Eli Lilly and Company, currently riding an unprecedented wave of success fueled by its GLP-1 franchise, has announced its intent to acquire Kelonia Therapeutics in a deal potentially valued at up to $7 billion. This strategic move, focusing on an early-stage CAR-T developer, signals Lilly’s determined effort to diversify its pipeline and secure future growth beyond its highly lucrative diabetes and obesity portfolio. The acquisition comes amidst a broader M&A spree by Lilly, prompting industry observers to draw parallels with Pfizer’s recent post-COVID spending binge, and to question whether Lilly can navigate its expansion without encountering similar financial headwinds.

Lilly’s Strategic Foray into Advanced Oncology: The Kelonia Acquisition

On [Insert Date if available, otherwise imply recent], Eli Lilly formally announced its agreement to acquire Kelonia Therapeutics, a biotechnology company specializing in in vivo CAR-T cell therapies, for an upfront payment plus significant milestone-based considerations that could total up to $7 billion. This acquisition marks a significant expansion of Lilly’s oncology footprint, particularly into the cutting-edge field of gene-edited cell therapies. Kelonia’s technology focuses on developing CAR-T therapies that can be administered directly into a patient’s body, eliminating the need for complex and time-consuming ex vivo cell manufacturing processes currently associated with approved CAR-T treatments. This in vivo approach holds the promise of making these transformative therapies more accessible, less expensive, and potentially safer for a broader patient population battling various forms of cancer.

The strategic rationale behind the Kelonia acquisition is multifaceted. Firstly, it positions Lilly at the forefront of the next generation of CAR-T development, an area with immense therapeutic potential but also significant technological hurdles. The ability to deliver CAR-T cells in vivo could revolutionize cancer treatment, offering a novel modality for patients who may not be eligible for or cannot access conventional CAR-T therapies. Secondly, it strengthens Lilly’s oncology pipeline, which, while robust, has not yet achieved the blockbuster status seen in its metabolic disease division. Investing in innovative platforms like Kelonia’s demonstrates Lilly’s long-term commitment to oncology, a therapeutic area often characterized by high unmet medical need and significant market opportunity.

A Broader M&A Blitz: Diversifying Beyond GLP-1

The Kelonia deal is not an isolated event but rather the latest in a series of strategic acquisitions and collaborations that underscore Lilly’s aggressive pursuit of pipeline diversification. Over the past couple of years, the company has committed substantial capital to bolster its R&D capabilities across various therapeutic areas and technological platforms:

- Morphic Therapeutic (2024): Lilly acquired Morphic Therapeutic for approximately $3.2 billion. This acquisition brought Morphic’s oral integrin inhibitors, including a Phase 2 asset for inflammatory bowel disease, into Lilly’s immunology and gastroenterology portfolio, signaling a commitment to expanding in these high-growth areas.

- Scorpion Therapeutics (2025): A collaboration with Scorpion Therapeutics, potentially worth up to $2.5 billion, focused on discovering and developing novel small-molecule precision oncology drugs. This partnership leverages Scorpion’s drug discovery platform to target undruggable cancer pathways.

- Verve Therapeutics (2025): A collaboration with Verve Therapeutics, valued at around $1.3 billion, entered Lilly into the burgeoning field of in vivo gene editing. This partnership aims to develop gene-editing therapies for cardiovascular diseases, a major area of unmet need.

- SiteOne Therapeutics (2025): Lilly acquired SiteOne Therapeutics for up to $1.0 billion, enhancing its pain management pipeline with SiteOne’s Phase 2-ready selective sodium channel inhibitors.

- Insilico Medicine (2026): A significant collaboration with Insilico Medicine, potentially reaching $2.75 billion, highlights Lilly’s embrace of artificial intelligence in drug discovery. This partnership aims to leverage Insilico’s end-to-end AI engine to identify and develop novel preclinical oral therapeutics, demonstrating a forward-looking strategy to accelerate drug development cycles and reduce costs.

Collectively, these deals represent a potential aggregate value of approximately $18 billion, reflecting a concerted effort by Lilly to invest in earlier-stage, platform-oriented assets across diverse therapeutic modalities, including small molecules, biologics, gene editing, cell therapy, and AI-driven discovery. This strategy aims to build a sustainable pipeline that can deliver the "next wave of growth" well beyond the current dominance of its GLP-1 franchise.

The GLP-1 Juggernaut: Fueling Lilly’s Ambitions

The financial firepower behind Lilly’s aggressive M&A strategy originates directly from the unprecedented success of its tirzepatide franchise. Tirzepatide, marketed as Mounjaro for type 2 diabetes and Zepbound for chronic weight management, has rapidly ascended to become one of the best-selling pharmaceutical products globally.

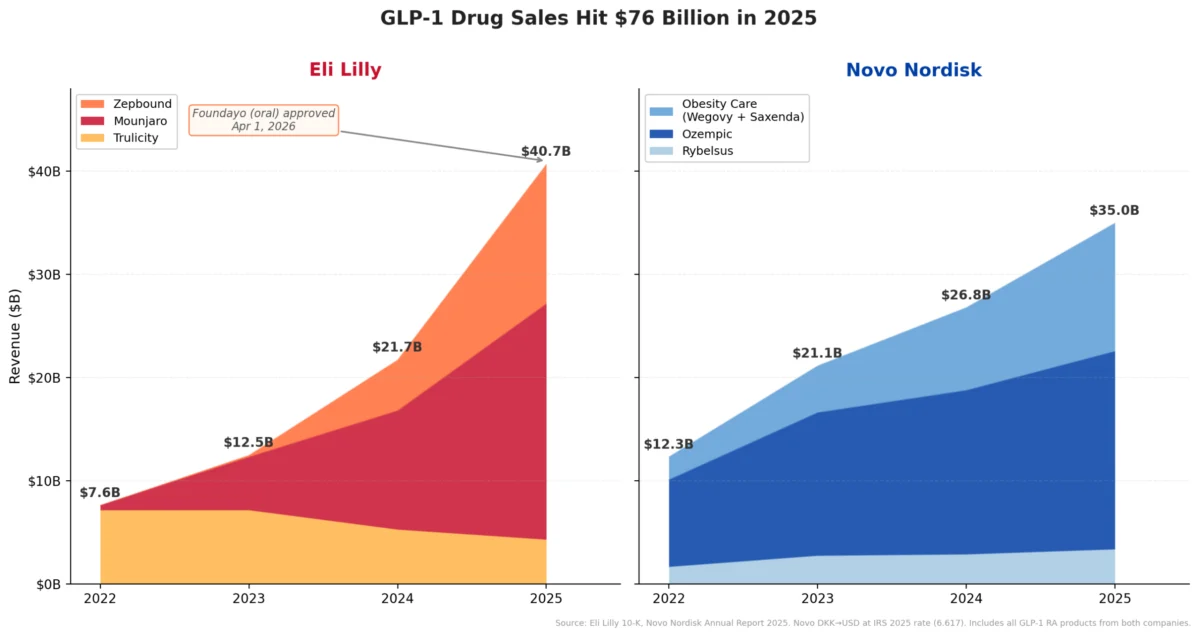

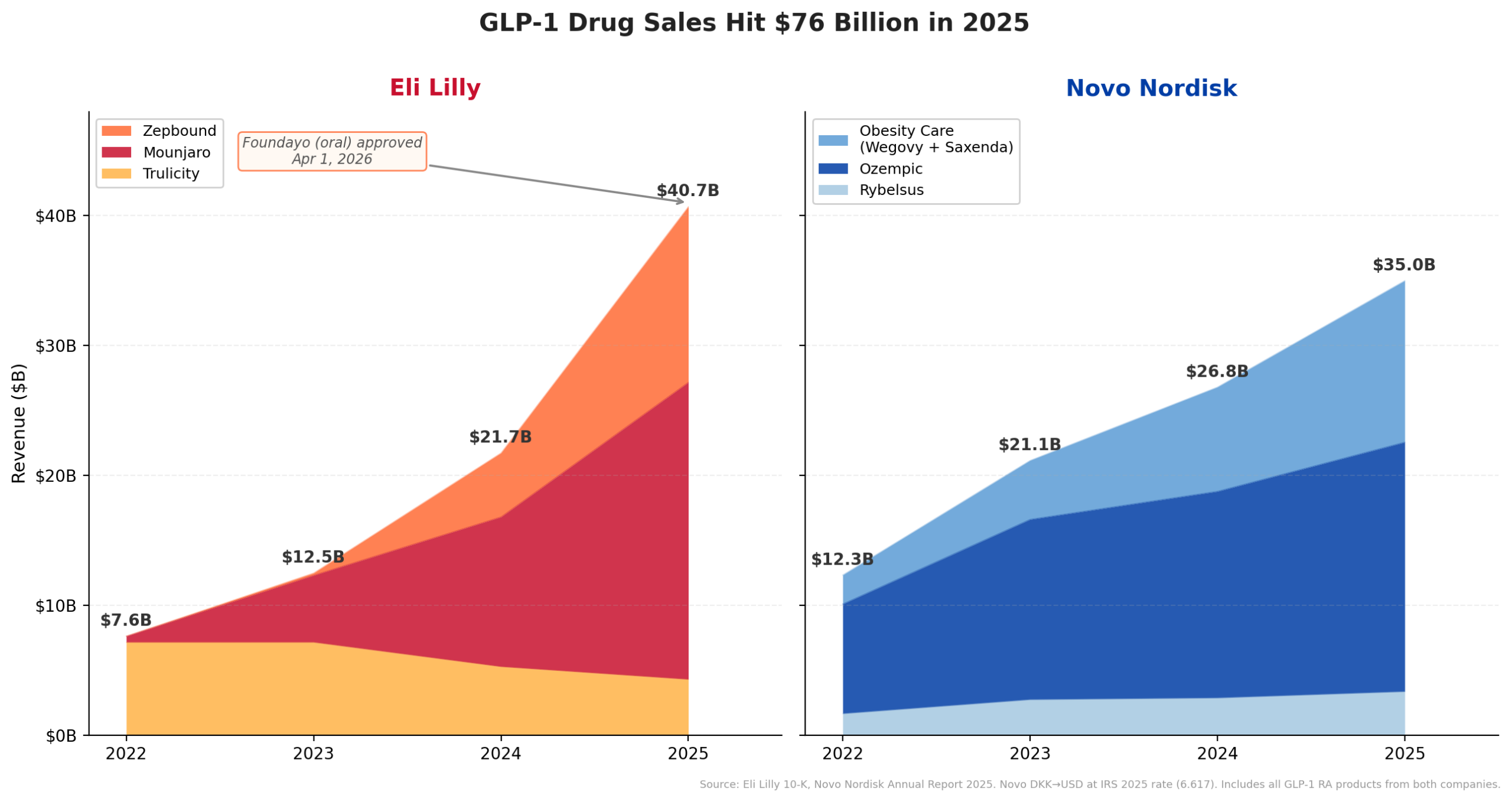

In 2025, tirzepatide generated roughly $36.5 billion of Lilly’s total $65.2 billion in revenue, with Mounjaro contributing $23.0 billion and Zepbound adding $13.5 billion. This represents a staggering growth trajectory, with Lilly’s overall GLP-1 revenue surging from $7.6 billion in 2022 to $40.7 billion in 2025 – a more than fivefold increase in just three years. Management has guided for continued robust growth, projecting total revenue for 2026 to be between $80 billion and $83 billion, underscoring the sustained momentum of its GLP-1 portfolio.

Further solidifying its market position, Lilly received FDA approval for Foundayo (orforglipron), its oral GLP-1 for obesity, on April 1, 2026, under the National Priority Voucher program, just 50 days after filing. This rapid approval and subsequent rollout through LillyDirect at $149/month for the lowest dose, with anticipated Medicare Part D access at $50/month by July, adds a crucial oral growth vector to its injectable franchise. This strategic expansion is expected to broaden patient access and market penetration, further enhancing Lilly’s revenue base.

The company’s financial posture remains strong, with $7.3 billion in cash and $16.8 billion in operational cash flow, even with long-term debt standing at $40.9 billion. This robust cash generation from its growing revenue base provides the necessary capital for its acquisition spree, allowing it to invest heavily in future innovation.

Pfizer’s Precedent: A Cautionary Tale?

The context of Lilly’s current M&A activity inevitably draws comparisons to Pfizer’s recent spending spree, particularly its acquisition of Seagen for $43 billion in late 2023. Pfizer, like Lilly, found itself flush with cash from a single blockbuster franchise, albeit one driven by a unique global health crisis.

Pfizer’s COVID-19 vaccine, Comirnaty, and antiviral treatment, Paxlovid, generated an extraordinary windfall during the pandemic. In 2022, Pfizer’s total revenue peaked at $100.3 billion, with Comirnaty contributing $37.8 billion and Paxlovid $18.9 billion. This immense cash flow enabled Pfizer to embark on a significant acquisition drive, aiming to build out its oncology business and deepen its antibody-drug conjugate (ADC) portfolio. Beyond Seagen, Pfizer also acquired Biohaven Pharmaceuticals for approximately $11.6 billion in 2022, gaining access to its approved migraine drug Nurtec ODT, and Global Blood Therapeutics for around $5.4 billion in 2022, adding the approved sickle cell disease treatment Oxbryta. These deals collectively represented approximately $60 billion in headline acquisition value.

However, the timing and nature of Pfizer’s acquisitions differed significantly from Lilly’s. Pfizer was acquiring Seagen just as its COVID windfall was already in free fall. Full-year revenue for Pfizer collapsed by 42% from $100.3 billion in 2022 to $58.5 billion in 2023, with Comirnaty sales dropping by 64% and Paxlovid by 58%. This sharp decline in its primary revenue drivers meant that Pfizer was making massive acquisitions from a position of declining, rather than growing, financial strength. The acquired assets were predominantly commercial or late-stage, aimed at immediately filling the impending revenue gap left by the plummeting COVID-19 product sales. This strategy, while securing new revenue streams, also placed significant pressure on Pfizer’s balance sheet, leading to deferred share buybacks until the company could de-lever post-Seagen.

Divergent Playbooks: Growth vs. Gap-Filling

The contrast between Lilly’s and Pfizer’s approaches highlights two distinct M&A playbooks:

- Timing of the Deal Wave: Lilly’s M&A spree is happening while its cash engine, tirzepatide, is still on a steep upward curve, projecting continued growth into 2026. This allows Lilly to invest from a position of strength, anticipating further revenue generation to support these long-term bets. Pfizer, conversely, launched its major acquisitions as its COVID-19 revenue was already in sharp decline, effectively using a past windfall to plug future revenue holes.

- Stage of Acquired Assets: Lilly is largely targeting earlier-stage assets and platform technologies – Phase 1, Phase 1/2, or preclinical assets like Kelonia, Scorpion, Verve, SiteOne, and Insilico Medicine. This indicates a strategy focused on building a diversified, innovative pipeline for the long term, with the understanding that these investments will take years to mature. Pfizer, on the other hand, focused on approved or late-stage commercial assets such as Nurtec, Oxbryta, and Seagen’s portfolio of four approved ADCs. This was a clear strategy to acquire immediate revenue and established market presence to offset the rapid decline of its COVID-19 products.

- Financial Posture and Market Perception: Lilly’s current financial health is robust, with growing revenue and strong operational cash flow, supporting its investment strategy. Its market capitalization reflects this confidence, standing between $830 billion and $880 billion in April 2026. Pfizer, while a giant in its own right, has faced significant challenges in investor confidence following its revenue cliff, reflected in its market cap of approximately $155 billion during the same period. The market seems to be rewarding Lilly’s proactive, growth-oriented strategy over Pfizer’s reactive, gap-filling approach.

- Risk Profile: Lilly’s investments in early-stage technologies carry higher clinical and regulatory risks but also offer potentially higher rewards if successful, as they could represent truly transformative medicines. Pfizer’s focus on late-stage and commercial assets carries lower developmental risk but higher integration risk and often comes at a premium valuation, with less upside potential from foundational scientific breakthroughs.

Broader Implications for the Biopharma Landscape

Lilly’s aggressive M&A strategy, particularly its move into in vivo CAR-T with Kelonia and its embrace of AI in drug discovery, reflects several key trends shaping the broader biopharmaceutical industry:

- Diversification Imperative: Major pharmaceutical companies are increasingly aware of the need to diversify their revenue streams and therapeutic portfolios to mitigate risks associated with patent cliffs and market competition. Relying heavily on one or two blockbuster drugs, while lucrative in the short term, can leave companies vulnerable.

- Pursuit of Transformative Technologies: The biopharma industry is witnessing a rapid evolution in therapeutic modalities, from traditional small molecules and biologics to gene therapies, cell therapies, and gene editing. Companies like Lilly are investing heavily to acquire expertise and platforms in these cutting-edge areas, which promise to deliver truly transformative treatments for previously intractable diseases.

- The Rise of AI in Drug Discovery: The collaboration with Insilico Medicine underscores the growing importance of artificial intelligence and machine learning in accelerating drug discovery and development. AI can analyze vast datasets, identify novel drug targets, and design more effective compounds, potentially reducing the time and cost associated with bringing new medicines to market.

- Competitive Landscape in Metabolic Diseases: While Lilly is leveraging its GLP-1 success, the market for obesity and diabetes treatments is becoming increasingly competitive, with rivals like Novo Nordisk also aggressively expanding their portfolios. Lilly’s continued investment in an oral GLP-1 (Foundayo) and diversification into other areas can be seen as a strategy to maintain its competitive edge and long-term growth even as the GLP-1 market matures. Notably, Lilly’s GLP-1 revenue growth has been steeper than Novo Nordisk’s over the 2022-2025 period, and Lilly is guiding for continued growth in 2026, while Novo projects a slight decline in adjusted sales. This suggests Lilly may indeed have a more durable playbook, at least in the near term.

Conclusion: A Calculated Bet on Future Innovation

Eli Lilly’s acquisition of Kelonia Therapeutics and its broader M&A strategy represent a calculated bet on future innovation, financed by the unparalleled success of its GLP-1 franchise. By focusing on early-stage, platform-oriented assets across diverse and cutting-edge therapeutic areas, Lilly aims to build a sustainable pipeline that can drive growth for decades to come.

The contrast with Pfizer’s recent acquisition spree serves as a crucial point of analysis. While both companies leveraged significant windfalls, Lilly’s timing – investing from a position of growing strength – and its focus on foundational technologies differentiate its approach. Pfizer’s strategy, while understandable given its revenue cliff, appears to have been more about immediate revenue replacement and late-stage asset consolidation.

Whether Lilly can successfully integrate these diverse, early-stage assets and translate them into commercial success remains to be seen. The risks associated with early-stage drug development are considerable. However, by strategically deploying its substantial GLP-1 generated capital into high-potential, transformative technologies, Lilly appears to be laying the groundwork for sustained long-term growth, rather than merely seeking to fill immediate revenue gaps. The market, as evidenced by its robust valuation, seems to be optimistic that Lilly’s proactive and diversified approach will indeed help it avoid the post-blockbuster challenges that have impacted its peer. The coming years will reveal if Lilly’s "durable playbook" can successfully translate into a new era of pharmaceutical leadership.

Leave a Reply