Eli Lilly and Company is embarking on a significant acquisition drive, highlighted by its agreement to acquire Kelonia Therapeutics, a developer of in vivo CAR-T cell therapies, in a deal potentially valued at up to $7 billion. This strategic move, announced amidst a period of unprecedented success driven by its GLP-1 franchise, positions Lilly to diversify its pipeline and secure future growth beyond its current blockbuster obesity and diabetes treatments. The company’s aggressive M&A strategy draws parallels with Pfizer’s post-COVID spending spree, which saw the pharmaceutical giant acquire Seagen for $43 billion. However, analysts and investors are keenly observing whether Lilly can navigate its expansion without encountering the financial headwinds that have challenged Pfizer in the wake of declining COVID-19 product sales.

Lilly’s Aggressive Push into Advanced Therapies

Lilly’s acquisition of Kelonia is a bold statement about its ambition to establish a strong foothold in the burgeoning field of advanced cell and gene therapies, specifically in vivo CAR-T. Kelonia’s technology focuses on developing therapies that can deliver CAR-T cells directly into the body, potentially eliminating the complex, time-consuming, and expensive ex vivo manufacturing process currently required for approved CAR-T treatments. This in vivo approach holds the promise of making these life-saving therapies more accessible, safer, and cost-effective for a wider patient population, particularly in oncology. The initial $250 million upfront payment, coupled with up to $6.75 billion in potential development, regulatory, and commercial milestones, underscores the high-risk, high-reward nature of this early-stage technology. Kelonia’s lead program, an in vivo CAR-T therapy targeting B-cell malignancies, is still in its preclinical phase, indicating Lilly’s willingness to invest in groundbreaking, yet unproven, platforms.

This deal is not an isolated event but rather the latest in a series of strategic transactions by Lilly, collectively valued at approximately $18 billion in potential deal value. Over the past few years, Lilly has been systematically building out its pipeline through a combination of acquisitions and collaborations targeting diverse therapeutic areas and innovative technologies. Notable deals include:

- Morphic Therapeutic (2024): Acquired for approximately $3.2 billion, Morphic brought a pipeline of oral integrin inhibitors, deepening Lilly’s immunology and gastroenterology portfolio with assets like MORF-057, a Phase 2 asset for inflammatory bowel disease.

- Scorpion Therapeutics (2025): A collaboration potentially worth up to $2.5 billion, focusing on precision oncology medicines.

- Verve Therapeutics (2025): An investment of around $1.3 billion, aimed at developing in vivo gene editing therapies for cardiovascular diseases, with a lead asset in Phase 1b.

- SiteOne Therapeutics (2025): Acquired for up to $1.0 billion, enhancing Lilly’s pain management pipeline with SiteOne’s Phase 2-ready sodium channel blockers.

- Insilico Medicine (2026): A collaboration valued at up to $2.75 billion, leveraging Insilico’s end-to-end AI drug discovery engine to identify and develop novel preclinical oral therapeutics. This partnership highlights Lilly’s commitment to integrating advanced computational methods into its R&D process.

These acquisitions collectively illustrate Lilly’s "early-stage platform bet" strategy, focusing on novel mechanisms of action and disruptive technologies that could yield future blockbusters across multiple therapeutic areas, including oncology, immunology, cardiovascular, and metabolic diseases.

The Tirzepatide Tailwind: Fueling Lilly’s Ambitions

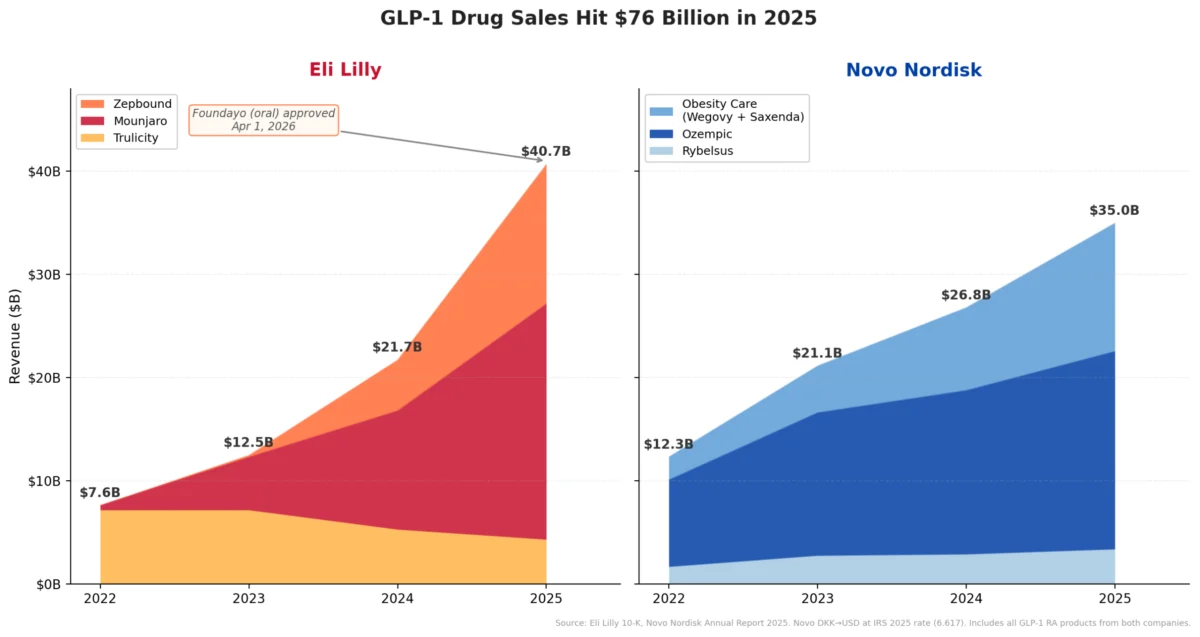

Lilly’s current acquisition spree is largely underpinned by the phenomenal success of its GLP-1 receptor agonist, tirzepatide, marketed as Mounjaro for type 2 diabetes and Zepbound for chronic weight management. The tirzepatide franchise has become a pharmaceutical juggernaut, driving unprecedented revenue growth for the company. In 2025, tirzepatide generated approximately $36.5 billion of Lilly’s $65.2 billion in total revenue, with Mounjaro contributing $23.0 billion and Zepbound $13.5 billion. This remarkable growth propelled Lilly’s total revenue by 45% year-over-year.

The company’s financial outlook remains exceptionally strong, with management guiding for $80 billion to $83 billion in revenue for 2026, signaling continued upward momentum. The strategic introduction of Foundayo (orforglipron), Lilly’s oral GLP-1 for obesity, further solidifies its market leadership. Approved by the FDA on April 1, 2026, under the National Priority Voucher program, Foundayo’s rapid approval – just 50 days after filing – underscores its potential impact. With a competitive pricing strategy of $149/month for the lowest dose via LillyDirect and anticipated Medicare Part D access at $50/month by July, Foundayo is poised to capture a significant share of the rapidly expanding oral anti-obesity market, complementing the injectable franchise. This multi-pronged approach to the GLP-1 market offers Lilly a more diversified and potentially more durable growth trajectory compared to its GLP-1 pioneer competitor, Novo Nordisk. While Lilly’s GLP-1 revenue surged from $7.6 billion to $40.7 billion between 2022 and 2025, a steeper ramp than Novo Nordisk’s $12.3 billion to $35.0 billion climb over the same period, Lilly is projecting continued growth in 2026, whereas Novo Nordisk has projected a 5% to 13% decline in adjusted sales. This divergence highlights Lilly’s strategic advantage in both pipeline depth and commercial execution within the GLP-1 space.

Pfizer’s Post-COVID Reckoning: A Cautionary Tale?

The narrative of Lilly’s current M&A push inevitably draws comparisons to Pfizer’s acquisition strategy in the wake of its COVID-19 vaccine (Comirnaty) and antiviral (Paxlovid) windfall. Pfizer’s $43 billion acquisition of Seagen in March 2023 became a symbol of its extensive post-COVID spending spree, aiming to establish a robust oncology business and deepen its antibody-drug conjugate (ADC) portfolio. Seagen brought four approved oncology medicines and a promising ADC pipeline, offering Pfizer immediate commercial assets and late-stage candidates. Other significant deals included Biohaven for $11.6 billion in 2022, securing approved migraine drug Nurtec, and Global Blood Therapeutics for $5.4 billion in 2022, adding approved sickle cell drug Oxbryta. These deals collectively amounted to approximately $60 billion across headline acquisitions.

However, Pfizer’s aggressive spending occurred just as its COVID-19 revenue was in precipitous decline. Full-year revenue for Pfizer collapsed by 42%, from $100.3 billion in 2022 to $58.5 billion in 2023. Comirnaty sales plummeted by 64%, and Paxlovid sales fell by 58%. This dramatic reduction in its cash engine left Pfizer in a challenging financial position, needing to de-lever its balance sheet and defer share buybacks post-Seagen. While the Seagen acquisition was strategically sound in terms of pipeline diversification, its timing coincided with a severe financial contraction, leading to significant investor concern and a substantial drop in Pfizer’s market capitalization, which currently hovers around $155 billion (as of April 2026), a stark contrast to Lilly’s $830 billion-$880 billion valuation.

A Tale of Two Strategies: Deep Dive Comparison

The contrasting fortunes and strategic approaches of Eli Lilly and Pfizer offer valuable insights into pharmaceutical M&A. Both companies found themselves flush with cash from a single, dominant blockbuster franchise, which served as the impetus for their respective deal-making waves. However, the timing, nature of acquired assets, and overall financial posture present distinct playbooks.

| Feature | Eli Lilly LILLY vs. PFIZER: ACQUISITION SPREE COMPARISON

Two blockbuster-funded deal waves, different playbooks

| Feature | Eli Lilly

Leave a Reply