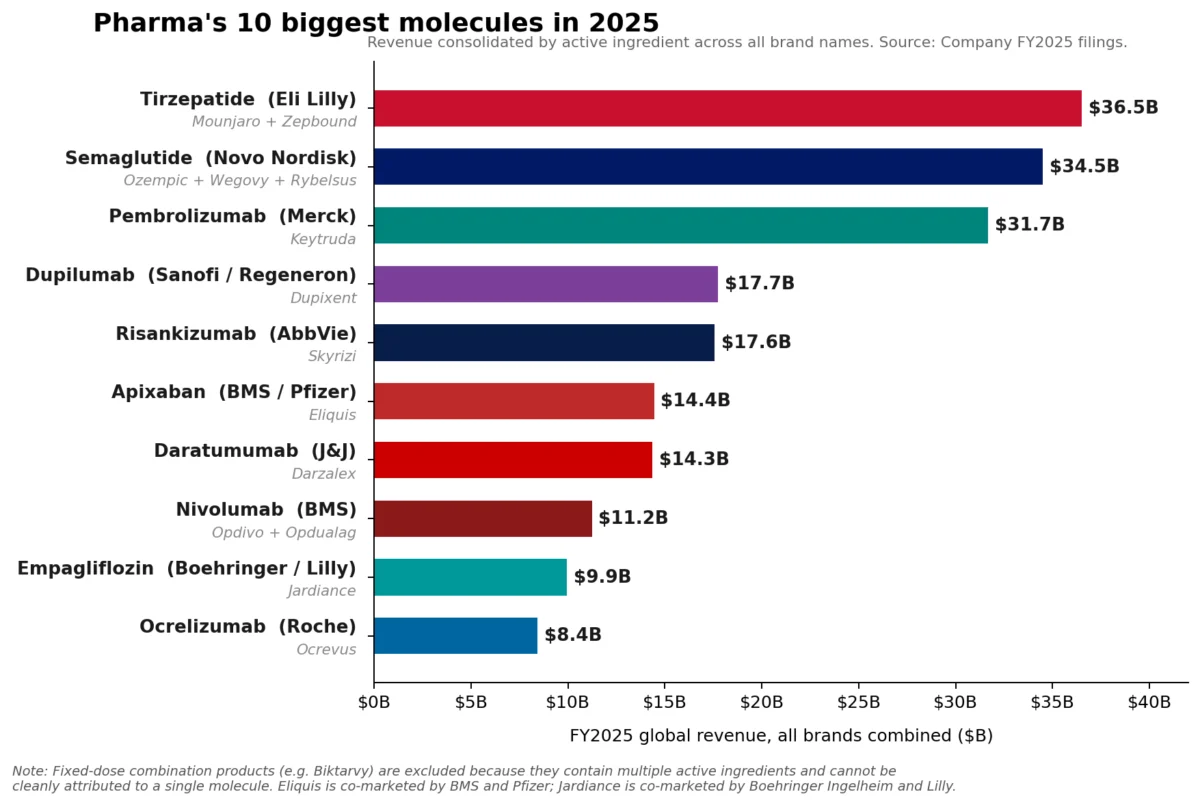

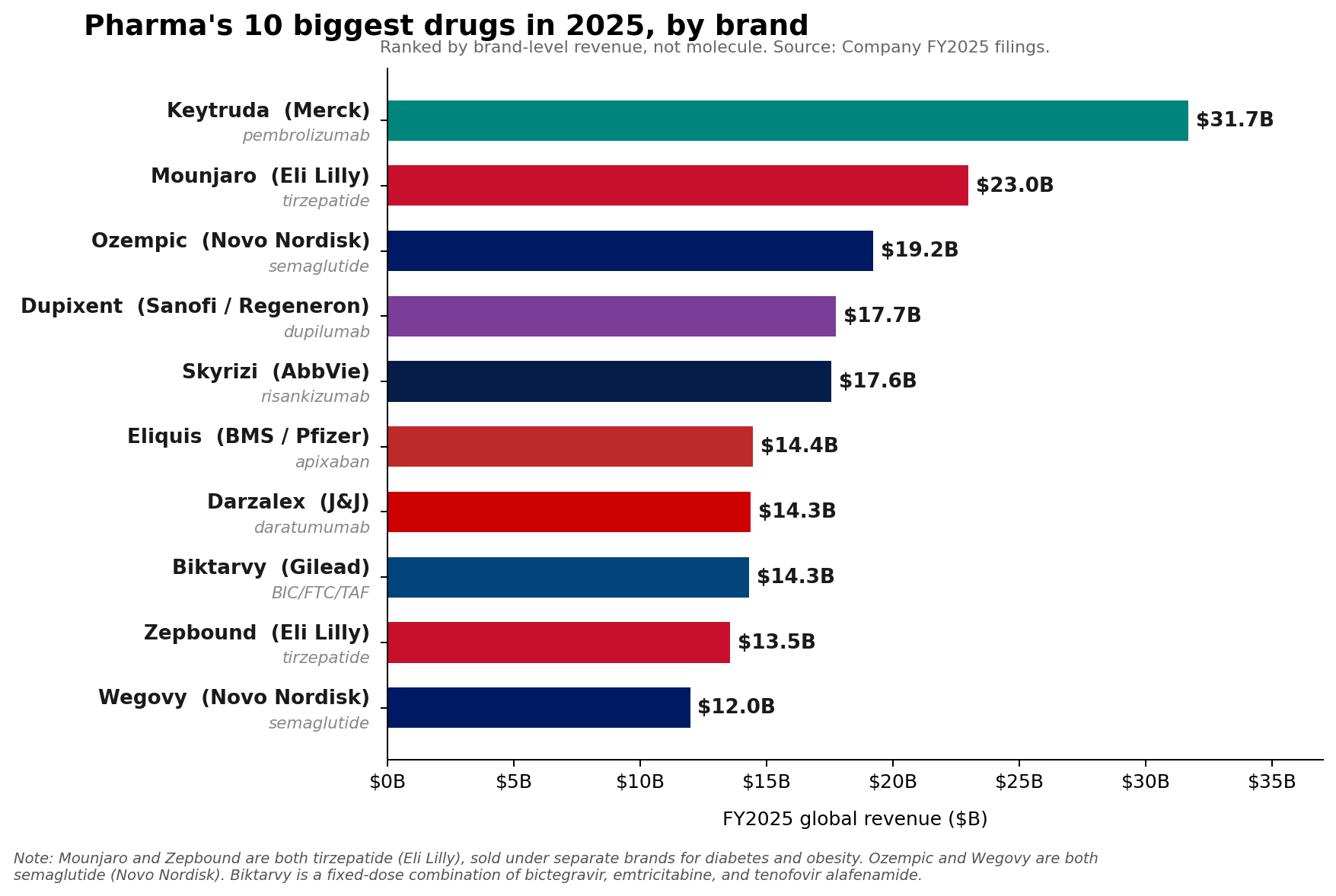

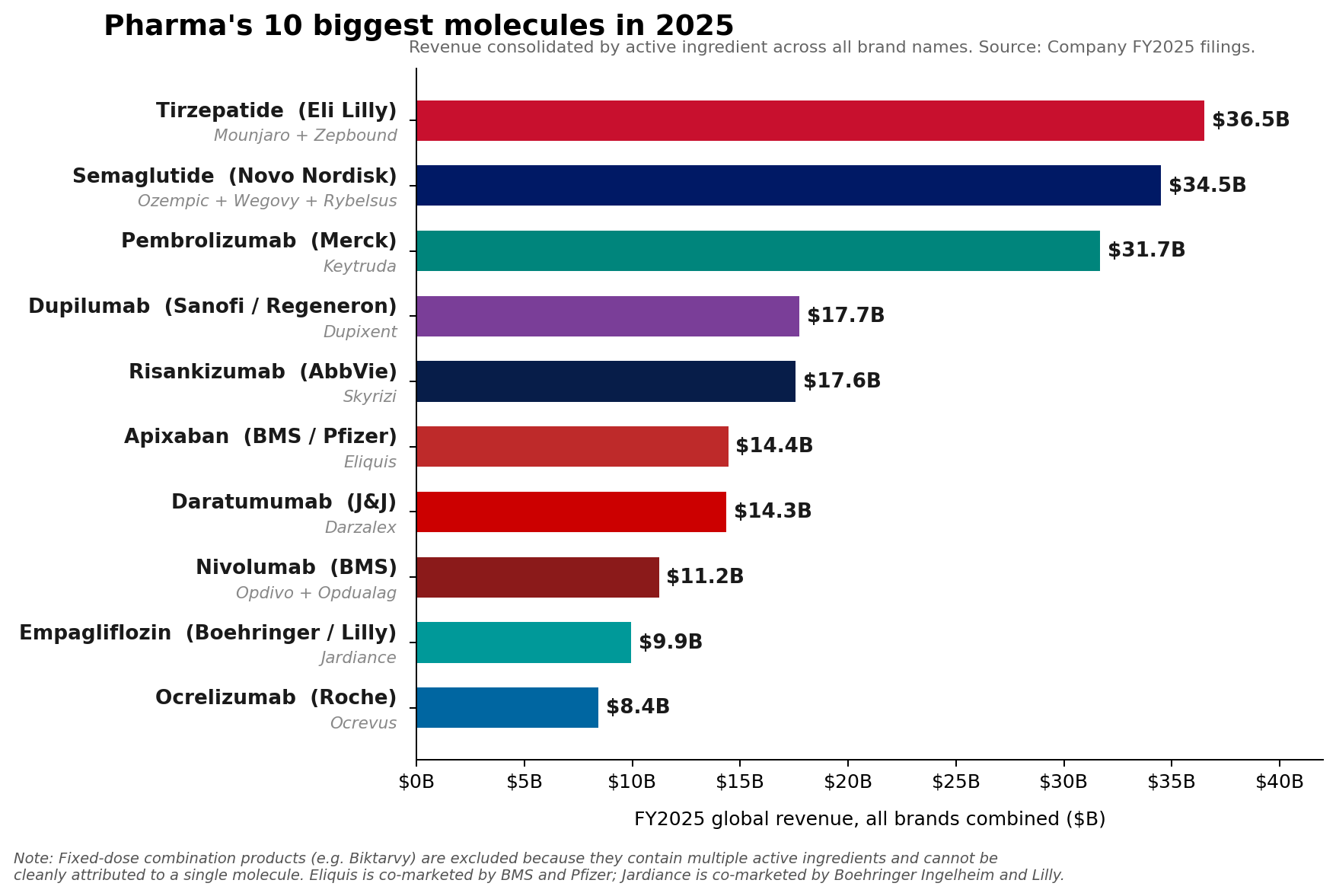

Merck’s Keytruda (pembrolizumab) maintained its formidable position as the pharmaceutical industry’s leading brand in Fiscal Year 2025, recording an impressive $31.7 billion in sales. However, a significant shift has occurred at the molecular level, signaling an evolving landscape in the global pharmaceutical market. For the first time, two revolutionary metabolic drug franchises—Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide—have collectively surpassed Keytruda’s molecule-level sales, challenging the long-standing dominance of oncology treatments at the pinnacle of drug revenue.

The ascendance of these GLP-1 and GIP receptor agonists marks a pivotal moment, driven by their profound impact on managing type 2 diabetes and, increasingly, obesity. Lilly’s tirzepatide franchise, comprising the blockbuster drugs Mounjaro and Zepbound, achieved a combined revenue of approximately $36.5 billion in 2025. Mounjaro alone contributed $22.965 billion, with Zepbound rapidly adding $13.542 billion. Hot on its heels, Novo Nordisk’s semaglutide franchise, encompassing Ozempic, Wegovy, and Rybelsus, collectively garnered roughly $34.5 billion, underscoring the explosive growth and transformative potential of this therapeutic class.

Keytruda’s Enduring Brand Strength Amidst Shifting Tides

Despite being overtaken at the molecule level, Keytruda’s performance in FY2025 remains a testament to its unparalleled success and Merck’s strategic execution. The immuno-oncology powerhouse grew by a robust 7% in 2025, demonstrating sustained market penetration and clinical utility across a widening array of cancer indications. Keytruda, a programmed cell death protein 1 (PD-1) inhibitor, has revolutionized cancer treatment since its initial approval in 2014, becoming a cornerstone therapy for melanoma, non-small cell lung cancer, head and neck squamous cell carcinoma, and numerous other malignancies. Its mechanism of action, which involves blocking the PD-1 pathway to unleash the immune system’s anti-tumor response, has made it a foundational drug in modern oncology.

Merck continues to actively extend the Keytruda franchise through lifecycle management strategies, including the pursuit of new indications and the development of more convenient formulations such as subcutaneous Keytruda QLEX. These efforts are crucial as the drug approaches its critical loss of exclusivity (LOE) in the coming years. Patent expiry typically opens the door to biosimilar competition, which can significantly erode market share and revenue. However, Merck CEO Rob Davis has publicly characterized the anticipated revenue drop-off as "more of a hill than a cliff," a statement reflecting confidence in the drug’s entrenched position, continued expansion into new treatment algorithms, and the potential for the subcutaneous formulation to offer a differentiated patient experience that could buffer some of the impact of biosimilar entry.

Nonetheless, the looming LOE has cast a shadow on Merck’s immediate financial outlook. The company’s FY2026 revenue guidance, projected between $65.5 billion and $67.0 billion, fell below Wall Street expectations, signaling investor apprehension regarding the future revenue trajectory post-patent cliff. This scenario underscores the immense pressure on pharmaceutical giants to innovate and diversify their pipelines to mitigate the inevitable impact of patent expirations on their top-selling assets.

The Metabolic Revolution: Tirzepatide and Semaglutide Reshape the Landscape

The rise of tirzepatide and semaglutide is not merely a statistical anomaly but a profound indicator of a paradigm shift in pharmaceutical priorities and market demand. These drugs address two of the most prevalent and costly public health crises globally: type 2 diabetes and obesity.

Eli Lilly’s tirzepatide, marketed as Mounjaro for type 2 diabetes and Zepbound for chronic weight management, distinguishes itself as a dual glucose-dependent insulinotropic polypeptide (GIP) and glucagon-like peptide-1 (GLP-1) receptor agonist. This dual mechanism offers superior efficacy in glycemic control and weight loss compared to GLP-1 monotherapy, contributing to its rapid adoption and exceptional revenue growth. The combined sales figures for Mounjaro and Zepbound highlight the immense unmet need in both the diabetes and obesity markets, which are characterized by large patient populations and historically limited effective long-term treatment options.

Similarly, Novo Nordisk’s semaglutide franchise, comprising Ozempic (diabetes), Wegovy (obesity), and Rybelsus (oral diabetes), leverages the power of GLP-1 agonism. While Ozempic and Wegovy are injectable formulations, Rybelsus represents an earlier foray into oral GLP-1 therapy. The success of semaglutide, particularly Wegovy, has catapulted obesity into a primary therapeutic focus for the pharmaceutical industry, demonstrating that significant investment in this area can yield unprecedented commercial success. The global obesity epidemic, affecting hundreds of millions, provides a vast and growing market for highly effective weight management solutions.

The rapid ascent of these metabolic drugs has captivated not only patients and prescribers but also investors, who recognize the vast market potential and the transformative impact these therapies can have on public health outcomes. The collective sales of tirzepatide and semaglutide underscore a broader trend: the industry’s focus is diversifying beyond oncology, with metabolic disorders emerging as equally lucrative and impactful therapeutic arenas.

The Oral Wildcard: Orforglipron and the Future of Convenience

The competitive landscape in the obesity market is poised for further intensification, particularly with the introduction of novel oral formulations. Eli Lilly’s orforglipron, licensed from Chugai in 2018 and now marketed as Foundayo, represents a significant strategic play. This once-daily oral small-molecule GLP-1 receptor agonist received FDA approval on April 1, 2026, and became commercially available as of April 9, 2026.

Orforglipron is considered a potential "wildcard" by industry analysts, who hold differing views on its ultimate market impact. While the convenience of an oral pill could significantly expand patient access and adherence compared to injectables, its late market entry relative to Lilly’s own Mounjaro and Zepbound, which are already blockbuster-scale injectables, means its immediate revenue contribution in 2026 may be strategic rather than dominant. Lilly’s 2026 revenue guidance of $80 billion to $83 billion is primarily predicated on the continued robust performance of Mounjaro and Zepbound. Foundayo’s approval post-Q1 2026 suggests its impact will be felt more strongly in the latter half of the year and beyond.

The broader significance of orforglipron lies in its potential to democratize access to highly effective weight loss therapies. An oral formulation could reduce barriers related to injection aversion, storage, and administration, potentially reaching a wider segment of the eligible population. This strategic move highlights the ongoing race among pharmaceutical companies to deliver more convenient and patient-friendly drug delivery systems, especially in chronic conditions requiring long-term treatment.

Similarly, Novo Nordisk is pushing the envelope with oral semaglutide. While the older Rybelsus formulation saw a 2% decline at constant exchange rates (CER) in 2025, the newer oral Wegovy pill, launched in January 2026, is central to Novo Nordisk’s future obesity strategy. The company plans a broader rollout of oral Wegovy in 2026, including the introduction of a 7.2 mg dose in various countries and the recent launch of Wegovy HD in the U.S. However, Novo Nordisk’s overall 2026 guidance anticipates adjusted sales growth of negative 5% to negative 13% at CER, reflecting anticipated pricing pressures, heightened competition, and complex U.S. access dynamics. This suggests that while oral semaglutide is strategically important for market expansion and patient choice, it may not immediately translate into dominant revenue growth in 2026 compared to its established injectable counterparts.

Beyond GLP-1s: Sustained Growth in Immunology and Oncology

While the GLP-1/GIP agonists have captured headlines, other specialty brands in immunology and oncology continued to demonstrate impressive growth and market strength in 2025, preventing the pharmaceutical leaderboard from becoming a "GLP-1 monoculture." These large, durable franchises are still compounding, driven by expanding indications, strong clinical profiles, and unmet patient needs.

AbbVie’s immunology portfolio, a testament to strategic pipeline development post-Humira, showed exceptional performance. Skyrizi (risankizumab) achieved $17.562 billion in sales in 2025, and Rinvoq (upadacitinib) reached $8.304 billion. Together, these two drugs generated $25.866 billion, accounting for approximately 42% of AbbVie’s total net revenue of $61.160 billion for the year. This establishes AbbVie’s immunology engine as a formidable force, with two drugs approaching the scale of the industry’s largest single brands. Skyrizi and Rinvoq, used in conditions like psoriasis, psoriatic arthritis, and rheumatoid arthritis, exemplify the continued demand for advanced immunomodulatory therapies.

Sanofi’s Dupixent (dupilumab), another immunology standout, rose to an impressive €15.714 billion ($17.06 billion USD at an approximate 1.08 USD/EUR exchange rate), solidifying its position as a leading treatment for atopic dermatitis, asthma, and other inflammatory conditions. Novartis’s Kisqali (ribociclib), an oncology drug for breast cancer, climbed a remarkable 58% to $4.783 billion, showcasing the continued innovation and market demand within targeted cancer therapies. Johnson & Johnson also reported strong 2025 Innovative Medicine growth, primarily fueled by products such as Darzalex (daratumumab) for multiple myeloma and Tremfya (guselkumab) for psoriasis and psoriatic arthritis.

Broader Industry Trends and the R&D Landscape

The commercial picture presented by the top-selling drugs is reinforced by broader trends in pharmaceutical research and development. Citeline’s 2026 R&D review highlighted a significant expansion in specific therapeutic areas even as the overall pipeline count dipped. Immunologicals, for instance, were one of the few large therapeutic buckets that continued to expand, rising by 20.6%. This indicates sustained investment and ongoing innovation in autoimmune and inflammatory diseases, driven by the identification of novel targets and a growing understanding of disease pathology.

Perhaps most striking, the anti-obesity pipeline experienced a "gut-busting" 30.7% jump, expanding to 588 active compounds. This dramatic increase underscores the industry’s vigorous response to the soaring demand for effective weight management solutions and the groundbreaking success of the GLP-1/GIP class. The concentration of R&D efforts in these high-growth areas suggests a strategic reallocation of resources, with companies prioritizing therapeutic categories that promise substantial returns and address critical unmet medical needs. This focused investment contrasts with a general contraction observed in other therapeutic areas, signaling a more selective and concentrated approach to drug discovery and development across the industry.

Outlook: A Dynamic Pharmaceutical Future

The FY2025 sales figures paint a picture of a pharmaceutical industry in dynamic transition. While established giants like Keytruda continue to demonstrate formidable brand strength, the molecular leadership has undeniably shifted towards metabolic innovators. The rapid ascent of tirzepatide and semaglutide underscores the immense commercial potential of addressing widespread conditions like diabetes and obesity, challenging oncology’s long-held dominance at the revenue summit.

The impending loss of exclusivity for Keytruda, coupled with the strategic launch of oral GLP-1s, signals a period of intense competition and innovation. Companies like Merck are investing heavily in lifecycle management and pipeline diversification, while Lilly and Novo Nordisk are racing to capture and expand the burgeoning obesity market with new formulations and delivery methods. Meanwhile, robust growth in immunology and other oncology franchises demonstrates the enduring strength and diversity of the pharmaceutical landscape.

The future of the Pharma 50 will likely be characterized by a more diversified top tier, driven by a blend of next-generation metabolic drugs, resilient immunological therapies, and targeted oncology innovations. This evolving landscape promises continued advancements for patients and a fascinating competitive arena for pharmaceutical companies and investors alike.

Leave a Reply