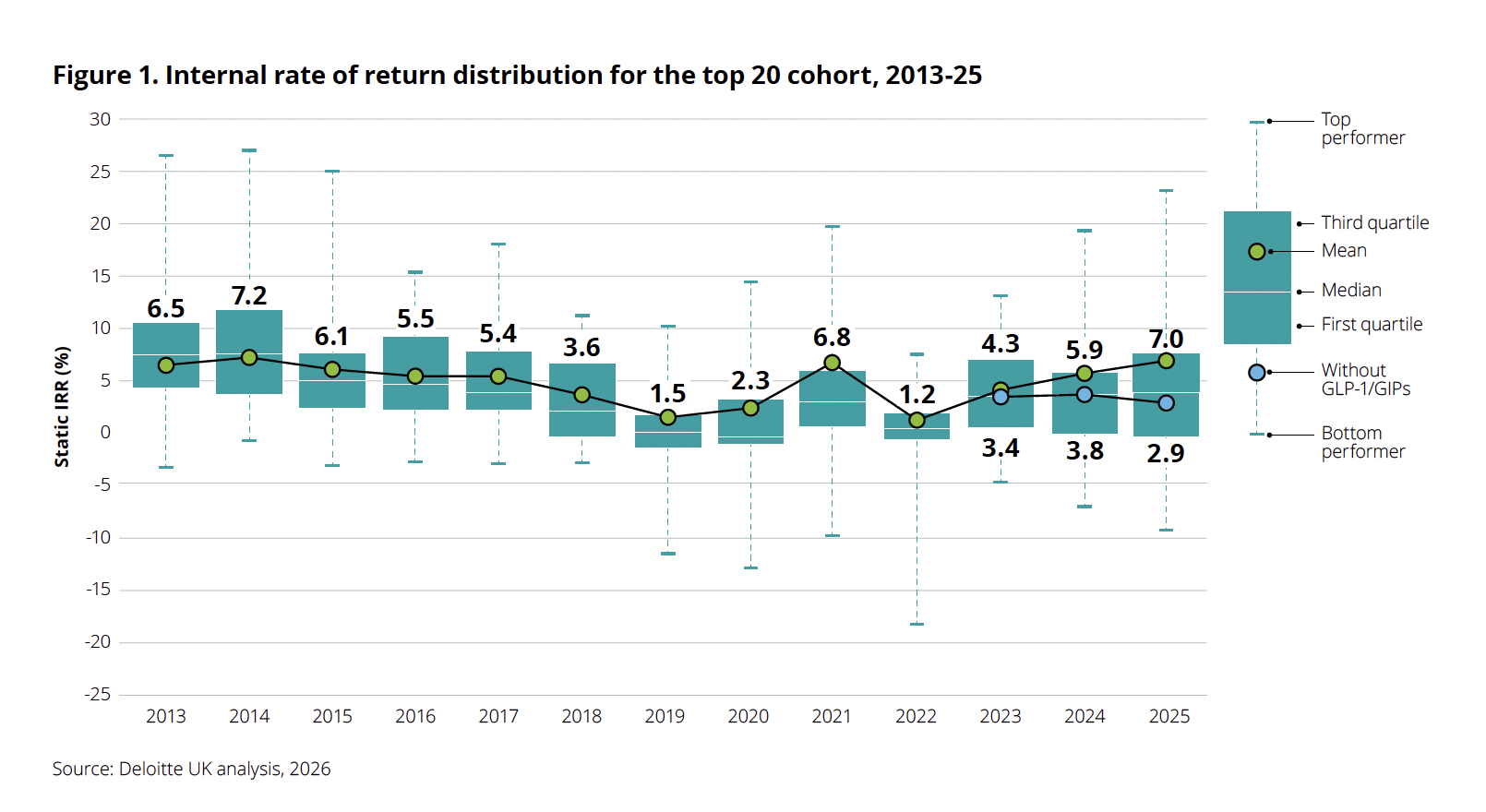

After a prolonged period where growth remained uneven in the wake of global disruptions, a pivotal metric for biopharma research and development (R&D) productivity has demonstrated a notable upward trajectory. The 16th annual "Measuring the Return from Pharmaceutical Innovation" report by Deloitte, aptly titled "Navigating the GLP-1 boom," indicates that the projected internal rate of return (IRR) on late-stage pipeline assets has ascended for the third consecutive year, reaching 7.0% in 2025. This marks a substantial increase from 5.9% recorded in the preceding year, signaling what some industry observers describe as a transition from a challenging "winter" to a more promising "spring" for the sector. Kevin Dondarski, a principal for life sciences strategy at Deloitte Consulting, underscored the significance of this shift, stating, "We went through a period of so many years where the returns kept declining, excluding the COVID impact in the middle. But the increase over the last few years is analytically unprecedented."

However, this impressive headline figure is accompanied by a crucial caveat. A significant portion of this growth in 2025 can be attributed to a singular class of therapeutics: Glucagon-like peptide-1 (GLP-1) and Glucose-dependent insulinotropic polypeptide (GIP) receptor agonists, primarily targeting obesity and related metabolic conditions. These highly impactful drugs are estimated to account for a staggering 38% of all projected commercial inflows from the 2025 late-stage pipeline. Were these therapies to be excluded from the analysis, the overall IRR would plummet from 7.0% to a mere 2.9%. For context, the IRR stood at 5.9% in 2024, and without the contribution of GLP-1/GIP drugs, it was 3.8%. This stark disparity highlights a dual narrative within the pharmaceutical landscape. "There are two different messages here," Dondarski explained. "One, it’s certainly attractive, because the market is valuing the potential impact that those therapies can have on the public, which is great. But at the same time, it raises the question of sustainability. As those programs progress, is there going to continue to be that opportunity through the next generation and the next? It will create a responsibility for these companies to find the right assets to replace in the pipeline." This year’s report marks the most dramatic instance in its 16-year history where the removal of a single drug class so profoundly altered the headline IRR.

The Rise of GLP-1s: A Paradigm Shift in Pipeline Value

The emergence of GLP-1/GIP receptor agonists, initially developed for type 2 diabetes, has dramatically reshaped the pharmaceutical industry’s focus and valuation metrics. These drugs, which work by mimicking natural hormones to regulate blood sugar, slow gastric emptying, and promote satiety, have shown remarkable efficacy in weight loss. This has opened up a colossal market opportunity in obesity, a chronic disease affecting hundreds of millions globally and associated with numerous comorbidities such as cardiovascular disease, sleep apnea, and certain cancers. The sheer scale of this unmet medical need and the clinical effectiveness of these therapies have led to unprecedented market excitement and investor confidence.

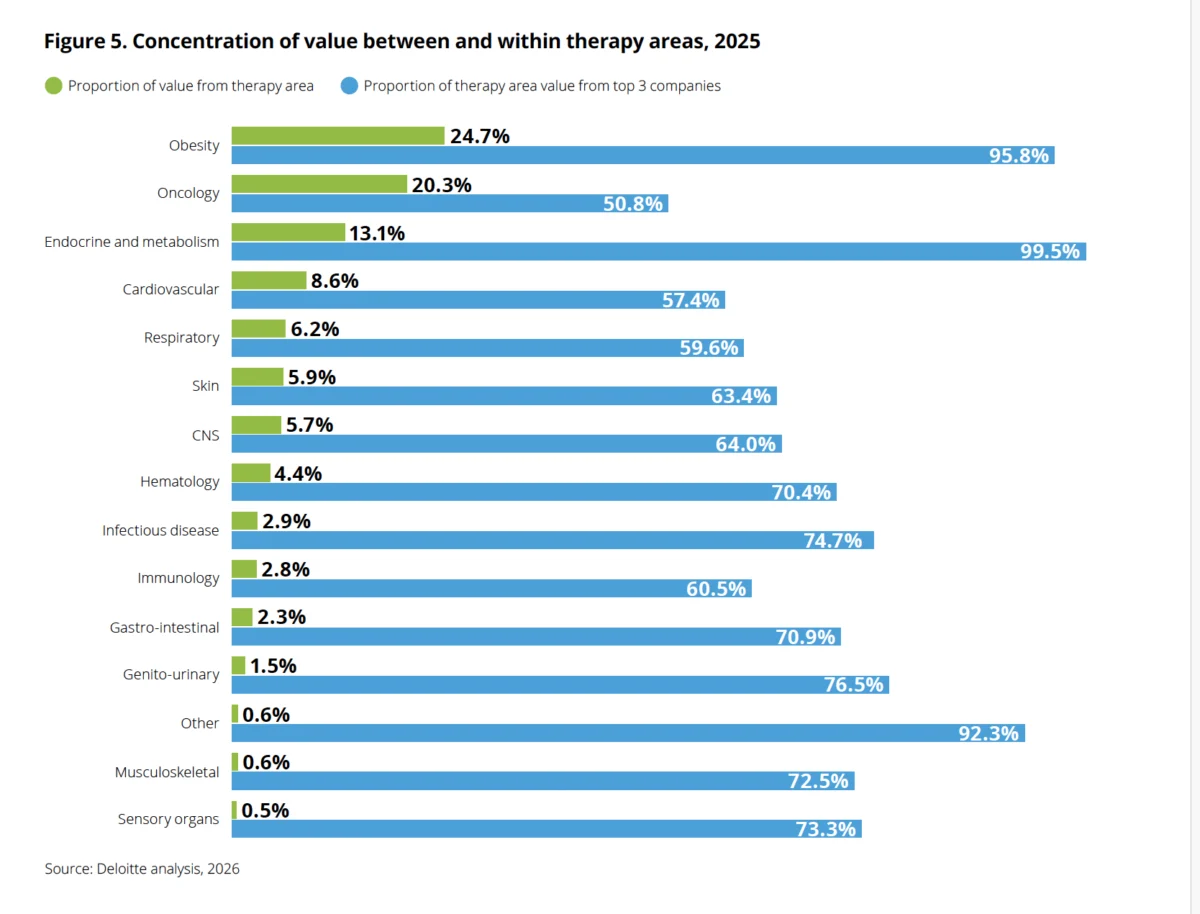

For the first time in the report’s 16-year history, obesity now commands the largest share of late-stage pipeline value, reaching 24.7%. This surpasses oncology, which traditionally held the top spot, now accounting for 20.3%. However, the concentration within the obesity segment is even more striking: nearly 96% of that value is attributed to just three companies, underscoring the dominant positions of a few key players. This concentration raises questions about market diversification and the potential for future competitive dynamics as more companies attempt to enter this lucrative space.

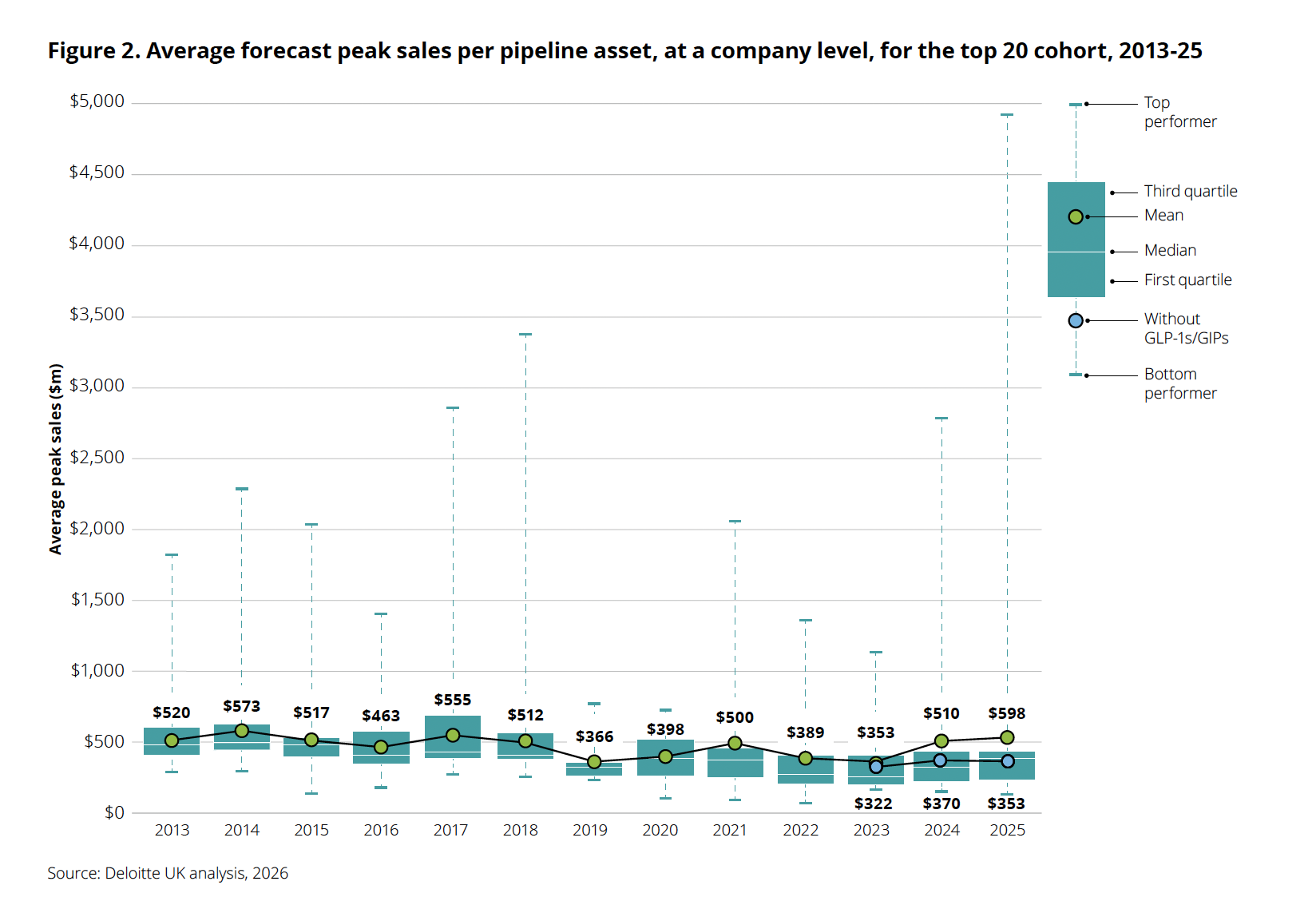

The average forecast peak sales per pipeline asset has also seen a significant jump, rising to $598 million in 2025. Yet, this aggregate figure masks the underlying reality. The top-performing assets, predominantly GLP-1/GIP drugs, now approach an astounding $5 billion in projected peak sales. In stark contrast, if these obesity blockbusters are excluded, the average forecast peak sales per asset drops to $353 million, which is actually lower than the figure from the year prior. This data point is critical, as it suggests that underlying pipeline productivity, when stripped of the GLP-1 effect, is actually declining, presenting a significant challenge for the industry’s long-term health and innovation model.

Navigating the "GLP-1 Boom": A Look at Industry Leaders

The "GLP-1 boom" has brought both immense opportunity and significant turbulence to the pharmaceutical giants at its forefront, primarily Eli Lilly and Novo Nordisk. Investors have been receiving mixed signals regarding the long-term durability and growth trajectory of this new therapeutic class.

Eli Lilly, the developer of tirzepatide (marketed as Mounjaro for diabetes and Zepbound for obesity), has experienced a dynamic period. While the company reported a robust first quarter in 2026, surpassing analyst expectations, its stock has seen a modest skid of approximately 10-13% year-to-date. Despite this volatility, Lilly raised its full-year revenue guidance to an impressive $82-$85 billion, primarily on the strength of Mounjaro and Zepbound’s volume growth. In Q1 2026, Lilly reported revenue of $19.8 billion (against an expected $17.6 billion), representing a substantial 56% year-over-year increase. This growth was largely driven by Mounjaro, which garnered $8.7 billion (+125%), and Zepbound, which brought in $4.1 billion (+79%). Further solidifying its position, Lilly launched its oral GLP-1, orforglipron (marketed as Foundayo), in April 2026, signaling its continued commitment to expanding its portfolio in the metabolic disease space. However, even Lilly’s stellar performance came with a nuance: its 56% revenue growth was fueled by a 65% volume increase, partially offset by a 13% decline in realized prices, hinting at early signs of pricing pressures or strategic adjustments.

Novo Nordisk, another dominant player with its semaglutide-based drugs Ozempic (diabetes) and Wegovy (obesity), has faced more pronounced challenges. In 2025, the company underwent significant leadership changes, with longtime CEO Lars Fruergaard Jorgensen being replaced by Maziar Mike Doustdar, amid slowing momentum and pressure on its share price. A broader restructuring followed, with seven board members stepping down at an extraordinary general meeting in November 2025, and the company announcing plans to cut approximately 9,000 roles from its global workforce of 78,400. By Q1 2026, Novo Nordisk’s workforce had reportedly shrunk to about 67,900 employees, implying a reduction of around 10,500 roles since the restructuring announcement.

Adding to investor disappointment, Novo Nordisk’s highly anticipated CagriSema, a combination of the amylin analogue cagrilintide and semaglutide, failed to meet expectations. In February 2026, results from the REDEFINE 4 Phase 3 head-to-head trial showed that CagriSema delivered 23.0% weight loss, falling short of non-inferiority against Lilly’s Zepbound, which achieved 25.5% weight loss. This outcome triggered another wave of investor concern regarding Novo Nordisk’s future growth drivers beyond its existing GLP-1 portfolio. Despite these headwinds, Novo Nordisk’s Q1 2026 results reported sales of DKK 96.8 billion ($15.2 billion). Its oral Wegovy pill, launched on January 5, 2026, performed exceptionally well, generating DKK 2.26 billion in its inaugural quarter, nearly double the DKK 1.16 billion analysts had anticipated. However, like Lilly, Novo Nordisk’s adjusted sales still fell 4% at constant exchange rates once a one-time $4.2 billion 340B provision reversal was excluded, further highlighting the complexities of market dynamics and pricing.

The Spiraling Cost of R&D and Unfulfilled AI Promise

Beyond the dazzling performance of GLP-1s, the Deloitte report sheds light on a more concerning trend: the relentless increase in the cost of pharmaceutical R&D. The average cost to develop a drug from discovery to launch continued its upward climb, reaching an astonishing $2.67 billion in 2025, a significant leap from $2.23 billion in the previous year. Dondarski confirmed that this was not an anomaly caused by a single outlier, noting, "We saw the cost increase for 17 out of the 20 companies, so it was a persistent theme."

Several factors converged to drive this spike. R&D costs continued to rise above general inflation, indicating systemic inefficiencies or increasing complexity in drug development. Large-scale merger and acquisition (M&A) deals also played a role, often inflating the R&D cost base of acquiring companies. Furthermore, attrition rates remained high, with the overall number of late-stage programs shrinking by approximately 4-5%, meaning more resources are being expended on fewer successful candidates. This trend of escalating costs, coupled with the declining underlying pipeline productivity when GLP-1s are excluded, paints a challenging picture for sustainable innovation across the industry.

In last year’s edition of the Deloitte report, titled "Be brave, be bold," the firm strongly urged pharmaceutical companies to embrace AI-powered drug development platforms, automation, and advanced analytics as a crucial pathway to reversing decades of declining R&D productivity. The expectation was that artificial intelligence could significantly reduce development time and costs, streamlining processes from target identification to clinical trial optimization. However, the 2025 data suggests that this promise has "not yet been realized at scale." Clinical cycle times remain stubbornly long, and R&D costs continue their ascent, indicating that AI’s transformative potential is still largely untapped in practical application.

The report attributes this gap to a "pilot-driven, function-by-function approach" rather than a holistic, integrated strategy. While pharmaceutical companies are actively exploring AI, the widespread, systemic integration needed to unlock its full value remains elusive. "Everybody’s actively focusing on AI, and everybody’s had some degree of success," Dondarski noted, acknowledging the industry’s engagement. "But from our vantage point, there’s a good amount of variability in the velocity at which organizations are scaling those efforts to maximize value creation." This suggests that while individual successes exist, the industry as a whole is struggling with the strategic implementation and scaling of AI technologies across the entire drug development lifecycle. The implication is that without a more cohesive and aggressive approach to AI adoption, the challenges of rising costs and stagnant productivity in non-GLP-1 areas will persist.

Broader Implications and Future Outlook

The Deloitte report’s findings carry significant implications for the pharmaceutical industry’s strategic direction, investment landscape, and long-term innovation model. The heavy reliance on a single class of drugs, however groundbreaking, raises questions about portfolio diversification and resilience. Companies are now faced with the "responsibility" to identify and nurture the next generation of assets that can sustain growth beyond the current GLP-1 boom. This necessitates intensified investment in early-stage research, exploring novel mechanisms of action, and venturing into therapeutic areas that may not offer immediate blockbuster potential but could yield significant patient benefits and market share in the longer term.

The pricing pressures observed with GLP-1s, including agreements to lower U.S. prices through Medicare, Medicaid, and the TrumpRx initiative (which lists oral Wegovy at $149/month, Wegovy pen at $199, Ozempic at $199, and Zepbound at $299), indicate that even highly successful drugs are not immune to scrutiny and market adjustments. This further underscores the need for a diversified pipeline, as relying on a few high-value assets makes companies vulnerable to policy changes, competitive entrants, and evolving payer landscapes.

For investors, the report presents a nuanced picture. While the headline IRR is encouraging, the underlying trends suggest that investment decisions need to look beyond the immediate success of GLP-1s and carefully assess the breadth and depth of a company’s entire pipeline. Companies that demonstrate a robust strategy for sustainable innovation, effective cost management in R&D, and successful integration of advanced technologies like AI across their operations may be better positioned for long-term value creation.

Ultimately, the 16th edition of Deloitte’s report serves as a critical barometer for the pharmaceutical industry. It celebrates the remarkable success and patient impact of GLP-1/GIP therapies, which have injected much-needed vitality into R&D returns. However, it simultaneously issues a stark warning: beneath the surface of this GLP-1-driven resurgence, fundamental challenges in R&D productivity persist, costs continue to escalate, and the transformative potential of AI remains largely unfulfilled. The future health of pharmaceutical innovation will depend on the industry’s ability to leverage the current boom to strategically reinvest, diversify, and fundamentally reshape its approach to drug discovery and development.