Eli Lilly and Company is embarking on a significant acquisition spree, exemplified by its recent agreement to acquire Kelonia Therapeutics for up to $7 billion, signaling a strategic push into next-generation cell therapies. This proactive expansion, funded by the surging revenues from its tirzepatide franchise, invites comparisons to Pfizer’s substantial M&A activities following its COVID-19 windfall. While both pharmaceutical giants leveraged blockbuster drug success to fuel major deals, the timing, nature of acquired assets, and underlying financial trajectories present a stark contrast, raising critical questions about Lilly’s ability to navigate its diversification strategy more smoothly than Pfizer.

Eli Lilly’s Strategic Offensive: Diversifying Beyond GLP-1 Dominance

Eli Lilly’s decision to acquire Kelonia Therapeutics for a potential $7 billion underscores a deliberate strategy to broaden its therapeutic pipeline beyond its highly successful GLP-1 receptor agonist drugs, Mounjaro and Zepbound. The deal, announced in early 2026, aims to integrate Kelonia’s innovative in vivo CAR-T (Chimeric Antigen Receptor T-cell) technology, which promises to overcome some of the significant logistical and cost challenges associated with conventional ex vivo CAR-T therapies. Traditional CAR-T treatments involve extracting a patient’s T-cells, genetically modifying them outside the body, and then reinfusing them—a complex, time-consuming, and expensive process. Kelonia’s approach, still in early clinical development (Ph 1), seeks to deliver the CAR-T genes directly into T-cells within the patient’s body, potentially making the therapy more accessible, safer, and less costly.

This acquisition is not an isolated event but rather the latest in a series of strategic investments by Lilly, collectively totaling around $18 billion in announced potential value over the past two years. These deals include:

- Morphic Therapeutic (2024): Approximately $3.2 billion to bolster its immunology and gastrointestinal portfolio with oral integrin inhibitors (Ph 2 assets).

- Scorpion Therapeutics (2025): Up to $2.5 billion for a portfolio of AI-driven oncology assets (Ph 1/2).

- Verve Therapeutics (2025): Around $1.3 billion for in vivo gene editing programs, particularly for cardiovascular diseases (Ph 1b).

- SiteOne Therapeutics (2025): Up to $1.0 billion for novel pain management therapies (Ph 2-ready).

- Insilico Medicine (2026): A collaboration potentially worth up to $2.75 billion for a suite of AI-originated preclinical oral therapeutics, further embedding artificial intelligence into its drug discovery process.

These acquisitions and collaborations reflect a clear pattern: Lilly is targeting earlier-stage pipeline assets and platform technologies, particularly in cutting-edge areas like cell and gene therapy, AI-driven drug discovery, and immunology. This approach suggests a long-term vision to cultivate future growth drivers while its GLP-1 franchise continues to generate substantial revenue.

The GLP-1 Powerhouse: Fueling Lilly’s Ambitions

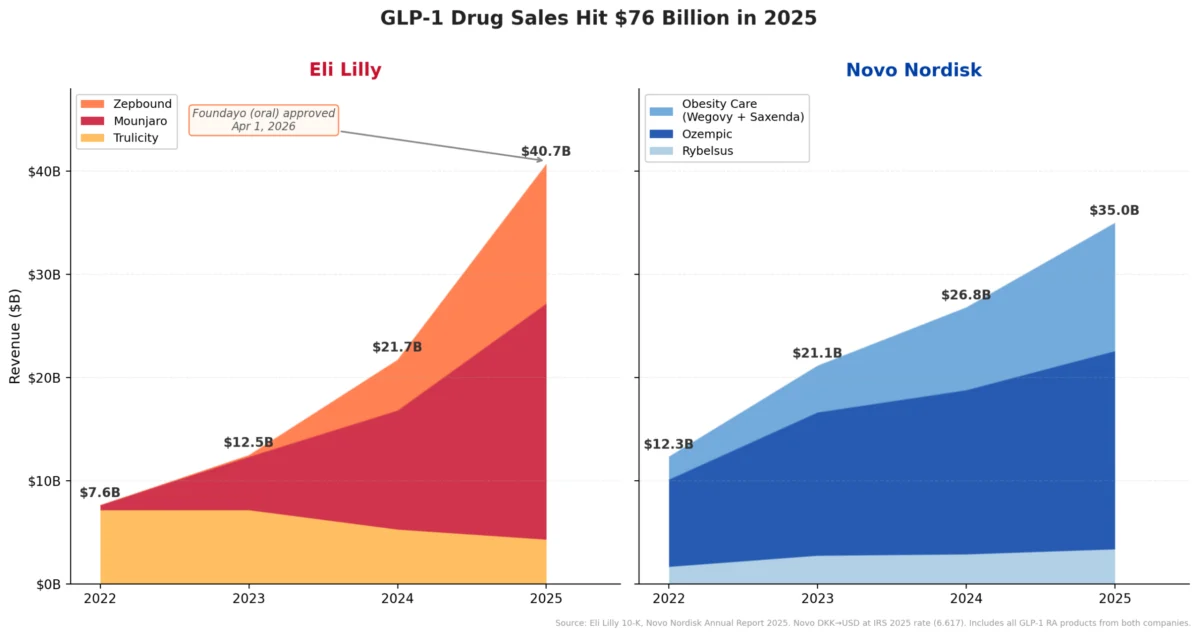

The financial bedrock supporting Lilly’s ambitious M&A strategy is the explosive growth of its tirzepatide franchise. Tirzepatide, marketed as Mounjaro for type 2 diabetes and Zepbound for chronic weight management, has redefined the landscape of metabolic disease treatment. In 2025, tirzepatide alone generated approximately $36.5 billion of Lilly’s $65.2 billion in total revenue, with Mounjaro contributing $23.0 billion and Zepbound $13.5 billion. This represents a remarkable increase from $7.6 billion in GLP-1 revenue in 2022 to $40.7 billion in 2025, demonstrating a steeper growth trajectory than its competitor Novo Nordisk’s semaglutide portfolio, which climbed from $12.3 billion to $35.0 billion over the same period.

Lilly’s management has guided for continued robust growth, projecting total revenue between $80 billion and $83 billion for 2026. This confidence is further bolstered by the recent FDA approval of Foundayo (orforglipron), Lilly’s oral GLP-1 for obesity, on April 1, 2026. Approved under the National Priority Voucher program just 50 days after filing, Foundayo’s rapid market entry, with pricing at $149/month for the lowest dose via LillyDirect and anticipated Medicare Part D access at $50/month by July, adds another significant growth vector. This oral option not only expands market access but also diversifies the company’s GLP-1 offerings, potentially insulating it against future competition in the injectable space. The Q1 2026 results, due April 30, are eagerly awaited by investors to confirm this sustained momentum.

Pfizer’s Post-Pandemic Pivot: A Challenging Transition

In contrast to Lilly’s proactive diversification during a period of escalating revenue, Pfizer’s recent acquisition spree was largely a reactive measure, designed to replenish its pipeline and revenue streams after the dramatic decline of its COVID-19 related products. The pandemic years saw Pfizer achieve unprecedented financial success, with its COVID-19 vaccine Comirnaty and antiviral treatment Paxlovid driving its full-year revenue to a record $100.3 billion in 2022. Comirnaty alone contributed $37.8 billion and Paxlovid $18.9 billion that year.

However, this windfall proved to be fleeting. As global vaccination rates plateaued and demand for COVID-19 treatments waned, Pfizer’s revenue experienced a sharp contraction. Full-year revenue plummeted by 42% from its 2022 peak to $58.5 billion in 2023. Comirnaty sales crashed by 64%, and Paxlovid sales fell by 58% in the same period. This precipitous decline created an urgent need for Pfizer to acquire new revenue-generating assets and robust pipeline candidates to offset the "patent cliff" looming for several of its established drugs and the sudden void left by its pandemic products.

The Seagen Bet and Other Key Acquisitions

Pfizer’s most significant move in this period was the $43 billion acquisition of Seagen, announced in March 2023 and completed by late 2023. This deal was emblematic of Pfizer’s strategy to bolster its oncology business and deepen its antibody-drug conjugate (ADC) portfolio. Seagen brought with it four approved oncology medicines (Adcetris, Padcev, Tukysa, and Tivdak) and a promising ADC pipeline, offering Pfizer immediate commercial oncology scale and a leading position in a rapidly evolving area of cancer therapy. This acquisition was framed as a long-term investment to reposition Pfizer as a major player in oncology, a field less susceptible to the boom-and-bust cycles seen with infectious disease products.

Prior to Seagen, Pfizer also made other notable acquisitions to address its impending revenue gaps:

- Biohaven Pharmaceuticals (2022): Approximately $11.6 billion to acquire the remaining stake in Biohaven, gaining full rights to Nurtec ODT, an approved migraine drug, and a pipeline of CGRP inhibitors.

- Global Blood Therapeutics (GBT) (2022): Around $5.4 billion for GBT, adding Oxbryta, an approved treatment for sickle cell disease, and other sickle cell programs.

These acquisitions collectively represented an investment of approximately $60 billion across headline deals, primarily focused on commercial or late-stage assets. Pfizer sought to acquire products already generating revenue or on the cusp of market approval, aiming for a quicker impact on its top line compared to Lilly’s more platform-centric, earlier-stage approach.

A Tale of Two Strategies: Growth vs. Rebuilding

The comparison between Eli Lilly’s current deal spree and Pfizer’s recent M&A activities highlights fundamentally different strategic playbooks, driven by distinct financial postures and market contexts.

Timing and Financial Posture

Lilly’s M&A wave is occurring while its tirzepatide franchise is still in a steep growth phase. The company’s revenue base is expanding rapidly, with rising margins providing ample cash flow for strategic investments. As of FY2025, Lilly reported $7.3 billion in cash, $16.8 billion in operating cash flow, and $40.9 billion in long-term debt. This strong financial position allows Lilly to invest in early-stage, high-potential assets that may not yield returns for several years but offer significant long-term growth opportunities. The market cap for Lilly in April 2026 stood robustly between $830 billion and $880 billion, reflecting investor confidence in its growth trajectory and diversified pipeline.

Conversely, Pfizer’s major acquisitions, particularly Seagen, happened just as its COVID-19 windfall was in free fall. The company was facing a significant revenue cliff, and its dealmaking was perceived by many as an urgent attempt to fill a looming financial void. While Pfizer had a substantial cash reserve from its pandemic sales, the rapid decline in core product revenue put pressure on its balance sheet. Its operating cash flow was $11.7 billion in FY2025, but the substantial Seagen acquisition required significant financing. As a result, Pfizer deferred share buybacks to prioritize de-leveraging its balance sheet. This reactive strategy, coupled with the sharp revenue decline, contributed to a more cautious investor sentiment, reflected in Pfizer’s market cap of approximately $155 billion in April 2026.

Nature of Acquired Assets

Lilly’s acquisitions lean towards earlier-stage assets and platform technologies. Kelonia’s in vivo CAR-T is Ph 1, Verve’s gene editing is Ph 1b, Scorpion’s oncology assets are Ph 1/2, and Morphic’s programs are Ph 2. The Insilico Medicine collaboration is for preclinical AI-originated therapies. This focus on foundational technologies and earlier-stage clinical programs suggests a long-term investment in future innovation and the development of entirely new therapeutic modalities. This approach, while carrying higher R&D risk, offers the potential for transformative breakthroughs and sustained intellectual property.

Pfizer, on the other hand, largely acquired commercial or late-stage assets. Biohaven’s Nurtec and GBT’s Oxbryta were already approved, providing immediate revenue. Seagen’s portfolio included four approved oncology medicines and a late-stage ADC pipeline. This strategy aimed for more immediate impact on revenue and pipeline strength, seeking to quickly replace lost sales and address near-term patent expirations. While this approach carries lower development risk, it often comes with higher acquisition costs and potentially less long-term disruptive innovation.

Broader Impact and Implications

The distinct strategies of Lilly and Pfizer offer valuable insights into pharmaceutical M&A in a rapidly evolving industry.

Lilly’s Outlook: Sustained Growth and Innovation

Eli Lilly’s strategy appears to be a calculated move to capitalize on its current GLP-1 success to secure future growth vectors. By investing in areas like in vivo CAR-T, gene editing, and AI drug discovery, Lilly is positioning itself at the forefront of medical innovation. The Kelonia acquisition, in particular, could be a game-changer for cell therapy, potentially democratizing access to these powerful treatments by making them simpler and less expensive to administer. This proactive diversification, coupled with the continued strength of its GLP-1 franchise and the launch of oral Foundayo, suggests a more durable growth playbook. However, the risks associated with early-stage assets are significant; many preclinical and Phase 1 programs fail. Lilly will need to demonstrate strong R&D execution to translate these promising technologies into approved therapies. The competitive landscape in GLP-1s is also intensifying, with numerous players developing next-generation obesity and diabetes treatments, requiring Lilly to maintain its innovation edge.

Pfizer’s Path Forward: Integration and R&D Productivity

Pfizer’s challenge lies in effectively integrating its numerous acquisitions, particularly the complex Seagen deal, and translating them into sustainable revenue growth. The company’s focus on oncology and ADCs is a sound strategic direction, given the high unmet medical need and market potential. However, the immediate financial impact of these acquisitions was overshadowed by the rapid decline in COVID-19 product sales, leading to investor skepticism and a significant drop in market valuation. Pfizer needs to demonstrate consistent R&D productivity from its new assets and successfully navigate clinical trials to regain investor confidence. The long-term success of its oncology pivot will depend on its ability to compete effectively against established players and continuously innovate in a highly competitive therapeutic area.

Industry Trends: Cell Therapy, AI, and Metabolic Health

Both companies’ strategies reflect broader trends in the pharmaceutical industry. The Kelonia deal highlights the growing excitement and investment in cell and gene therapies, particularly the quest to overcome the limitations of current ex vivo approaches. The Insilico Medicine collaboration underscores the increasing integration of artificial intelligence into drug discovery, promising to accelerate development timelines and improve success rates. Meanwhile, the GLP-1 market continues its unprecedented expansion, reshaping the treatment paradigms for obesity and diabetes and influencing the investment decisions of major pharmaceutical players.

In conclusion, while both Eli Lilly and Pfizer leveraged periods of significant financial strength to pursue large-scale acquisitions, their approaches diverge significantly. Lilly is making bold, early-stage bets from a position of escalating strength, aiming to proactively build its next wave of innovation. Pfizer, conversely, acted more reactively to fill a post-pandemic revenue void, prioritizing late-stage and commercial assets. The coming years will reveal whether Lilly’s strategy of investing in nascent, high-potential technologies during a period of sustained growth will prove to be a more resilient and rewarding path than Pfizer’s urgent efforts to rebuild its revenue base. The market’s perception of these contrasting playbooks, reflected in their respective valuations, suggests that timing and the nature of strategic investments are paramount in the high-stakes world of pharmaceutical M&A.

Leave a Reply