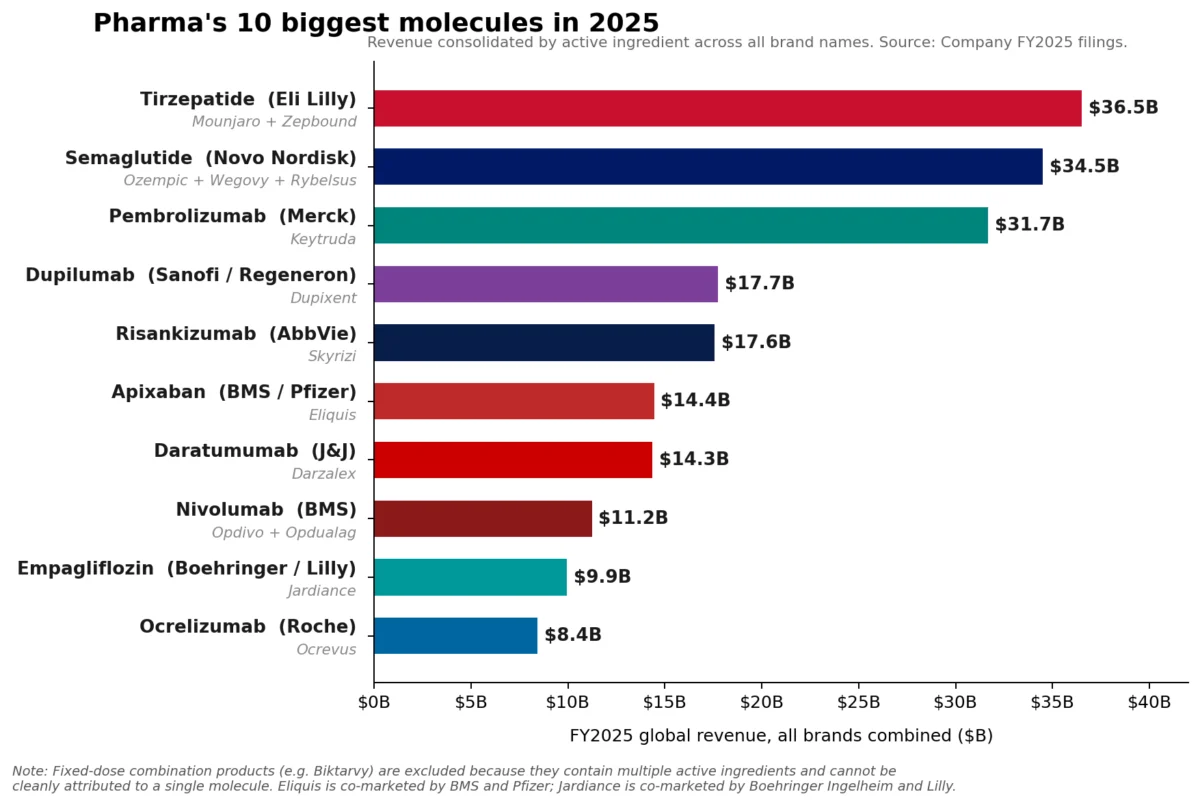

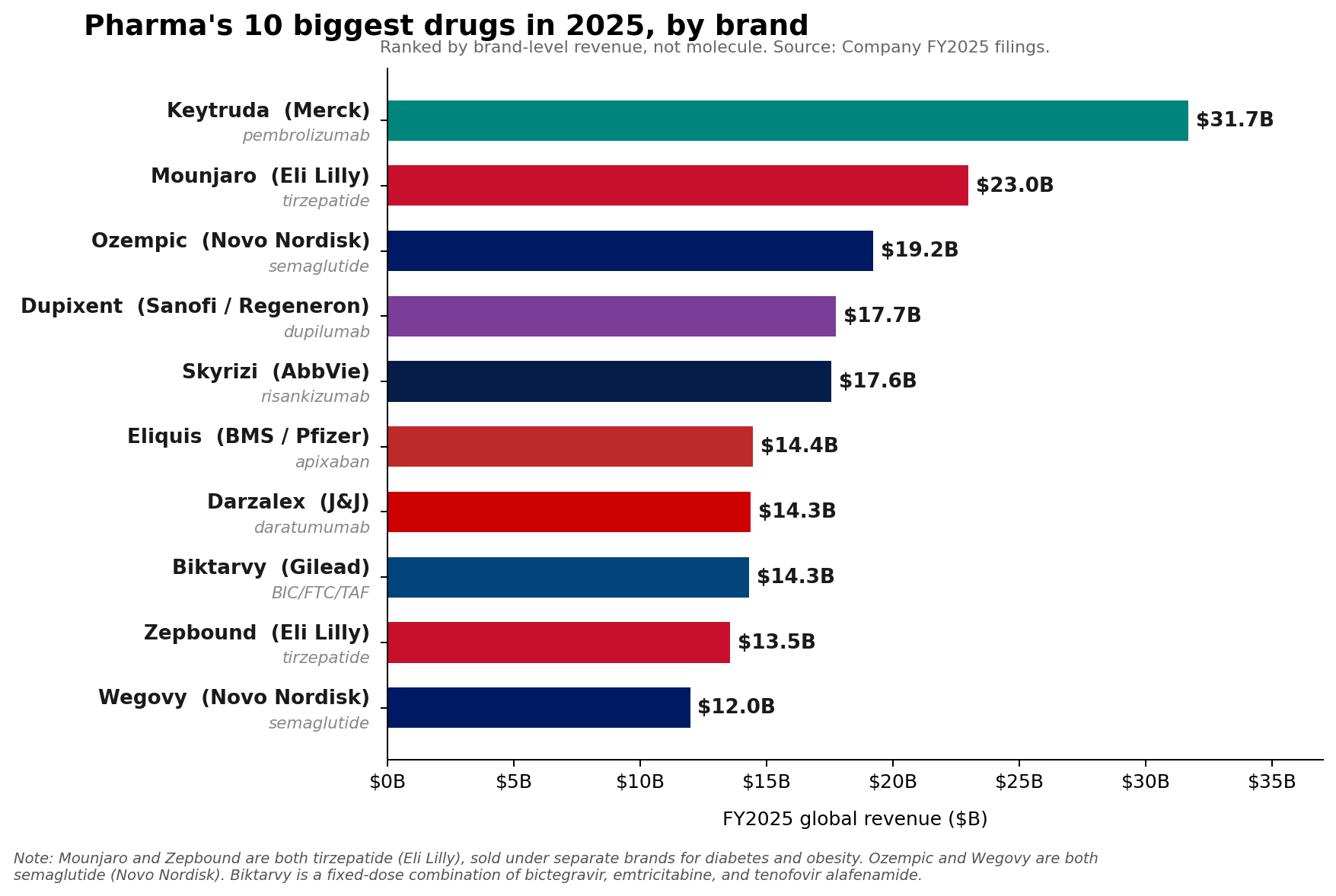

Merck’s Keytruda (pembrolizumab), a cornerstone of modern oncology, maintained its position as the pharmaceutical industry’s leading brand in Fiscal Year 2025, recording an impressive $31.7 billion in sales. This robust performance underscored its continued dominance in the lucrative immuno-oncology market. However, a significant shift in the broader pharmaceutical landscape has occurred, with a new class of metabolic medicines – specifically, the glucagon-like peptide-1 (GLP-1) receptor agonists – collectively surpassing Keytruda at the fundamental molecule level. Eli Lilly’s tirzepatide franchise, comprising the diabetes medication Mounjaro and the weight-loss drug Zepbound, achieved a combined revenue of approximately $36.5 billion in 2025. Similarly, Novo Nordisk’s semaglutide franchise, which includes Ozempic, Wegovy, and Rybelsus, collectively generated roughly $34.5 billion. This bifurcation between brand and molecule-level leadership signals a dynamic evolution within the pharmaceutical sector, driven by innovation in metabolic health and a continued strong showing from immunology.

Keytruda’s Enduring Brand Power Amidst Shifting Tides

Keytruda’s consistent growth, evidenced by a 7% increase in 2025 sales, highlights Merck’s strategic prowess in extending the lifecycle of its blockbuster drug. Pembrolizumab, a programmed death-1 (PD-1) blocking antibody, has revolutionized the treatment of numerous cancers, including melanoma, lung cancer, and various solid tumors, since its initial approval. Its mechanism of action, which involves boosting the body’s immune response against cancer cells, has led to its broad adoption and expansion into over 40 indications across various cancer types. This extensive label expansion has been a critical factor in maintaining its revenue trajectory.

Merck’s proactive approach to lifecycle management includes developing new indications and introducing alternative formulations, such as the subcutaneous version of Keytruda, QLEX. These efforts are designed to enhance convenience for patients and clinicians, potentially broadening its market reach and reinforcing patient adherence. However, the looming challenge for Merck is the approaching loss of exclusivity (LOE) for Keytruda in the coming years. Patent expirations typically open the door for generic or biosimilar competition, which can lead to significant revenue erosion. Merck CEO Rob Davis has publicly characterized this anticipated decline as "more of a hill than a cliff," indicating a strategic plan to mitigate the impact. This strategy likely involves maximizing current indications, securing new approvals, and leveraging combination therapies to maintain market share for as long as possible before biosimilars exert their full pressure. Despite these assurances, Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion came in below Wall Street expectations, underscoring investor concerns about the post-Keytruda future. The company is actively investing in its pipeline across oncology, vaccines, and other therapeutic areas to diversify its revenue streams and prepare for this pivotal transition.

The Ascendancy of GLP-1 Agonists: A Metabolic Revolution

The remarkable ascent of tirzepatide and semaglutide marks a paradigm shift in pharmaceutical sales, reflecting the immense global burden of metabolic diseases. Tirzepatide, a dual GIP (glucose-dependent insulinotropic polypeptide) and GLP-1 receptor agonist developed by Eli Lilly, has demonstrated superior efficacy in both Type 2 Diabetes management and weight reduction. Its franchise, comprising Mounjaro (primarily for diabetes) and Zepbound (specifically for weight loss), achieved nearly $36.5 billion in 2025 revenue. Mounjaro, launched with significant anticipation, quickly became a frontrunner, securing $22.965 billion in sales. Zepbound, approved later, rapidly scaled to $13.542 billion, testament to the unmet need in the obesity market.

Novo Nordisk’s semaglutide, a GLP-1 receptor agonist, has similarly transformed the treatment landscape. Its portfolio, including Ozempic (for Type 2 Diabetes), Wegovy (for chronic weight management), and Rybelsus (an oral formulation for Type 2 Diabetes), collectively reached approximately $34.5 billion in 2025. Ozempic has been a long-standing success, while Wegovy’s launch significantly expanded the market for medical weight loss solutions. The explosive growth of both tirzepatide and semaglutide underscores the profound impact these drugs are having on public health. Obesity and Type 2 Diabetes are global epidemics, with rising prevalence rates contributing to a cascade of associated health complications and enormous healthcare costs. These GLP-1 class drugs offer not just glycemic control but also significant cardiovascular benefits and weight loss, addressing multiple facets of these complex conditions. The convenience and efficacy of these treatments have driven unprecedented demand, challenging manufacturing capacities and leading to supply chain discussions globally.

Orforglipron: The Oral Wildcard and Future of Obesity Management

The competitive landscape in the obesity market is poised for further disruption with the introduction of oral GLP-1 therapies. Eli Lilly’s Foundayo (orforglipron), a once-daily oral small-molecule GLP-1 receptor agonist, emerged as a significant strategic wildcard for 2026. Licensed by Lilly from Chugai in 2018, orforglipron received FDA approval on April 1, 2026, and became commercially available as of April 9. This swift market entry of an oral option is a critical development, as it addresses a key barrier to broader adoption of weight-loss medications: the need for injections.

While analysts diverge on orforglipron’s immediate revenue potential for 2026, its strategic importance is undeniable. Lilly’s robust guidance of $80 billion to $83 billion in 2026 revenue, largely propelled by Mounjaro and Zepbound, indicates confidence in its metabolic portfolio. Orforglipron’s approval came after the first quarter of 2026 ended, meaning its financial impact will be more pronounced in the latter half of the year. Mounjaro and Zepbound entered 2026 with substantial sales bases of $22.965 billion and $13.542 billion, respectively, positioning them to continue driving the largest absolute revenue gains. However, orforglipron’s oral formulation offers a distinct advantage in terms of patient preference and accessibility, potentially expanding the overall market significantly by attracting individuals hesitant to use injectable medications. This could be a game-changer for long-term market penetration and adherence, even if initial revenue figures do not immediately eclipse its injectable predecessors.

Citeline’s 2026 Pharma R&D Annual Review reinforces the burgeoning interest in anti-obesity treatments, noting a "gut-busting 30.7%" expansion in the anti-obesity pipeline to 588 active compounds, contrasting with an overall contraction in the pharmaceutical pipeline. This surge in R&D activity indicates a long-term commitment from the industry to capitalize on this growing market. Orforglipron is entering a market that is not only expanding rapidly but also one where Lilly already holds a dominant position with two blockbuster injectable products. The key challenge and opportunity for orforglipron will be to carve out its own space by leveraging the convenience of its oral delivery, potentially converting a new segment of the population to medical weight management.

Novo Nordisk is also actively pursuing the oral GLP-1 space. While its older oral semaglutide, Rybelsus, saw a 2% decline at constant exchange rates (CER) in 2025, the company launched a newer, higher-dose oral Wegovy in January 2026. Novo Nordisk expects to broaden the rollout of oral Wegovy throughout 2026 and introduce a 7.2 mg dose in various countries, alongside the recent U.S. launch of Wegovy HD. However, Novo Nordisk’s own 2026 guidance projects adjusted sales growth of negative 5% to negative 13% at CER, reflecting anticipated pricing pressure, increased competition, and U.S. access dynamics. This suggests that while oral semaglutide is strategically vital for widening market access and patient choice, it may not be the primary driver of immediate revenue growth in 2026 for Novo Nordisk, as the company navigates a more competitive landscape.

Sustained Momentum in Immunology and Oncology

While the metabolic market commands significant attention, other specialty areas, particularly immunology and oncology, continue to demonstrate robust growth and contribute substantially to the pharmaceutical leaderboard. These therapeutic areas are characterized by chronic conditions requiring long-term treatment and continuous innovation.

AbbVie’s immunology engine exemplifies this trend, with its key assets Skyrizi (risankizumab) and Rinvoq (upadacitinib) achieving impressive sales in 2025. Skyrizi, a selective IL-23 inhibitor for inflammatory conditions such as psoriasis, psoriatic arthritis, and Crohn’s disease, reached $17.562 billion in sales. Rinvoq, a JAK inhibitor approved for conditions like rheumatoid arthritis, psoriatic arthritis, atopic dermatitis, and ulcerative colitis, generated $8.304 billion. Together, these two drugs amassed $25.866 billion, representing approximately 42% of AbbVie’s total net revenue of $61.160 billion for the year. AbbVie’s guidance for 2026 adjusted EPS of $14.37 to $14.57 further underscores the expected continued strength of this immunology portfolio. The company has successfully diversified its revenue streams following the patent expiration of Humira, demonstrating the durability of its immunology franchise.

Sanofi’s Dupixent (dupilumab), an IL-4Rα antagonist used for atopic dermatitis, asthma, and chronic rhinosinusitis with nasal polyps, also showed formidable growth, rising to €15.714 billion (approximately $17 billion, depending on exchange rates) in 2025. Novartis’s Kisqali (ribociclib), a CDK4/6 inhibitor for breast cancer, climbed a significant 58% to $4.783 billion, indicating strong uptake in the oncology space. Johnson & Johnson reported that its 2025 Innovative Medicine growth was primarily fueled by products including Darzalex (daratumumab), a CD38-directed monoclonal antibody for multiple myeloma, and Tremfya (guselkumab), an IL-23 inhibitor for psoriasis and psoriatic arthritis.

These performances are consistent with broader industry trends. Citeline’s 2026 R&D review highlighted that immunologicals were one of the few large therapeutic areas that still expanded, growing 20.6% in terms of pipeline count, even as the overall pharmaceutical pipeline experienced a slight contraction. This indicates sustained investment and innovation in addressing autoimmune and inflammatory diseases. The market for these conditions is vast and growing, driven by improved diagnostic capabilities and the development of highly effective targeted therapies. The chronic nature of these diseases ensures long-term patient populations and recurring revenue streams for these established franchises.

Broader Implications and Future Outlook

The pharmaceutical industry is undergoing a significant transformation, characterized by several key dynamics. The shift in molecule-level leadership from a single oncology blockbuster like Keytruda to a combined force of metabolic therapies underscores the industry’s responsiveness to evolving global health challenges. While oncology remains a critical and innovative area, the sheer scale of the diabetes and obesity epidemics is creating unprecedented market opportunities for GLP-1 agonists.

The emergence of oral formulations like orforglipron and oral Wegovy represents a crucial step in making highly effective treatments more accessible and convenient, potentially expanding patient populations far beyond those willing or able to manage injectable therapies. This shift will intensify competition, drive innovation in drug delivery, and put pressure on pricing models, especially as more players enter the crowded metabolic space.

Meanwhile, the sustained growth of immunology and certain oncology franchises demonstrates the resilience and continued importance of specialty medications for chronic and life-threatening conditions. These areas benefit from ongoing research and development, leading to new mechanisms of action and improved patient outcomes. The investment in these fields, as evidenced by expanding R&D pipelines, suggests they will remain significant revenue drivers for years to come.

For pharmaceutical companies, adapting to these shifts requires strategic foresight. Merck’s "hill not a cliff" approach to Keytruda’s LOE exemplifies the need for proactive lifecycle management and pipeline diversification. Lilly and Novo Nordisk are racing to dominate the metabolic market, with both injectable and oral formulations, while AbbVie, Sanofi, J&J, and Novartis continue to leverage strong positions in immunology and oncology. The future pharmaceutical leaderboard will likely be a more diversified landscape, with robust franchises in metabolic health, immunology, and oncology competing for the top spots, reflecting a dynamic and evolving global healthcare environment. The industry’s ability to innovate, adapt to patient needs, and navigate complex market dynamics will determine which companies will lead in this new era of pharmaceutical sales.

Leave a Reply