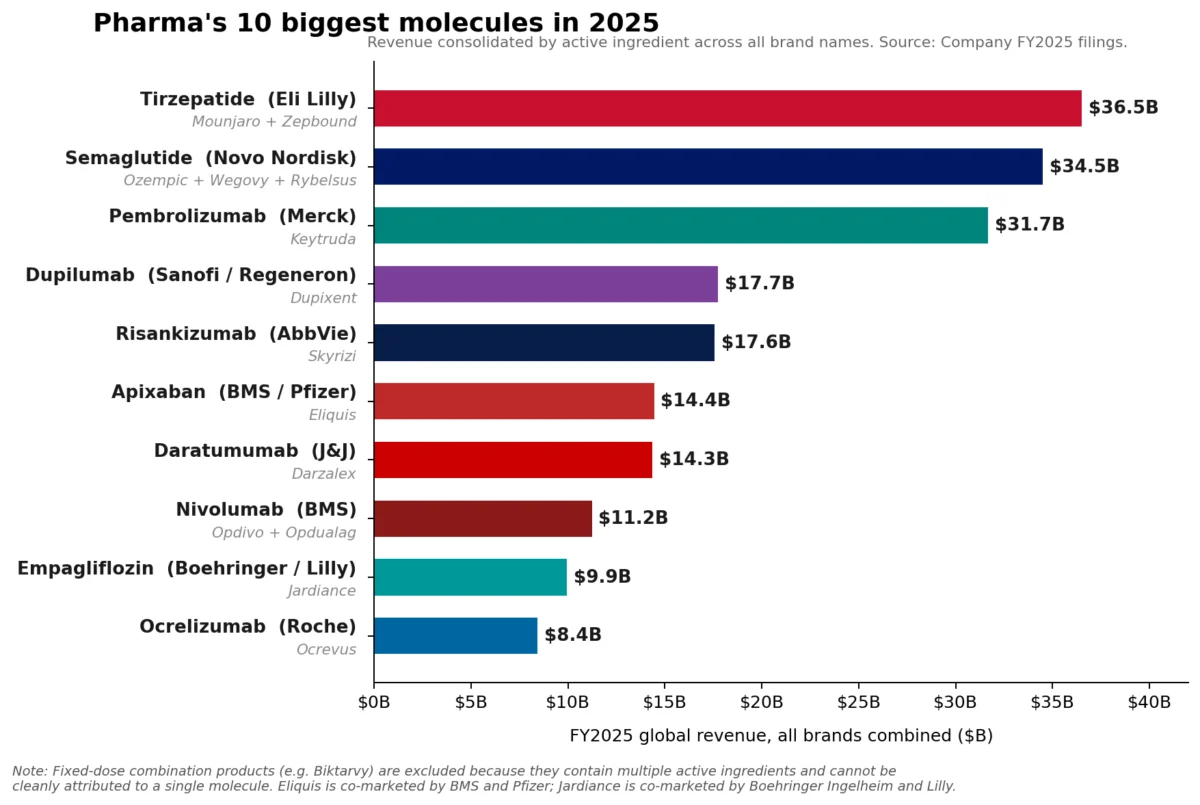

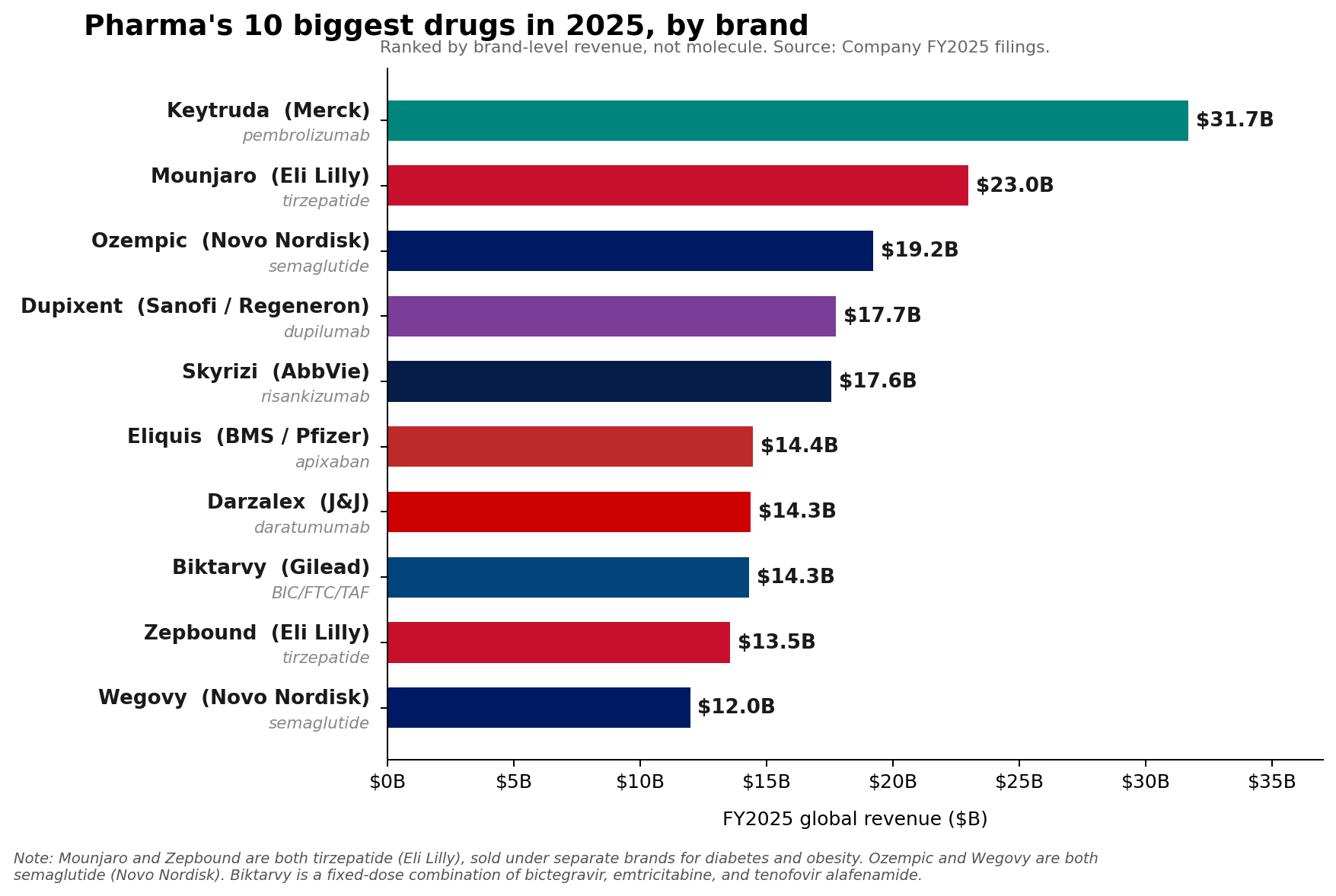

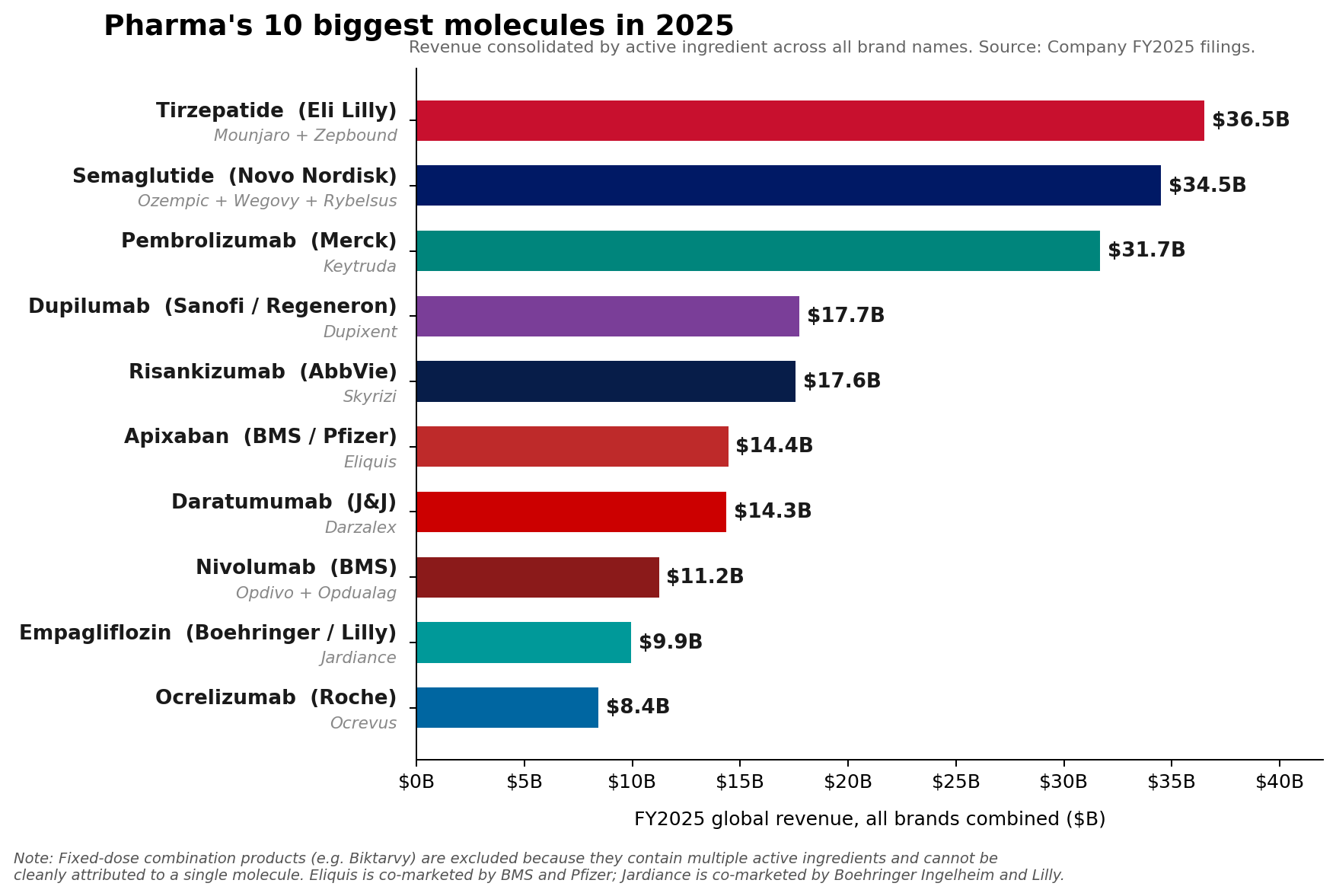

The pharmaceutical industry’s financial landscape underwent a significant transformation in fiscal year 2025, revealing a nuanced shift in leadership despite the enduring strength of established powerhouses. While Merck’s oncology blockbuster, Keytruda (pembrolizumab), steadfastly maintained its position as the top-selling pharmaceutical brand globally, racking up an impressive $31.7 billion in sales, a deeper analysis at the molecule level indicates a new guard has emerged. Eli Lilly’s tirzepatide franchise, comprising the diabetes and weight-loss medications Mounjaro and Zepbound, collectively surged to approximately $36.5 billion in revenue. Close behind, Novo Nordisk’s semaglutide franchise, encompassing Ozempic, Wegovy, and Rybelsus, reached an estimated $34.5 billion, signaling a definitive rise of GLP-1 receptor agonists to the apex of pharmaceutical sales. This reordering underscores a pivotal moment for the industry, reflecting both the continued robust performance of groundbreaking oncology treatments and the unprecedented, rapidly expanding market for metabolic therapies.

The Shifting Landscape: Brand vs. Molecule

The distinction between a "brand" and a "molecule" in pharmaceutical sales is critical for understanding this market evolution. A brand, such as Keytruda, represents a single commercial product, even if it has multiple indications. A molecule, however, aggregates all products containing the same active pharmaceutical ingredient, regardless of their individual brand names or therapeutic uses. For instance, tirzepatide is the active molecule found in both Mounjaro (primarily for type 2 diabetes) and Zepbound (specifically for weight management). Similarly, semaglutide is the core molecule for Ozempic (diabetes), Wegovy (weight loss), and Rybelsus (oral diabetes treatment).

Keytruda’s retention of the top brand slot for FY2025, with its $31.7 billion in sales, speaks volumes about its continued dominance in the oncology space. Approved for over 30 indications across various cancers, Keytruda has revolutionized cancer treatment, particularly in immuno-oncology. Its 7% growth in 2025 demonstrates ongoing clinical utility and market penetration, despite increasing competition and the sheer scale of its existing sales base. Merck has strategically extended the franchise’s lifecycle through new indications and innovative formulations like subcutaneous Keytruda QLEX, aiming to sustain its trajectory.

However, the combined might of the GLP-1 agonists at the molecule level represents a seismic shift. Tirzepatide’s combined sales from Mounjaro ($22.965 billion) and Zepbound ($13.542 billion) pushed it past Keytruda’s single-brand revenue, reaching roughly $36.5 billion. Novo Nordisk’s semaglutide, with its diversified portfolio, also surpassed Keytruda, achieving approximately $34.5 billion. This surge highlights the explosive demand for effective treatments in type 2 diabetes and, more dramatically, in the burgeoning obesity market, which is rapidly redefining pharmaceutical priorities and revenue streams.

Keytruda’s Enduring Legacy and Looming Transition

Merck’s Keytruda, a monoclonal antibody targeting the PD-1 pathway, has been a cornerstone of the company’s financial success for nearly a decade. Its consistent growth, including the 7% increase in 2025, underscores its broad applicability and significant clinical benefits across a multitude of cancer types, from melanoma and lung cancer to head and neck squamous cell carcinoma. The continuous pursuit of new indications and strategic lifecycle management, such as the development of a subcutaneous formulation (Keytruda QLEX), are crucial tactics employed by Merck to maximize the drug’s revenue potential as long as possible. A subcutaneous option offers convenience for patients and healthcare providers, potentially expanding access and adherence.

Despite its current stronghold, the looming specter of Keytruda’s loss of exclusivity (LOE) in the coming years, particularly around 2028 in the United States, casts a long shadow over Merck’s future financial projections. Biosimilar competition is anticipated to erode a significant portion of its sales, posing one of the largest patent cliffs in pharmaceutical history. Merck CEO Rob Davis has publicly characterized this anticipated drop-off as "more of a hill than a cliff," suggesting that the company is prepared to manage the transition through pipeline diversification, strategic acquisitions, and the aforementioned lifecycle management efforts. However, the market’s skepticism was reflected in Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion, which came in below Wall Street expectations, indicating investor concern about the post-Keytruda era. The company is actively investing in new oncology assets, vaccines, and other therapeutic areas to mitigate the impending revenue decline.

The Meteoric Rise of GLP-1 Agonists

The ascent of GLP-1 receptor agonists like tirzepatide and semaglutide is arguably the most compelling narrative in recent pharmaceutical history. Originally developed for type 2 diabetes, these drugs have demonstrated remarkable efficacy in weight management, unlocking a vast and underserved patient population struggling with obesity and its related comorbidities. The success of Mounjaro and Zepbound for Lilly, and Ozempic and Wegovy for Novo Nordisk, is a testament to both their clinical effectiveness and the immense global health burden of metabolic diseases.

Mounjaro, initially approved for type 2 diabetes, quickly gained traction due to its superior glucose control and impressive weight loss benefits. Zepbound, specifically approved for chronic weight management, capitalized on this efficacy, extending tirzepatide’s reach into the burgeoning obesity market. The combined sales of these two brands in 2025 firmly established tirzepatide as the leading molecule by revenue, highlighting Lilly’s strategic success in a highly competitive therapeutic area.

Novo Nordisk’s semaglutide franchise has similarly capitalized on this trend. Ozempic, a weekly injectable for type 2 diabetes, and Wegovy, a higher-dose formulation for weight loss, have become household names. Rybelsus, the first oral GLP-1 receptor agonist, offered a convenient alternative for diabetes patients. The combined sales of these semaglutide products underscore the widespread adoption and therapeutic value recognized by both patients and healthcare providers. The global obesity market alone is projected to reach hundreds of billions of dollars in the coming years, driven by increasing prevalence rates and a growing understanding of obesity as a chronic disease requiring medical intervention.

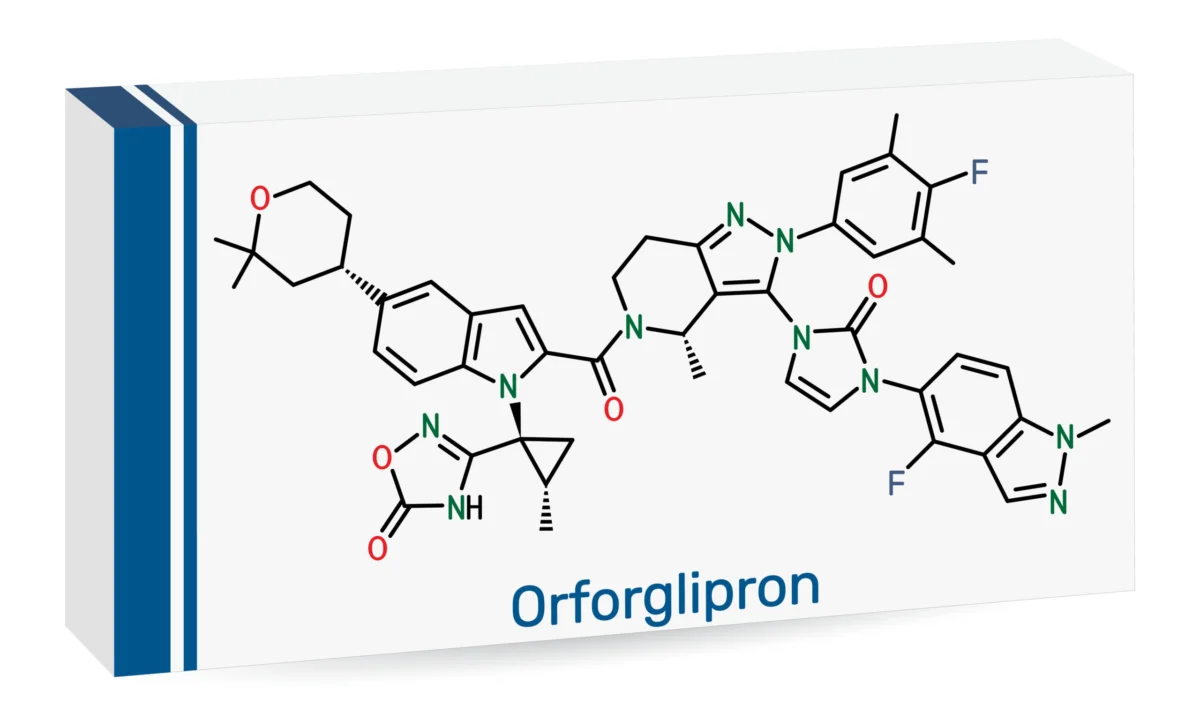

Lilly’s Strategic Play with Oral Orforglipron

Eli Lilly’s strategic foresight in the obesity market is further exemplified by the recent FDA approval of its oral GLP-1 receptor agonist, orforglipron, marketed as Foundayo. Licensed from Chugai in 2018, Foundayo represents a significant advancement by offering a once-daily oral small-molecule GLP-1, a potential game-changer in terms of patient convenience and accessibility. The approval, announced on April 1, 2026, with commercial availability commencing April 9, 2026, positions Lilly to further solidify its leadership in the metabolic health space.

While Mounjaro and Zepbound remain the primary drivers of Lilly’s impressive 2025 performance and are projected to continue leading revenue gains in 2026 (Lilly guided to $80 billion to $83 billion in 2026 revenue), Foundayo introduces a new strategic variable. Its late Q1 2026 approval means its impact will be more pronounced in the latter half of the fiscal year. Analysts, however, hold differing views on its immediate revenue potential, acknowledging its strategic importance in expanding market access and appealing to patients who prefer oral medication over injectables. The convenience of a pill could significantly widen the patient funnel, attracting individuals hesitant to use injectable therapies. This move not only diversifies Lilly’s GLP-1 portfolio but also positions it to compete more effectively against future oral GLP-1 entrants from other pharmaceutical companies.

According to Citeline’s 2026 Pharma R&D Annual Review, the anti-obesity pipeline experienced a "gut-busting" 30.7% expansion, reaching 588 active compounds, even as the overall pharmaceutical pipeline contracted. This data underscores the intense competition and innovation pouring into this therapeutic area. Orforglipron’s entry into this rapidly expanding market, while strategically crucial, will still navigate the established success of its injectable predecessors, Mounjaro and Zepbound, which are already operating at blockbuster scale.

Novo Nordisk’s Expanding Semaglutide Franchise

Novo Nordisk, a pioneer in diabetes and obesity care, continues to evolve its semaglutide franchise to meet market demands. While the older oral semaglutide product, Rybelsus, saw a 2% decline at constant exchange rates (CER) in 2025, the company’s focus is clearly on the newer, higher-dose oral Wegovy. The launch of oral Wegovy in January 2026 and its anticipated broader rollout in 2026, alongside the introduction of new doses like the 7.2 mg and the recently launched Wegovy HD in the U.S., reflect Novo Nordisk’s commitment to expanding access and options within the semaglutide family.

Despite these strategic launches, Novo Nordisk’s own 2026 guide for adjusted sales growth came in at a cautious negative 5% to negative 13% at CER. This outlook reflects anticipated pricing pressure, increasing competition (particularly from Lilly’s strong portfolio), and evolving U.S. market access dynamics. While oral semaglutide is strategically vital for patient convenience and market penetration, it does not currently appear poised to be the primary driver of absolute revenue growth for Novo Nordisk in 2026, suggesting that the established injectable forms will continue to contribute the lion’s share of sales. The challenge for Novo Nordisk, as for all players in this space, will be to balance market expansion with sustainable pricing and effective differentiation in an increasingly crowded field.

Diversification Beyond GLP-1s: The Strength of Immunology and Oncology

While the GLP-1 agonists have seized the spotlight, the pharmaceutical leaderboard beneath Keytruda is far from a monoculture. The FY2025 data reinforces the enduring strength and growth potential of several large, durable franchises in immunology and oncology. These therapeutic areas continue to be pillars of pharmaceutical revenue, driven by unmet medical needs and continuous innovation.

AbbVie, for example, demonstrated the power of its immunology engine. Skyrizi (risankizumab), primarily for psoriasis and psoriatic arthritis, reached $17.562 billion in 2025 sales, while Rinvoq (upadacitinib), an oral JAK inhibitor for various inflammatory conditions, achieved $8.304 billion. Together, these two drugs generated a combined $25.866 billion in 2025, accounting for approximately 42% of AbbVie’s total net revenue of $61.160 billion for the year. This impressive performance underscores AbbVie’s successful pivot and diversification strategy in the post-Humira era, proving that it can generate blockbuster-level sales from multiple assets in immunology. The company’s 2026 adjusted EPS guidance of $14.37 to $14.57 further signals confidence in the continued growth of these key products.

Other significant gainers in 2025 included Sanofi’s Dupixent (dupilumab), an antibody for atopic dermatitis, asthma, and other allergic conditions, which rose to €15.714 billion. Novartis’ Kisqali (ribociclib), a CDK4/6 inhibitor for breast cancer, climbed a remarkable 58% to $4.783 billion, showcasing strong uptake in oncology. Johnson & Johnson also reported that its 2025 Innovative Medicine growth was primarily fueled by established products such as Darzalex (daratumumab) for multiple myeloma and Tremfya (guselkumab) for psoriatic disease.

These figures align with broader industry trends. Citeline’s 2026 R&D review highlighted that immunologicals were one of the few large therapeutic categories that continued to expand, growing by 20.6% even as the overall pipeline count experienced a dip. This indicates sustained investment and innovation in treating autoimmune and inflammatory diseases, driven by new mechanisms of action and expanding patient populations. The consistent growth of these specialty brands illustrates that the pharmaceutical market remains diverse and robust, with significant opportunities beyond the highly publicized GLP-1 phenomenon.

Strategic Implications and Future Outlook

The FY2025 Pharma 50 report offers several critical insights into the strategic direction of the pharmaceutical industry. First, the dual leadership of Keytruda at the brand level and tirzepatide/semaglutide at the molecule level signifies a transitional period. While oncology remains a high-value therapeutic area, the metabolic health market, particularly obesity, has demonstrated an unprecedented capacity for rapid expansion and revenue generation. Companies with strong positions in this segment are poised for substantial growth.

Second, the impending loss of exclusivity for Keytruda serves as a stark reminder of the constant need for pipeline renewal and diversification in the pharmaceutical sector. Merck’s proactive measures, while commendable, underscore the immense challenge of replacing a multi-billion-dollar revenue stream. This pressure will likely accelerate M&A activity and R&D investment in novel therapies across various disease areas.

Third, the success of oral GLP-1s like orforglipron and oral Wegovy highlights the importance of patient convenience and accessibility in market adoption. While injectable therapies have proven highly effective, oral formulations can significantly broaden market reach, particularly for chronic conditions requiring long-term treatment. The competition in the obesity market is set to intensify, with a wave of new compounds and modalities expected to emerge, pushing companies to innovate not only in efficacy but also in delivery and patient experience.

Finally, the continued robust performance of immunology and other oncology franchises demonstrates the resilience and diversification of the pharmaceutical market. These therapeutic areas, driven by ongoing scientific advancements and significant unmet needs, will continue to be critical revenue drivers. The pharmaceutical industry is entering a dynamic era characterized by intense competition, rapid innovation, and a strategic reorientation towards areas of immense public health demand. The leaderboard of 2025 is not just a snapshot of past performance but a blueprint for the battles and breakthroughs that will define the industry’s future.

Leave a Reply