Eli Lilly and Company, a pharmaceutical giant currently experiencing unprecedented growth driven by its blockbuster GLP-1 agonists, has announced its intention to acquire Kelonia Therapeutics, a developer of in vivo CAR-T cell therapies, in a deal potentially valued at up to $7 billion. This strategic move, confirmed in late 2026, positions Lilly to significantly expand its oncology pipeline into the cutting-edge field of gene-edited cell therapies. The acquisition is the latest in a series of aggressive M&A activities by Lilly, prompting industry observers to draw parallels with Pfizer’s substantial acquisition spree in the immediate aftermath of its COVID-19 vaccine and antiviral windfall. However, a closer examination reveals distinct strategic differences that may dictate whether Lilly can successfully navigate its expansion without encountering the same post-blockbuster challenges that have tempered Pfizer’s recent performance.

Lilly’s Ambitious Leap into Next-Generation Oncology

The acquisition of Kelonia Therapeutics underscores Lilly’s commitment to diversifying its portfolio beyond its highly successful metabolic disease franchise. Kelonia, a Boston-based biotechnology firm, is pioneering an innovative approach to CAR-T cell therapy, focusing on in vivo gene delivery. Traditional CAR-T therapies, while revolutionary for certain hematological cancers, are complex, costly, and time-consuming, requiring ex vivo manipulation of a patient’s T-cells. Kelonia’s technology, which is still in its early developmental stages (Phase 1), aims to circumvent these challenges by directly delivering CAR-encoding genetic material into T-cells within the patient’s body, potentially making the therapy more accessible, scalable, and safer.

The deal’s structure, with an upfront payment and significant milestone-based payouts reaching up to $7 billion, reflects the high-risk, high-reward nature of early-stage therapeutic platforms. For Lilly, this investment is a calculated bet on a technology that could fundamentally transform cancer treatment. The company views Kelonia’s platform as a strategic fit, leveraging its existing expertise in complex biologics and its substantial financial strength to accelerate the development of these novel therapies. This acquisition aligns with Lilly’s broader strategy of investing in innovative, potentially disruptive technologies that address significant unmet medical needs, particularly in oncology, an area where it already has a robust, albeit more conventional, presence.

The GLP-1 Phenomenon: Fueling Lilly’s Expansion

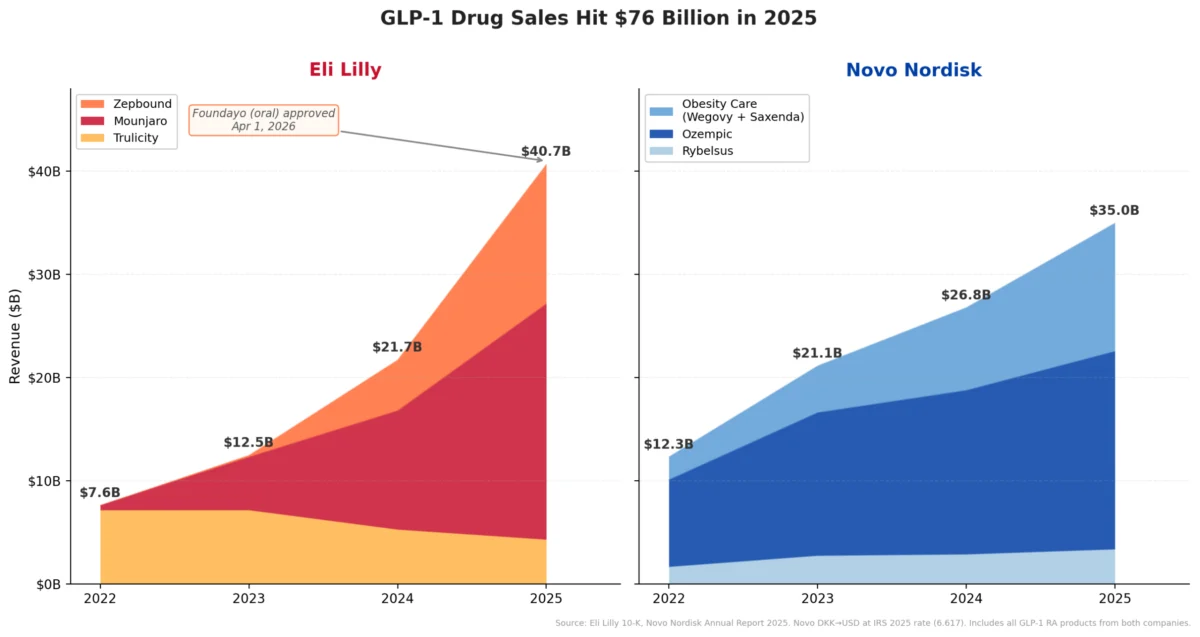

Lilly’s aggressive M&A strategy is directly enabled by the extraordinary commercial success of its tirzepatide franchise, marketed as Mounjaro for type 2 diabetes and Zepbound for chronic weight management. The company’s GLP-1 revenue surged from $7.6 billion in 2022 to an astounding $40.7 billion in 2025, marking a more than fivefold increase in just three years. This meteoric rise positioned tirzepatide as the primary driver of Lilly’s overall revenue, which reached $65.2 billion in fiscal year 2025. Of this, Mounjaro contributed an estimated $23.0 billion, and Zepbound, despite its more recent market entry, added $13.5 billion, underscoring the immense demand for these therapies.

The momentum shows no signs of abating. Lilly’s management has projected continued growth, guiding for total revenue between $80 billion and $83 billion in 2026. This optimism is further bolstered by the recent accelerated approval of Foundayo (orforglipron), Lilly’s oral GLP-1 agonist for obesity, by the FDA on April 1, 2026. The approval, granted under the National Priority Voucher program just 50 days after filing, highlights the urgency and strategic importance of this new offering. Foundayo, now shipping through LillyDirect at a competitive price point, with anticipated Medicare Part D access by July, is expected to provide an additional, highly accessible growth vector, complementing the injectable tirzepatide franchise and further solidifying Lilly’s dominance in the metabolic disease space. This robust and expanding revenue stream provides Lilly with the financial firepower and strategic flexibility to pursue ambitious acquisitions like Kelonia without immediately straining its balance sheet.

Pfizer’s Post-COVID Spending Spree: A Divergent Path

The comparison between Lilly’s current M&A activities and Pfizer’s recent deal-making spree is instructive. Pfizer, having reaped an unprecedented windfall from its COVID-19 vaccine Comirnaty and antiviral Paxlovid, embarked on a series of significant acquisitions. The most prominent of these was the $43 billion acquisition of Seagen in late 2023, a move designed to significantly bolster Pfizer’s oncology portfolio with established antibody-drug conjugate (ADC) technology and four approved medicines. Other notable deals included the $11.6 billion acquisition of Biohaven Pharmaceuticals in 2022 for its migraine drug Nurtec, and the $5.4 billion acquisition of Global Blood Therapeutics (GBT) in 2022 for its sickle cell disease drug Oxbryta.

However, Pfizer’s buying spree occurred precisely as its COVID-19 revenue was plummeting. The company’s full-year revenue collapsed by 42%, from a record $100.3 billion in 2022 to $58.5 billion in 2023. Comirnaty sales plunged by 64%, and Paxlovid sales fell by 58% during this period. This sharp decline created significant financial headwinds, even as Pfizer integrated its newly acquired assets. While the Seagen acquisition provided a much-needed boost to its oncology business, the timing meant that Pfizer was using cash from a rapidly diminishing source, leading to investor concerns about its financial leverage and future growth prospects. The company subsequently deferred share buybacks to prioritize deleveraging its balance sheet post-Seagen.

A Tale of Two Strategies: Early-Stage Innovation vs. Late-Stage Commercial Assets

The contrasting timing of their M&A strategies is not the only differentiator between Lilly and Pfizer. Their approaches to the type of assets acquired also vary significantly. Pfizer’s strategy largely focused on acquiring late-stage or already commercialized assets, such as Seagen’s approved oncology drugs, Biohaven’s Nurtec, and GBT’s Oxbryta. This "bolt-on" approach aimed to immediately diversify revenue and fill pipeline gaps with products that had a clearer path to market and existing sales. While this can provide quicker returns, it often comes with higher price tags for proven assets and carries the risk of integrating mature products into a new sales infrastructure.

Lilly, on the other hand, appears to be adopting a more "platform-centric" and earlier-stage acquisition strategy. Its recent deals, including Kelonia, reflect a willingness to invest in innovative technologies and preclinical or early-clinical stage assets that have the potential for long-term, transformative impact. Beyond Kelonia, Lilly’s deal wave includes:

- Morphic Therapeutic (2024): Acquired for approximately $3.2 billion, bringing a Phase 2 asset and a platform focused on integrin inhibitors for immunology and gastrointestinal disorders.

- Scorpion Therapeutics (2025): A collaboration valued up to $2.5 billion for precision oncology programs (Phase 1/2).

- Verve Therapeutics (2025): An investment of about $1.3 billion for gene-editing therapies (Phase 1b).

- SiteOne Therapeutics (2025): Up to $1.0 billion for a Phase 2-ready pain therapy.

- Insilico Medicine (2026): A collaboration potentially worth up to $2.75 billion for AI-originated preclinical oral therapeutics across various disease areas.

This strategy suggests Lilly is betting on foundational science and innovative platforms that could yield multiple future drug candidates, rather than just immediate revenue drivers. While this approach carries higher inherent developmental risk and longer timelines to market, it offers the potential for greater intellectual property control, differentiation, and sustained innovation over the long term. It also allows Lilly to acquire companies at an earlier valuation, potentially maximizing future returns if the technologies prove successful.

Financial Posture and Market Confidence

The financial health and investor perception of the two companies further highlight their distinct positions. As of late 2025, Lilly reported a robust cash position of $7.3 billion and strong operating cash flow of $16.8 billion, underpinned by its surging GLP-1 sales. While it carries long-term debt of $40.9 billion, this is managed against a rapidly expanding revenue base and rising margins. The market has responded enthusiastically to Lilly’s growth trajectory and strategic investments, pushing its market capitalization to an impressive $830 billion-$880 billion by April 2026, making it one of the most valuable pharmaceutical companies globally.

In contrast, Pfizer’s operating cash flow stood at $11.7 billion in FY2025, a significant decline from its peak years. The company has been focused on integrating its acquisitions and managing its balance sheet, with buybacks deferred to prioritize deleveraging post-Seagen. While Seagen is expected to contribute substantially to Pfizer’s oncology revenues in the coming years, the immediate impact of the COVID-19 revenue cliff has been a major headwind. Consequently, Pfizer’s market capitalization in April 2026 hovered around $155 billion, reflecting investor apprehension about its near-term growth and the challenges of replacing lost blockbuster revenue.

The Promise of In Vivo CAR-T and Kelonia’s Technology

Lilly’s bet on Kelonia is particularly noteworthy given the burgeoning yet challenging field of CAR-T cell therapy. Current FDA-approved CAR-T therapies, such as Kymriah (Novartis), Yescarta (Gilead), and Abecma (BMS/bluebird bio), have demonstrated remarkable efficacy in specific hematological malignancies. However, they are associated with significant logistical hurdles, including complex manufacturing processes, high costs (often exceeding $400,000 per patient), lengthy vein-to-vein times, and potential severe toxicities like cytokine release syndrome (CRS) and neurotoxicity. These factors limit their broad applicability.

Kelonia’s in vivo CAR-T approach aims to address these limitations by developing engineered lentiviral particles that can selectively deliver CAR genes to T-cells directly inside the patient’s body. This eliminates the need for apheresis, ex vivo cell processing, and lymphodepletion chemotherapy, potentially streamlining the treatment process, reducing costs, and improving safety. If successful, this technology could unlock CAR-T therapy for a much wider range of patients and potentially even for solid tumors, an area where traditional CAR-T has largely struggled. Lilly’s acquisition of Kelonia thus positions it at the forefront of a potentially disruptive innovation in oncology, promising a more accessible and scalable form of cellular immunotherapy.

Broader Implications for the Pharmaceutical Landscape

Lilly’s M&A strategy, fueled by an actively growing blockbuster franchise and focused on early-stage, platform-based innovation, presents a compelling counter-narrative to Pfizer’s experience. While both companies are leveraging significant cash flows to drive future growth, Lilly’s proactive investment in emerging technologies like in vivo CAR-T and AI-driven drug discovery platforms suggests a long-term vision for sustainable innovation rather than immediate revenue replacement. This approach, while riskier in the short term, could yield more proprietary and differentiated assets in the future.

The contrasting fortunes and strategies of Lilly and Pfizer offer valuable insights for the broader pharmaceutical industry. It underscores the critical importance of timing in M&A, the distinction between acquiring established assets versus innovative platforms, and the profound impact of a company’s core revenue trajectory on its ability to execute ambitious growth strategies. Lilly’s current deal spree, if successful in translating its early-stage bets into transformative medicines, could serve as a blueprint for how pharmaceutical companies can effectively reinvest blockbuster profits to secure future leadership in a rapidly evolving scientific landscape. As Lilly continues to report its financial results and advance its pipeline, the industry will be closely watching whether its carefully orchestrated expansion can indeed avoid the post-blockbuster pitfalls that have challenged its peers.

Leave a Reply