Eli Lilly and Company, a pharmaceutical giant currently experiencing unprecedented growth driven by its blockbuster GLP-1 agonists, has announced an agreement to acquire Kelonia Therapeutics, a developer of in vivo CAR-T cell therapies, in a deal potentially valued at up to $7 billion. This strategic acquisition marks Lilly’s latest move in an aggressive M&A spree, signaling a clear intent to diversify its pipeline and secure future growth drivers beyond its highly successful obesity and diabetes franchises. The company’s proactive stance invites comparisons to Pfizer’s recent post-COVID spending spree, which saw the latter acquire Seagen for $43 billion, amidst a dramatic decline in its pandemic-era revenue. The critical question for industry observers is whether Lilly’s current deal-making strategy, fueled by a surging revenue stream, can navigate the pitfalls that have challenged Pfizer’s post-acquisition trajectory.

Lilly’s Strategic Dive into CAR-T with Kelonia

The acquisition of Kelonia Therapeutics is a significant statement of intent for Eli Lilly, moving the company deeper into the burgeoning field of cell and gene therapy, specifically in vivo CAR-T. While traditional CAR-T therapies involve extracting a patient’s T-cells, genetically modifying them ex vivo to target cancer cells, and then reinfusing them, Kelonia’s approach focuses on in vivo gene delivery. This innovative method aims to modify T-cells directly within the patient’s body, potentially simplifying the treatment process, reducing manufacturing complexity, and broadening patient access.

The deal, structured with an upfront payment and a series of milestone-based payments that could push the total value to $7 billion, underscores the high premium placed on cutting-edge technologies that promise to revolutionize cancer treatment. Kelonia’s lead program, currently in Phase 1 development, targets specific hematological malignancies. The potential for an in vivo CAR-T platform to address solid tumors, a challenge for existing CAR-T therapies, also represents a significant upside. By integrating Kelonia’s platform, Lilly aims to establish a formidable presence in oncology, complementing its existing portfolio and providing a long-term growth vector in a highly competitive therapeutic area.

The GLP-1 Engine: Fueling Lilly’s Ambitious Expansion

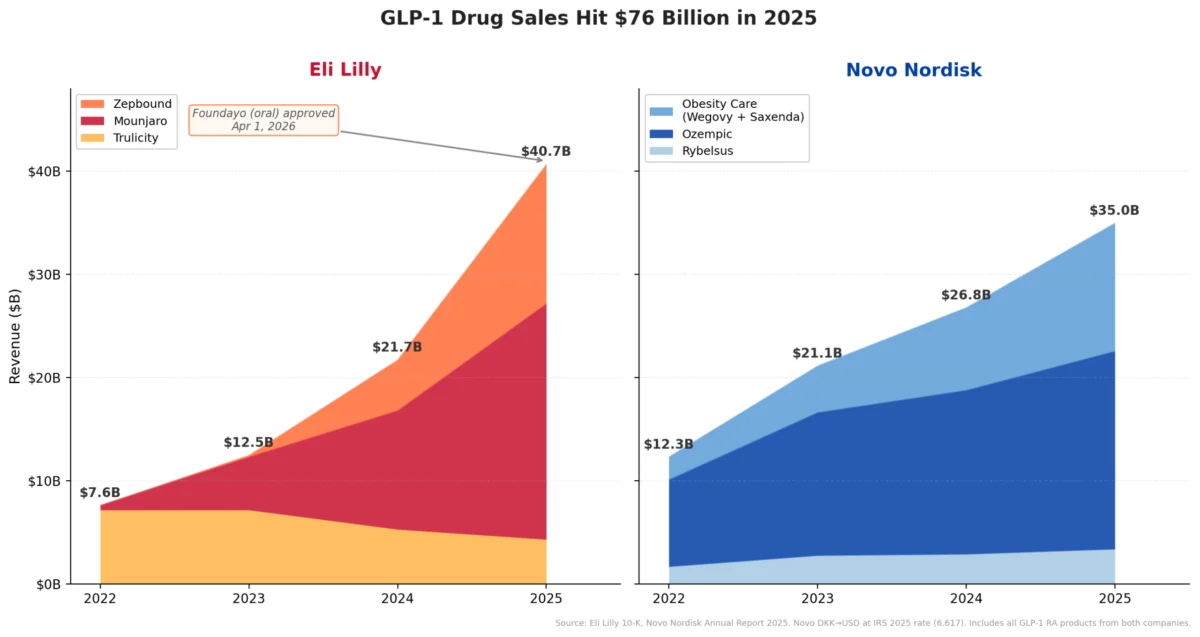

Lilly’s current acquisition spree is largely financed by the phenomenal success of its tirzepatide franchise, marketed as Mounjaro for type 2 diabetes and Zepbound for chronic weight management. This dual-agonist GLP-1/GIP receptor agonist has rapidly ascended to blockbuster status, driving an unprecedented surge in Lilly’s revenue. In fiscal year 2025, tirzepatide alone generated approximately $36.5 billion of Lilly’s $65.2 billion total revenue, with Mounjaro contributing an estimated $23.0 billion and Zepbound $13.5 billion. This represented a more than fivefold growth for the tirzepatide franchise in just three years.

The company’s financial outlook remains robust, with management guiding for an impressive $80 billion to $83 billion in total revenue for 2026. This projection is further bolstered by the recent accelerated approval of Foundayo (orforglipron), Lilly’s oral GLP-1 agonist for obesity. Approved by the FDA on April 1, 2026, under the National Priority Voucher program, Foundayo’s rapid authorization (just 50 days post-filing) highlights its strategic importance. The drug’s accessibility, with initial shipments through LillyDirect at $149/month for the lowest dose and anticipated Medicare Part D access at $50/month by July, positions it as a significant oral growth vector complementing the injectable tirzepatide franchise. This multi-pronged attack on the massive obesity and diabetes markets provides Lilly with substantial cash flow and a durable competitive advantage, differentiating its deal-making environment from Pfizer’s.

Comparatively, Lilly’s GLP-1 revenue trajectory has been steeper than that of its pioneer competitor, Novo Nordisk. Lilly’s GLP-1 portfolio surged from $7.6 billion in 2022 to $40.7 billion in 2025. In the same period, Novo Nordisk’s semaglutide portfolio (Ozempic, Wegovy, Rybelsus) climbed from $12.3 billion to $35.0 billion. While both companies have seen remarkable growth, Lilly’s current guidance projects continued expansion in 2026, whereas Novo Nordisk has projected a modest 5% to 13% decline in adjusted sales for the same period, indicating a potential widening of the revenue gap in Lilly’s favor. This strong, sustained revenue growth forms the bedrock of Lilly’s aggressive investment strategy.

Beyond GLP-1s: Diversifying the Pipeline for Future Resilience

Lilly’s acquisition strategy is not solely focused on oncology. The Kelonia deal is part of a broader, multi-faceted approach to diversify its therapeutic areas and technological platforms. In recent years, Lilly has committed approximately $18 billion in potential deal value across several strategic acquisitions and collaborations:

- Morphic Therapeutic (2024, approximately $3.2 billion): Acquired for its oral integrin inhibitors, deepening Lilly’s immunology and gastroenterology portfolio with a Phase 2 asset.

- Scorpion Therapeutics (2025, up to $2.5 billion): A collaboration focused on developing precision oncology drugs, including a Phase 1/2 asset.

- Verve Therapeutics (2025, approximately $1.3 billion): A partnership in gene editing for cardiovascular diseases, involving a Phase 1b program.

- SiteOne Therapeutics (2025, up to $1.0 billion): Focused on pain management with a Phase 2-ready asset.

- Insilico Medicine (2026, up to $2.75 billion): A significant collaboration leveraging artificial intelligence for drug discovery, aiming to generate a portfolio of AI-originated preclinical oral therapeutics. This deal highlights Lilly’s embrace of advanced technologies to accelerate the discovery of novel compounds.

These acquisitions and collaborations collectively demonstrate a clear strategy: to invest in early to mid-stage assets and innovative platforms across multiple therapeutic areas, from immunology and oncology to gene editing and AI-driven drug discovery. This approach aims to build a robust, diversified pipeline that can sustain growth long after the peak of its current GLP-1 franchise, mitigating reliance on a single therapeutic class.

Pfizer’s Post-COVID Reckoning: A Cautionary Tale?

The narrative of Lilly’s current expansion inevitably draws parallels with Pfizer’s recent trajectory, albeit with critical distinctions. Pfizer experienced an unprecedented windfall during the COVID-19 pandemic, with its mRNA vaccine Comirnaty and antiviral Paxlovid generating tens of billions in revenue. In 2022, Pfizer’s full-year revenue reached an astounding $100.3 billion, largely propelled by these two products, with Comirnaty bringing in $37.8 billion and Paxlovid $18.9 billion. This surge in cash enabled Pfizer to embark on its own aggressive acquisition strategy.

However, the rapid decline in demand for COVID-19 products led to a dramatic revenue collapse. In 2023, Pfizer’s full-year revenue plummeted by 42% to $58.5 billion, with Comirnaty sales dropping by 64% and Paxlovid by 58%. This precipitous decline occurred precisely as Pfizer was finalizing its largest acquisition, the $43 billion deal for Seagen, an oncology biotechnology company.

Pfizer’s deal wave, totaling approximately $60 billion across headline deals, aimed to diversify its portfolio and establish new growth drivers, particularly in oncology, following the impending patent cliffs for several key drugs and the sharp drop in COVID-19 revenue. Key acquisitions included:

- Biohaven Pharmaceuticals (2022, approximately $11.6 billion): Acquired for Nurtec ODT, an approved migraine drug.

- Global Blood Therapeutics (2022, approximately $5.4 billion): Acquired for Oxbryta, an approved treatment for sickle cell disease.

- Seagen (2023, approximately $43 billion): The largest acquisition, bringing four approved antibody-drug conjugate (ADC) oncology medicines and a deep pipeline.

While these acquisitions were strategically sound in principle, their timing coincided with a severe downturn in Pfizer’s core revenue engine. This created significant financial pressure, leading to a deferral of share buybacks until the balance sheet could be de-levered post-Seagen. The market’s reaction has been palpable, with Pfizer’s market capitalization in April 2026 standing at approximately $155 billion, a stark contrast to Lilly’s $830 billion-$880 billion.

Key Differences in Playbook: Lilly vs. Pfizer

The comparison between Lilly and Pfizer reveals distinct strategic playbooks, particularly concerning the timing and nature of their acquisition sprees:

-

Cash Engine Trajectory:

- Lilly: Is making its significant acquisitions while its cash engine, the tirzepatide franchise, is still on a steep upward curve and expected to continue growing. The introduction of Foundayo provides an additional, robust growth vector. This allows Lilly to invest from a position of strength and sustained profitability.

- Pfizer: Made its major acquisitions after its primary cash engines (Comirnaty and Paxlovid) had peaked and were already in free fall. This meant Pfizer was deploying capital from a rapidly diminishing revenue base, creating immediate pressure to integrate and derive value from acquired assets to offset core business declines.

-

Stage of Acquired Assets:

- Lilly: Has primarily targeted earlier-stage pipeline assets and platform bets (e.g., Kelonia’s Phase 1 in vivo CAR-T, Morphic’s Phase 2 integrin inhibitors, Insilico’s AI platform). This approach suggests a long-term investment in foundational technologies and future innovation, with a higher risk but potentially higher reward profile over a longer horizon.

- Pfizer: Focused on acquiring commercial or late-stage assets (e.g., Seagen’s four approved ADCs, Biohaven’s Nurtec, GBT’s Oxbryta). This strategy aimed for more immediate revenue generation and diversification to fill the void left by declining COVID-19 sales, prioritizing near-term impact.

-

Financial Posture:

- Lilly: Operates with a strong and growing revenue base, rising margins, and substantial operating cash flow ($16.8 billion in FY2025). While it carries significant long-term debt ($40.9 billion), its robust cash generation provides flexibility for strategic investments.

- Pfizer: Faced a significant reduction in operating cash flow ($11.7 billion in FY2025, down from pandemic highs) and had to defer capital return to shareholders to de-lever its balance sheet after the Seagen acquisition. Its financial position became more constrained, necessitating a rapid return on investment from its acquired assets.

-

Market Perception and Valuation:

- Lilly: Enjoys immense investor confidence, reflected in its current market capitalization of $830 billion-$880 billion (April 2026). The market is betting on Lilly’s sustained growth and successful pipeline diversification.

- Pfizer: Has experienced a significant contraction in its market valuation to approximately $155 billion, reflecting investor concerns about its revenue decline, the scale of its debt, and the time required for acquired assets to fully contribute.

Broader Impact and Implications

Lilly’s strategy is not without risks. The integration of multiple early-stage companies and platforms requires significant R&D investment, managerial oversight, and a tolerance for clinical trial failures. The CAR-T field, while promising, is highly competitive, complex, and expensive, with challenges in manufacturing, patient access, and managing potential severe side effects. The success of Kelonia’s in vivo CAR-T platform is still contingent on robust clinical data and regulatory approval. Similarly, the long-term impact of AI in drug discovery, while transformative, is still being fully realized.

However, by investing in diverse, cutting-edge technologies and therapeutic areas while its primary revenue engine is thriving, Lilly appears to be building a more resilient and future-proof pipeline. The company is strategically leveraging its current success to sow the seeds for its next wave of growth, rather than scrambling to fill a sudden revenue void. This proactive approach allows for a more deliberate integration process, potentially reducing the immediate pressure for acquired assets to perform, unlike Pfizer’s more reactive strategy.

Looking Ahead: Can Lilly Maintain Momentum?

As Eli Lilly prepares to release its Q1 2026 results on April 30, the market will be keenly watching for continued strong performance from its GLP-1 franchise and further details on its pipeline development. The success of its multi-billion-dollar deal spree hinges on the effective integration of these new assets, the advancement of their clinical programs, and ultimately, the commercialization of novel therapies.

Lilly’s current trajectory suggests a deliberate attempt to learn from past industry experiences, including perhaps Pfizer’s post-COVID challenges. By investing aggressively from a position of strength, targeting innovative, earlier-stage assets, and diversifying its technological bets, Lilly aims to create a sustainable growth model. The ability of Lilly to successfully translate these strategic investments into a diversified, high-value product portfolio will determine if its ambitious deal spree truly avoids the fate of its pharmaceutical peer and cements its position as a leader in the next generation of therapeutics.

Leave a Reply