Eli Lilly and Company, currently buoyed by the explosive success of its GLP-1 franchise, has announced its intent to acquire Kelonia Therapeutics, a privately held biotechnology company specializing in in vivo CAR-T cell therapies, in a deal potentially valued at up to $7 billion. This significant transaction marks the latest move in Lilly’s aggressive acquisition strategy, aimed at diversifying its pipeline and securing future growth avenues beyond its current blockbusters in obesity and diabetes. The Indianapolis-based pharmaceutical giant is leveraging its burgeoning cash reserves, largely propelled by the tirzepatide franchise, to make strategic bets on innovative, earlier-stage technologies, a stark contrast to Pfizer’s recent post-COVID spending spree which saw the company acquire established, late-stage assets amidst a precipitous decline in its pandemic-era revenues.

Kelonia Therapeutics: Pioneering In Vivo CAR-T Therapy

The acquisition of Kelonia Therapeutics positions Lilly at the forefront of a revolutionary shift in cellular immunotherapy. Chimeric Antigen Receptor (CAR) T-cell therapy has already transformed the treatment landscape for certain blood cancers, offering profound and often durable remissions for patients who have exhausted other options. However, current CAR-T therapies are complex, costly, and time-consuming, requiring ex vivo manufacturing processes where a patient’s T-cells are extracted, genetically modified in a lab, expanded, and then reinfused. This multi-step process limits accessibility and scalability.

Kelonia Therapeutics, founded by experts from Harvard Medical School and Massachusetts General Hospital, is developing an in vivo CAR-T platform designed to overcome these challenges. Their technology aims to deliver the CAR gene directly to T-cells within the patient’s body, eliminating the need for ex vivo manipulation. This is achieved through a precisely engineered lentiviral gene delivery system that specifically targets T-cells, enabling them to express the CAR and attack cancer cells without the need for lymphodepleting chemotherapy in some cases. The promise of in vivo CAR-T lies in its potential to make these life-saving therapies more accessible, affordable, and scalable, transforming them from highly specialized treatments into more broadly applicable therapeutic modalities.

While specific details of Kelonia’s pipeline targets were not extensively disclosed at the time of the announcement, the company’s focus has been on developing therapies for hematological malignancies, with aspirations to extend into solid tumors—a notoriously difficult challenge for CAR-T therapies. The "up to $7 billion" valuation reflects a substantial upfront payment combined with significant milestone payments tied to clinical and regulatory achievements, indicating Lilly’s confidence in Kelonia’s platform technology and its long-term potential, despite the inherent risks of early-stage drug development.

Lilly’s Strategic Imperative: Diversifying for Sustainable Growth

The Kelonia acquisition is not an isolated event but a crucial piece in Lilly’s broader strategy to build a diversified and robust pipeline. With tirzepatide (marketed as Mounjaro for type 2 diabetes and Zepbound for chronic weight management) shattering sales records, Lilly finds itself in an enviable financial position. The company generated an impressive $65.2 billion in revenue in 2025, with tirzepatide alone contributing approximately $36.5 billion. Management has guided for even stronger performance in 2026, projecting revenues between $80 billion and $83 billion. This financial firepower is being strategically deployed to acquire innovative technologies and assets that can drive the "next wave of growth" beyond its highly successful GLP-1 franchise.

Lilly’s M&A activity over the past few years highlights this diversification strategy. In 2024, the company announced the acquisition of Morphic Therapeutic for approximately $3.2 billion, bolstering its immunology and gastrointestinal portfolios with Morphic’s oral integrin inhibitors. This was followed by a series of collaborations and acquisitions in 2025, including deals with Scorpion Therapeutics (up to $2.5 billion for oncology assets), Verve Therapeutics (approximately $1.3 billion for gene editing in cardiovascular disease), and SiteOne Therapeutics (up to $1.0 billion for pain management). Most recently, prior to the Kelonia deal, Lilly signed a potentially $2.75 billion collaboration with Insilico Medicine for a portfolio of AI-originated preclinical oral therapeutics, signaling a commitment to leveraging artificial intelligence in drug discovery.

These deals collectively represent a potential investment of circa $18 billion in announced values, demonstrating Lilly’s aggressive pursuit of cutting-edge science across various therapeutic areas—oncology, immunology, neuroscience, cardiovascular, and gene therapy. The common thread among these acquisitions is their focus on earlier-stage pipeline assets and platform technologies, indicating a long-term investment horizon and a willingness to embrace higher-risk, higher-reward innovation. This approach contrasts sharply with the strategy of acquiring late-stage or already approved assets, which typically offer faster returns but come with higher price tags and potentially limited growth ceilings.

The GLP-1 Engine: A Powerful Catalyst

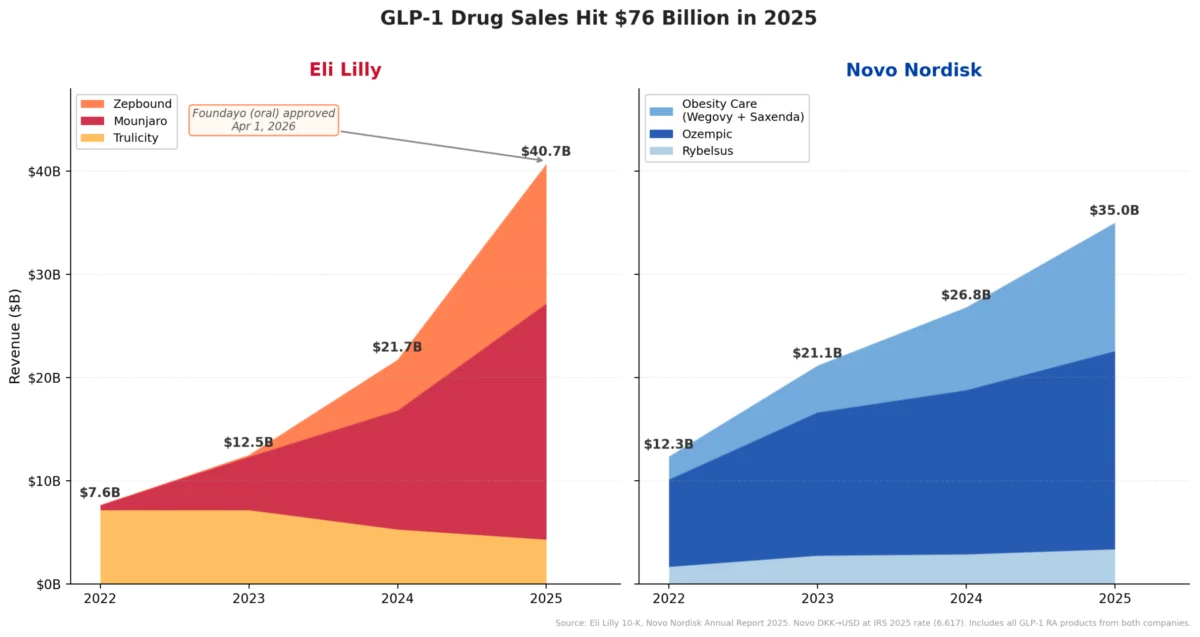

Lilly’s current M&A spree is underpinned by the unprecedented success of its GLP-1 receptor agonist tirzepatide. The drug’s dual agonism of GLP-1 and GIP receptors has demonstrated superior efficacy in both diabetes and weight loss compared to existing GLP-1 monotherapies. This advantage has fueled a remarkable growth trajectory: Lilly’s GLP-1 revenue surged from $7.6 billion in 2022 to an estimated $40.7 billion by the end of 2025. This growth outpaced even Novo Nordisk, the pioneer in the GLP-1 market, whose semaglutide portfolio (Ozempic, Wegovy) climbed from $12.3 billion to $35.0 billion over the same period. Analysts widely project this gap to widen further, with Lilly guiding for continued growth in 2026 while Novo Nordisk has projected a modest 5% to 13% decline in adjusted sales, largely due to intensifying competition and market dynamics.

A pivotal development further solidifying Lilly’s market position occurred on April 1, 2026, when the FDA approved Foundayo (orforglipron), Lilly’s oral GLP-1 for obesity. This approval, granted under the National Priority Voucher program just 50 days after filing, underscores the regulatory urgency and public health significance of novel obesity treatments. Foundayo’s introduction is a game-changer, offering patients a convenient oral alternative to injectable GLP-1s. With Foundayo now shipping through LillyDirect at an accessible price point of $149/month for the lowest dose, and Medicare Part D access anticipated at $50/month by July, Lilly is not only expanding its GLP-1 portfolio but also significantly enhancing market penetration and patient access. This oral formulation is expected to capture a substantial share of the rapidly expanding obesity market, adding another powerful growth vector on top of its already dominant injectable franchise.

Lilly vs. Pfizer: A Tale of Two Deal Waves

The comparison between Lilly’s current M&A strategy and Pfizer’s post-COVID acquisition spree is central to understanding the pharmaceutical industry’s evolving landscape. Both companies found themselves flush with cash from a single blockbuster franchise, leading to ambitious dealmaking. However, the timing and nature of their acquisitions reveal critical differences in strategic execution and market perception.

Pfizer’s spending spree peaked with the $43 billion acquisition of Seagen in late 2023. This deal, along with others like the $11.6 billion Biohaven acquisition (2022) and the $5.4 billion Global Blood Therapeutics acquisition (2022), aimed to rapidly replenish Pfizer’s pipeline and establish a strong oncology presence. However, this aggressive expansion occurred precisely when Pfizer’s COVID-19 windfall from Comirnaty (vaccine) and Paxlovid (antiviral) was in free fall. Full-year revenue collapsed by 42%, from $100.3 billion in 2022 to $58.5 billion in 2023, with Comirnaty sales plummeting 64% and Paxlovid sales falling 58%. Pfizer’s acquisitions, while strategically sound in principle, were perceived by many analysts as an urgent necessity to offset a massive revenue cliff. The company primarily targeted commercial or late-stage assets (Seagen had four approved medicines and a robust antibody-drug conjugate pipeline; Biohaven had approved Nurtec; GBT had approved Oxbryta), seeking immediate revenue streams and established market positions. This "buy now, fix later" approach, while understandable given the revenue imperative, put significant pressure on Pfizer’s balance sheet and necessitated deferring share buybacks until debt could be de-leveraged.

In contrast, Lilly’s M&A spree is unfolding while its primary cash engine, tirzepatide, is still on a steep upward curve. Lilly is acquiring from a position of immense strength, not immediate desperation. Its financial posture is robust, characterized by a growing revenue base, rising margins, $7.3 billion in cash, and $16.8 billion in operating cash flow (as of FY2025). While it carries $40.9 billion in long-term debt, this is seen as manageable given its explosive growth. Lilly’s focus on earlier-stage, platform-based acquisitions (Morphic’s oral integrins, Scorpion’s precision oncology, Verve’s gene editing, Kelonia’s in vivo CAR-T) suggests a long-term strategic vision to cultivate future blockbusters rather than simply plugging immediate revenue gaps. This approach, while inherently riskier due to the high failure rate of early-stage assets, offers the potential for much higher returns and a more sustainable growth trajectory if successful.

The market has responded decisively to these differing strategies. As of April 2026, Lilly’s market capitalization ranges between $830 billion and $880 billion, reflecting immense investor confidence in its growth prospects and strategic foresight. Pfizer, by contrast, holds a market cap of approximately $155 billion, indicative of the challenges it faces in rebuilding investor trust and demonstrating sustainable growth in a post-COVID era.

Industry Reactions and Future Outlook

The pharmaceutical industry and financial analysts are largely viewing Lilly’s M&A strategy with optimism, albeit with an acknowledgement of the inherent risks. Analysts have praised Lilly’s proactive approach to reinvesting its GLP-1 windfall into innovative, high-potential areas. The Kelonia acquisition, in particular, is seen as a bold, forward-looking move into the highly competitive but potentially transformative field of gene and cell therapy.

However, challenges remain. Integrating multiple diverse companies and technologies, managing complex clinical pipelines, and navigating the intense competitive landscape in fields like CAR-T therapy will require significant operational excellence. The success of Lilly’s acquired assets, particularly earlier-stage platforms like Kelonia’s, is far from guaranteed. Clinical trial failures, manufacturing hurdles, and market access issues could temper expectations. Furthermore, while Lilly is diversifying, the sheer scale of its GLP-1 revenue means that any significant slowdown in that franchise could still create pressure.

Despite these challenges, Lilly’s current trajectory positions it as one of the most dynamic and strategically astute players in the pharmaceutical industry. By investing heavily in cutting-edge science and leveraging its formidable financial strength, Lilly is attempting to build a multi-faceted pipeline that can sustain its growth well into the next decade. The Kelonia acquisition is a testament to this ambition, signaling Lilly’s intent to be a leader not just in metabolic diseases but also in the next generation of highly innovative, potentially curative therapies. The company’s Q1 2026 results, due on April 30, will provide further insight into the continued momentum of its GLP-1 franchise and its capacity to fuel this ambitious, transformative journey.

Leave a Reply