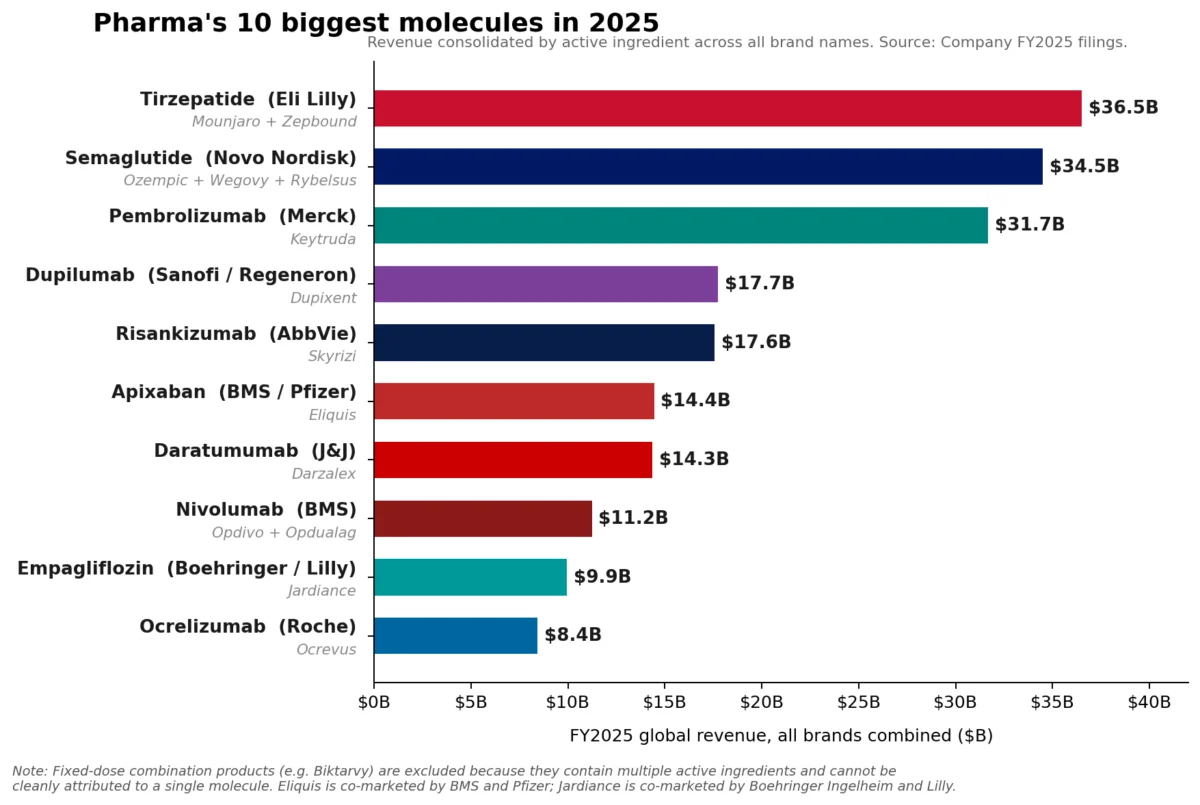

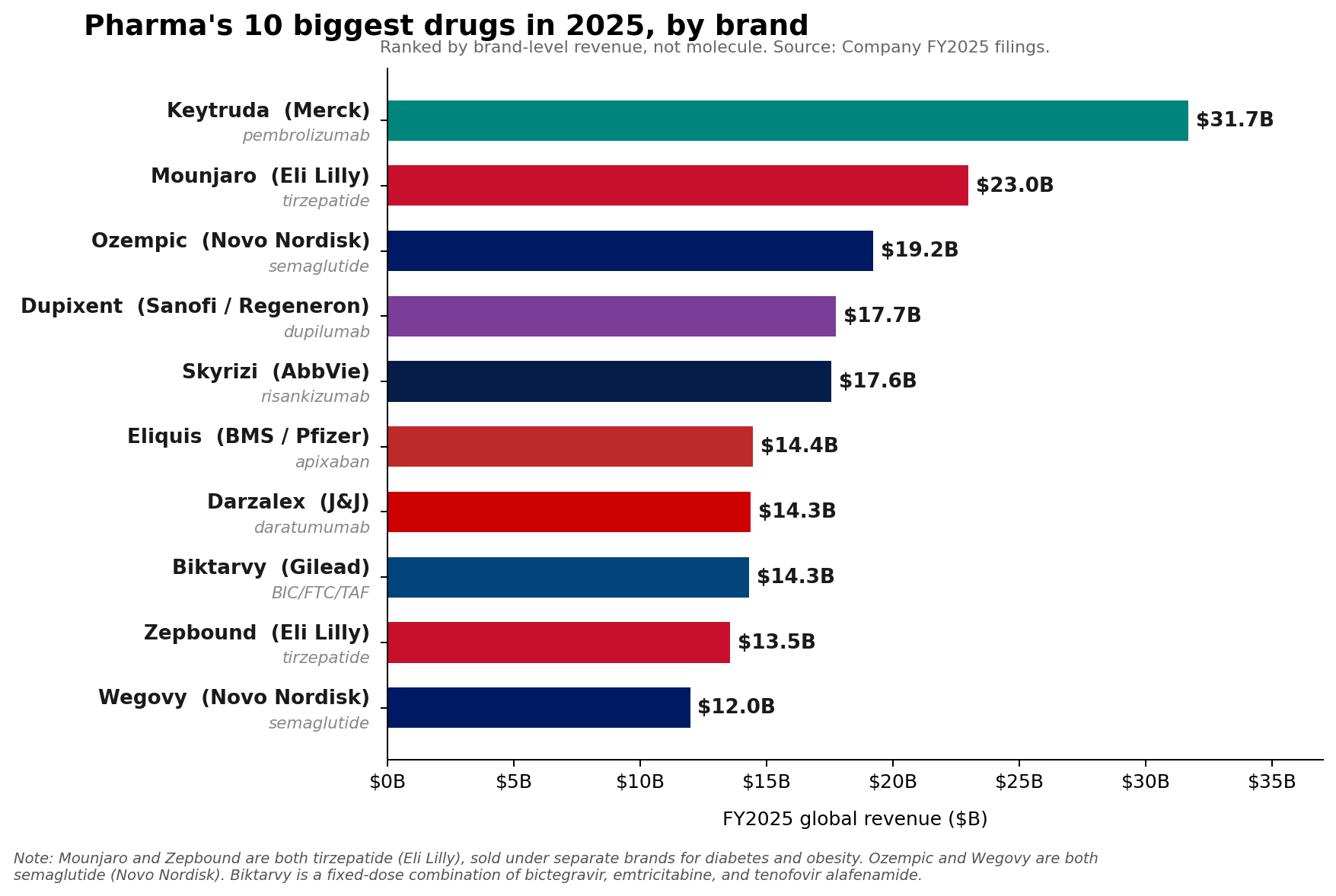

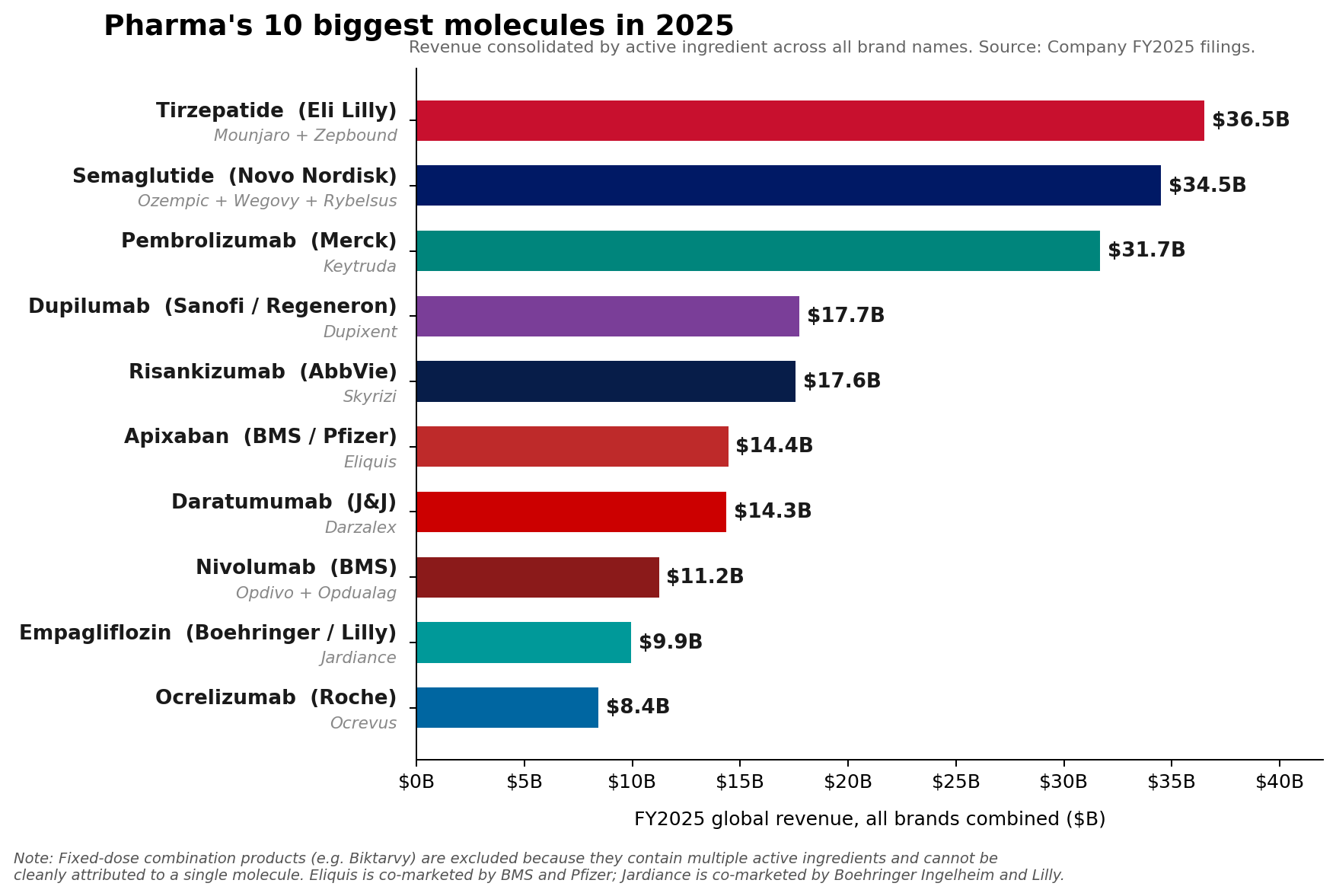

The pharmaceutical industry’s financial landscape underwent a significant reordering in fiscal year 2025, as revealed by the latest "Pharma 50" report. While Merck’s immuno-oncology blockbuster Keytruda (pembrolizumab) impressively retained its position as the world’s leading pharmaceutical brand, achieving $31.7 billion in sales, its dominance at the molecular level was eclipsed by the meteoric rise of metabolic disorder treatments. Eli Lilly’s tirzepatide franchise, comprising the diabetes medication Mounjaro and the weight-loss drug Zepbound, collectively generated approximately $36.5 billion in revenue for 2025. Similarly, Novo Nordisk’s semaglutide portfolio, encompassing Ozempic, Wegovy, and Rybelsus, posted an estimated $34.5 billion in combined sales, signaling a profound shift in the industry’s top-tier revenue drivers. This pivot underscores the escalating commercial power of GLP-1 and GIP receptor agonists, challenging the long-standing reign of oncology therapies.

Keytruda’s Enduring Strength and Approaching Horizon

Merck’s Keytruda, a programmed death receptor-1 (PD-1) blocking antibody, has been a cornerstone of cancer treatment since its initial accelerated approval by the U.S. Food and Drug Administration (FDA) in September 2014 for advanced melanoma. Its mechanism of action, which involves boosting the body’s immune response to fight cancer, has proven effective across an ever-expanding array of malignancies. In FY2025, Keytruda continued its robust growth trajectory, demonstrating a 7% increase in sales. This sustained performance is a testament to Merck’s aggressive strategy of lifecycle management and indication expansion. The company has diligently pursued new regulatory approvals, extending Keytruda’s utility to over 30 indications across various cancer types, including non-small cell lung cancer, melanoma, head and neck cancer, and renal cell carcinoma, often as a first-line treatment or in combination therapies.

A significant development in its lifecycle management is the introduction of subcutaneous Keytruda QLEX, which aims to improve patient convenience and potentially extend market exclusivity. Subcutaneous formulations reduce administration time and can be given in non-infusion settings, offering a significant advantage over traditional intravenous infusions. This strategic move is particularly crucial as Keytruda approaches its looming loss of exclusivity (LOE) in the coming years, with key patents expected to expire around 2028 in the U.S. and later in other markets. Merck CEO Rob Davis has publicly characterized this anticipated decline not as a "cliff" but as "more of a hill," suggesting the company has a diversified pipeline and strategic initiatives in place to mitigate the revenue impact. However, the market’s reaction to Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion, which fell below Wall Street expectations, indicates lingering investor concerns about the post-Keytruda era. The company’s ability to successfully transition its revenue base and pipeline assets will be closely watched by analysts and investors alike.

The Ascendancy of Metabolic Innovators: Tirzepatide and Semaglutide

The most striking development in the FY2025 rankings is the unprecedented surge of GLP-1 and GLP-1/GIP receptor agonists, fundamentally reshaping the pharmaceutical revenue hierarchy. Eli Lilly’s tirzepatide, a dual glucose-dependent insulinotropic polypeptide (GIP) and glucagon-like peptide-1 (GLP-1) receptor agonist, has emerged as a formidable challenger. Initially approved as Mounjaro for type 2 diabetes in May 2022, its superior efficacy in blood glucose control and significant weight reduction quickly propelled it to blockbuster status. Following its FDA approval for chronic weight management as Zepbound in November 2023, the drug’s commercial trajectory accelerated dramatically. In FY2025, Mounjaro alone accounted for $22.965 billion, while Zepbound contributed $13.542 billion, culminating in a combined tirzepatide franchise revenue of approximately $36.5 billion. This rapid ascent reflects the immense unmet need in the treatment of obesity and diabetes, as well as tirzepatide’s differentiated mechanism of action, which is believed to offer enhanced metabolic benefits compared to single-agonist GLP-1 therapies.

Not to be outdone, Novo Nordisk’s semaglutide franchise, a pure GLP-1 receptor agonist, also demonstrated colossal market penetration. Comprising the injectable diabetes medication Ozempic, the injectable weight-loss drug Wegovy, and the oral diabetes pill Rybelsus, the semaglutide portfolio collectively garnered an estimated $34.5 billion in FY2025. Ozempic, approved for type 2 diabetes in December 2017, laid the groundwork for the franchise’s success, followed by Wegovy’s landmark approval for chronic weight management in June 2021. Rybelsus, introduced as the first oral GLP-1 receptor agonist in September 2019, further expanded the drug’s accessibility and patient base. Novo Nordisk has been a pioneer in the GLP-1 space, and its sustained investment in semaglutide’s development and market expansion has solidified its position as a dominant player in metabolic health. The competitive dynamic between Lilly’s tirzepatide and Novo Nordisk’s semaglutide is a defining feature of the contemporary pharmaceutical landscape, driving innovation and market growth in an area of immense global health burden.

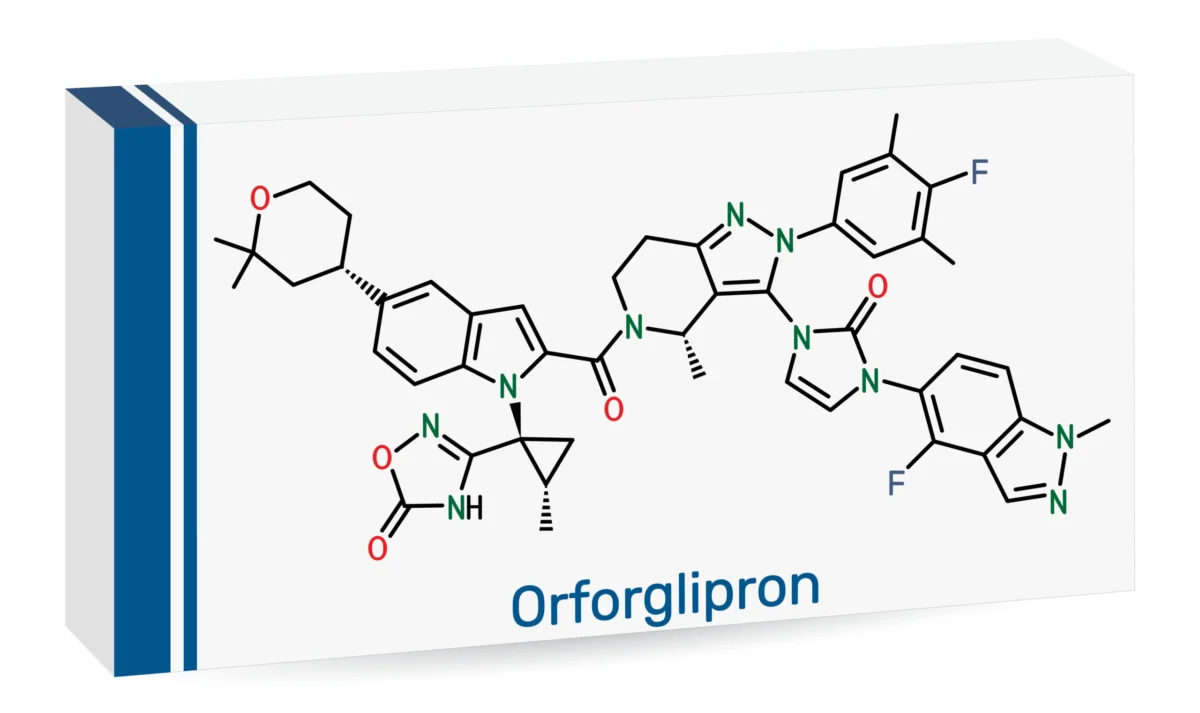

The Oral Revolution: Orforglipron as a Game Changer

The competitive landscape in the obesity market is poised for further disruption with the introduction of new therapeutic modalities. A significant "wildcard" for 2026 and beyond is Eli Lilly’s Foundayo (orforglipron), a once-daily oral small-molecule GLP-1 receptor agonist. Lilly’s journey with orforglipron began with a licensing agreement with Japan’s Chugai Pharmaceutical in 2018, recognizing the potential of an orally bioavailable GLP-1. The drug received a pivotal FDA approval on April 1, 2026, for chronic weight management, marking a crucial milestone as it became commercially available as of April 9, 2026. This approval, landing after the first quarter of 2026 concluded, positions orforglipron as a major strategic factor for the remainder of the year and beyond, though its absolute revenue contribution in 2026 might not immediately surpass its injectable counterparts.

Analysts hold varied opinions on orforglipron’s immediate revenue potential. While Lilly’s robust FY2026 revenue guidance of $80 billion to $83 billion largely rides on the continued momentum of Mounjaro and Zepbound, orforglipron introduces a new dimension. The convenience of an oral pill, eliminating the need for injections, has the potential to significantly broaden the patient population accessing GLP-1 therapies, particularly those hesitant about injectable medications. Mounjaro, with a 2025 base of $22.965 billion, and Zepbound, with $13.542 billion, are already established at blockbuster scale. Orforglipron, despite its strategic importance and ability to "widen the funnel" of GLP-1 users, will need time to build its sales base.

The broader context for orforglipron’s launch is a rapidly expanding anti-obesity pipeline. According to Citeline’s 2026 Pharma R&D Annual Review, the anti-obesity pipeline witnessed an astonishing 30.7% jump to 588 active compounds, a "gut-busting" expansion against a backdrop of overall pipeline contraction in other therapeutic areas. This intense competition underscores both the vast market opportunity and the challenge for new entrants to differentiate themselves. Orforglipron’s oral formulation provides a clear advantage, but it enters a market already dominated by Lilly’s own highly effective injectable products and Novo Nordisk’s semaglutide.

Similarly, Novo Nordisk is advancing its oral semaglutide offerings. While the older Rybelsus saw a 2% decline at constant exchange rates (CER) in 2025, the company launched the newer Wegovy pill in January 2026, with its impact already factored into Novo’s 2026 outlook. Novo Nordisk also plans a broader rollout of Wegovy and the introduction of a 7.2 mg dose in various countries, alongside the recent launch of Wegovy HD in the U.S. Despite these strategic moves, Novo Nordisk’s own 2026 guidance projects adjusted sales growth of negative 5% to negative 13% at CER, reflecting pricing pressure, increased competition, and U.S. access dynamics. This suggests that while oral semaglutide is strategically vital for market expansion and patient preference, it may not be the primary driver of absolute revenue growth for Novo Nordisk in the immediate future, with the injectable formulations continuing to lead sales.

Beyond Metabolic: The Resilient Power of Immunologics and Oncology

While the GLP-1/GIP agonists commanded the spotlight, other specialty brands demonstrated remarkable growth and sustained commercial power, ensuring that the pharmaceutical leaderboard remains diverse. The immunology market, in particular, proved to be a robust engine of growth. AbbVie’s immunology portfolio, anchored by Skyrizi (risankizumab) and Rinvoq (upadacitinib), showed exceptional performance. Skyrizi, an interleukin-23 (IL-23) inhibitor used for psoriatic arthritis, Crohn’s disease, and psoriasis, reached an impressive $17.562 billion in sales in 2025. Rinvoq, a Janus kinase (JAK) inhibitor approved for conditions such as rheumatoid arthritis, psoriatic arthritis, and ulcerative colitis, achieved $8.304 billion. Together, these two drugs generated $25.866 billion in 2025, constituting roughly 42% of AbbVie’s total net revenue of $61.160 billion for the year. This signifies that AbbVie has successfully cultivated a two-drug immunology engine that, by itself, is nearing the scale of the industry’s largest individual brands, mitigating some of the revenue impact from the biosimilar erosion of its long-standing blockbuster, Humira.

Sanofi’s Dupixent (dupilumab), a monoclonal antibody that inhibits the signaling of interleukin-4 (IL-4) and interleukin-13 (IL-13), continued its strong upward trajectory, rising to €15.714 billion (approximately $17 billion USD at prevailing exchange rates) in 2025. Dupixent’s broad utility across atopic dermatitis, asthma, chronic rhinosinusitis with nasal polyps, and eosinophilic esophagitis highlights the value of multi-indication specialty drugs in chronic inflammatory diseases. Novartis’s Kisqali (ribociclib), a cyclin-dependent kinase 4/6 (CDK4/6) inhibitor for breast cancer, climbed an impressive 58% to $4.783 billion, showcasing the continued demand for innovative oncology treatments. Johnson & Johnson also reported significant growth in its Innovative Medicine sector, driven primarily by products like Darzalex (daratumumab) for multiple myeloma and Tremfya (guselkumab) for psoriatic arthritis and psoriasis, further solidifying the strength of immunology and oncology franchises.

This commercial picture is reinforced by broader R&D trends. Citeline’s 2026 R&D review indicated that immunologicals were one of the few large therapeutic areas that continued to expand, with their pipeline count rising by 20.6% even as the overall pharmaceutical pipeline experienced a slight dip. This demonstrates sustained investment and innovation in immunology, suggesting a durable market for these therapies. Thus, while GLP-1s are rapidly ascending, the leaderboard below Keytruda is not becoming a "pure GLP-1 monoculture." Instead, it is becoming increasingly crowded with large, resilient franchises in immunology and oncology that continue to compound their growth through new indications, expanded patient access, and ongoing R&D.

Strategic Implications for the Pharmaceutical Industry

The shifts observed in FY2025 carry significant strategic implications for the global pharmaceutical industry. The rapid rise of metabolic drugs, particularly GLP-1 and GIP agonists, signals a paradigm shift where chronic conditions like obesity and type 2 diabetes are becoming primary revenue drivers, rivaling and even surpassing traditional strongholds like oncology in terms of molecular-level sales. This necessitates a re-evaluation of R&D priorities, market access strategies, and commercial models for many pharmaceutical companies. The sheer scale of the patient populations suffering from obesity and diabetes ensures a vast market, but also invites intense competition and pricing pressures.

For established players like Merck, the challenge lies in diversifying its portfolio and developing new blockbusters to offset the inevitable revenue decline from Keytruda’s loss of exclusivity. Its investment in a robust pipeline and strategic lifecycle management for existing assets is crucial. For Lilly and Novo Nordisk, the imperative is to manage explosive growth, ensure manufacturing capacity, navigate evolving reimbursement landscapes, and fend off new competitors entering the burgeoning obesity and diabetes markets. The success of oral formulations like orforglipron and oral semaglutide could dramatically expand market penetration, but also presents new challenges in patient adherence, pricing, and distribution.

Beyond the metabolic revolution, the sustained growth of immunology and oncology demonstrates the enduring value of precision medicines and targeted therapies in complex diseases. Companies like AbbVie, Sanofi, Novartis, and Johnson & Johnson are proving that focused investment in these areas, coupled with strong lifecycle management, can build incredibly resilient and high-performing franchises. The overall contraction in the pharmaceutical R&D pipeline, juxtaposed with targeted growth in specific therapeutic areas like anti-obesity and immunologicals, suggests a more concentrated and perhaps more efficient allocation of research resources. The industry is moving towards a future where multi-billion-dollar therapeutic areas are not singular, but rather a constellation of powerful franchises addressing critical unmet medical needs across diverse disease states. The FY2025 results are a powerful indicator of this dynamic and evolving pharmaceutical landscape.

Leave a Reply