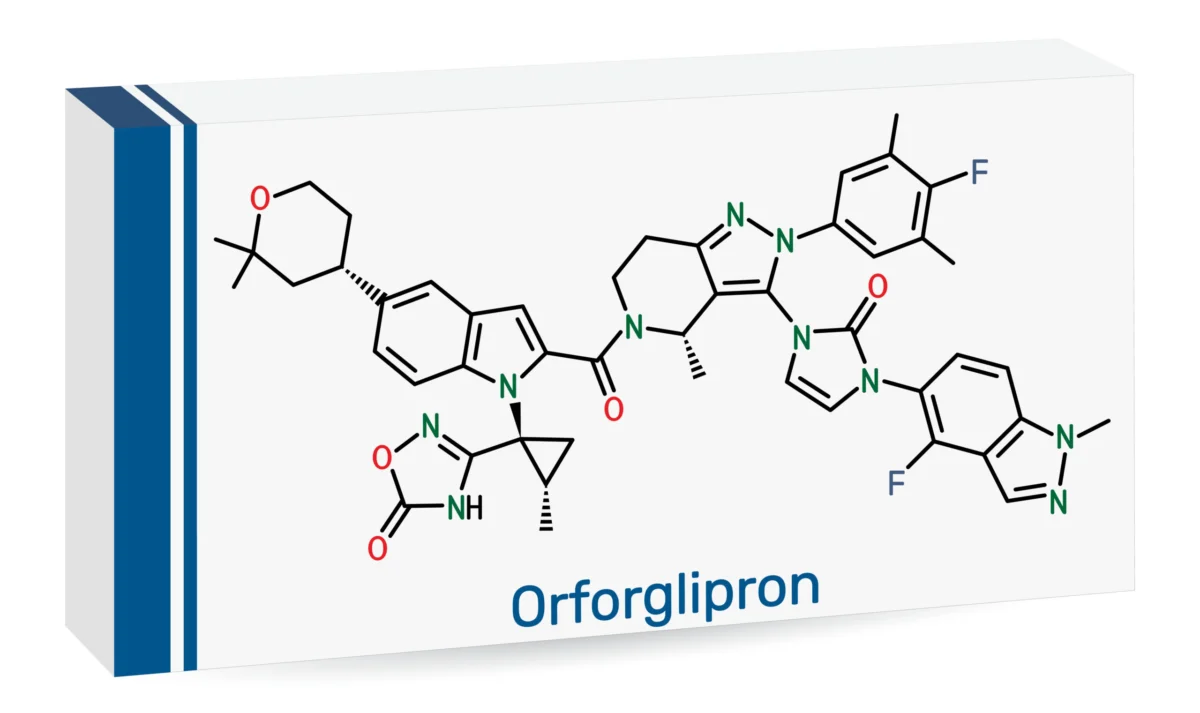

Eli Lilly, the developer of tirzepatide (marketed as Zepbound for weight loss and Mounjaro for diabetes), and the recently launched oral GLP-1 orforglipron (Foundayo, April 2026), has experienced some stock volatility. Since the beginning of the year, the company’s stock has seen a skid of roughly 10-13% year-to-date. This occurred even as the company raised its full-year revenue guidance to an impressive $82-$85 billion, primarily on the strength of Mounjaro and Zepbound volume growth. Lilly’s first-quarter 2026 financial results were robust, reporting revenue of $19.8 billion (exceeding analysts’ expectations of $17.6 billion), representing a 56% year-over-year increase. This growth was largely driven by Mounjaro sales of $8.7 billion (+125%) and Zepbound sales of $4.1 billion (+79%). However, a closer look revealed that this 56% revenue growth was propelled by a 65% volume increase, partially offset by a 13% decline in realized prices, indicating increasing pricing pressures.

Novo Nordisk, another dominant player with Ozempic and Wegovy, has also navigated a period of significant change and investor scrutiny. In 2025, the company saw a leadership transition, with longtime CEO Lars Fruergaard Jorgensen replaced by Maziar Mike Doustdar, amidst slowing momentum and share-price pressure. This period of recalibration also included a significant restructuring; seven board members stepped down at an extraordinary general meeting in November 2025, and the company announced plans to cut approximately 9,000 roles from its global workforce of 78,400. By Q1 2026, Novo Nordisk reported employing about 67,900 individuals, implying a reduction of around 10,500 roles since the restructuring announcement.

Adding to Novo Nordisk’s challenges, its highly anticipated combination therapy, CagriSema (a blend of the amylin analogue cagrilintide and semaglutide), failed to meet expectations. In February 2026, results from the REDEFINE 4 Phase 3 head-to-head trial showed CagriSema delivering 23.0% weight loss, failing to demonstrate non-inferiority against Lilly’s Zepbound, which achieved 25.5% weight loss. This clinical setback triggered another wave of investor disappointment regarding Novo Nordisk’s future growth drivers beyond its current GLP-1 portfolio.

Novo Nordisk’s Q1 2026 results reported sales of DKK 96.8 billion ($15.2 billion). Its oral Wegovy pill, launched on January 5, generated DKK 2.26 billion in its first quarter, nearly double the DKK 1.16 billion analysts had expected, showcasing strong initial uptake. However, the company’s adjusted sales still fell by 4% at constant exchange rates once a one-time $4.2 billion 340B provision reversal was excluded, highlighting underlying challenges in sustaining growth at previous rates.

Addressing Affordability: Pricing and Access Initiatives

The immense demand and high cost of GLP-1s have also brought them under increasing scrutiny regarding pricing and patient access. Both Eli Lilly and Novo Nordisk have entered agreements to lower U.S. prices for GLP-1s through federal programs like Medicare and Medicaid, as well as initiatives akin to TrumpRx. A November deal was expected to expand Medicare and Medicaid coverage for weight-loss indications for the first time, with eligible beneficiaries potentially benefiting from $50 monthly copays. Furthermore, public pricing platforms now list specific GLP-1 medications at significantly reduced monthly costs: Wegovy pill at $149, Wegovy pen at $199, Ozempic at $199, and Zepbound at $299. These initiatives reflect a growing societal and governmental pressure to make these transformative, yet expensive, therapies more accessible to a broader patient population.

The Spiraling Cost of R&D

While GLP-1s drive a headline surge in returns, the underlying cost of bringing new drugs to market continues its relentless climb. The Deloitte report found that the average cost to develop a drug from discovery to launch increased to $2.67 billion in 2025, up from $2.23 billion the year before. This escalation is not an anomaly attributable to a single outlier; Dondarski confirmed that "We saw the cost increase for 17 out of the 20 companies, so it was a persistent theme."

Several factors converged to fuel this spike. Firstly, R&D costs have continued to rise above general inflation rates, reflecting the increasing complexity and technological demands of modern drug discovery. Secondly, large-scale mergers and acquisitions (M&A) deals have inflated the overall R&D cost base, as companies integrate expensive pipelines and development programs. Finally, a persistent attrition rate, which saw the overall number of late-stage programs shrink by roughly 4-5%, means that the costs of failed programs are amortized across fewer successful ones, further driving up the average cost per launched asset. This trend exacerbates the long-standing challenge of declining R&D productivity that has plagued the pharmaceutical industry for decades.

AI: Still Waiting for Liftoff

Last year’s edition of the Deloitte report, provocatively titled "Be brave, be bold," urged pharmaceutical companies to aggressively adopt AI-powered drug development platforms, automation, and advanced analytics as a crucial pathway to reversing the decades-long decline in R&D productivity. The vision was clear: AI could streamline discovery, optimize clinical trials, and drastically cut costs and timelines.

However, the 2025 data paints a picture of aspiration rather than widespread transformation. Despite the enthusiastic rhetoric and significant investment in AI capabilities across the industry, R&D costs continued their ascent to a record $2.67 billion per asset, and clinical cycle times have remained stubbornly long. The report now concedes that AI’s promise to significantly reduce development time and costs "has not yet been realized at scale, largely due to a pilot-driven, function-by-function approach."

Dondarski offers a nuanced perspective on the current state of AI adoption. "Everybody’s actively focusing on AI, and everybody’s had some degree of success," he noted, acknowledging the pockets of innovation and efficiency gains. "But from our vantage point, there’s a good amount of variability in the velocity at which organizations are scaling those efforts to maximize value creation." This suggests that while individual projects or departments may be leveraging AI effectively, a comprehensive, integrated, and enterprise-wide application that could truly revolutionize R&D remains elusive. Challenges such as data integration, regulatory complexities, and the need for significant cultural and operational shifts within large organizations continue to hinder the full-scale deployment of AI in drug discovery and development.

Implications and Future Outlook

The insights from Deloitte’s report present a multifaceted challenge for the pharmaceutical industry. The unprecedented success of GLP-1s has provided a much-needed boost to R&D returns, demonstrating the immense value that truly innovative therapies can generate. However, this success is also a precarious foundation. The extreme concentration of value in a single therapeutic class raises profound questions about the long-term sustainability of these returns. A potential future slowdown in GLP-1 market growth, increased competition, or unforeseen clinical challenges could severely impact the industry’s overall financial health.

Pharmaceutical companies face an urgent mandate to diversify their pipelines beyond the current GLP-1 boom. This requires renewed investment and innovation in other therapeutic areas, particularly as oncology, a long-standing pillar of R&D, has been displaced in pipeline value. The escalating cost of drug development further amplifies this challenge, demanding more efficient and productive R&D models. The unfulfilled promise of AI at scale underscores the need for a more strategic and holistic approach to technological integration, moving beyond pilot programs to enterprise-wide transformation.

The "golden goose" effect of GLP-1s, while immediately beneficial, could also inadvertently distort investment priorities, potentially drawing resources away from other critical research areas that may offer less immediate, but equally vital, returns. The intensified pricing pressures for high-demand, high-cost therapies will also continue to shape market dynamics, forcing companies to balance innovation with affordability.

In essence, the pharmaceutical industry stands at a crossroads, buoyed by the unprecedented success of GLP-1s but challenged by the underlying fragility of its broader innovation engine. While these therapies offer immense public health benefits and significant commercial returns, the path forward demands a strategic recalibration, focusing on sustainable diversification, enhanced R&D efficiency, and the disciplined integration of transformative technologies like AI to ensure robust and resilient growth beyond the current "GLP-1 boom." The ability of the industry to navigate these complexities will define its trajectory for the remainder of the decade.

Leave a Reply