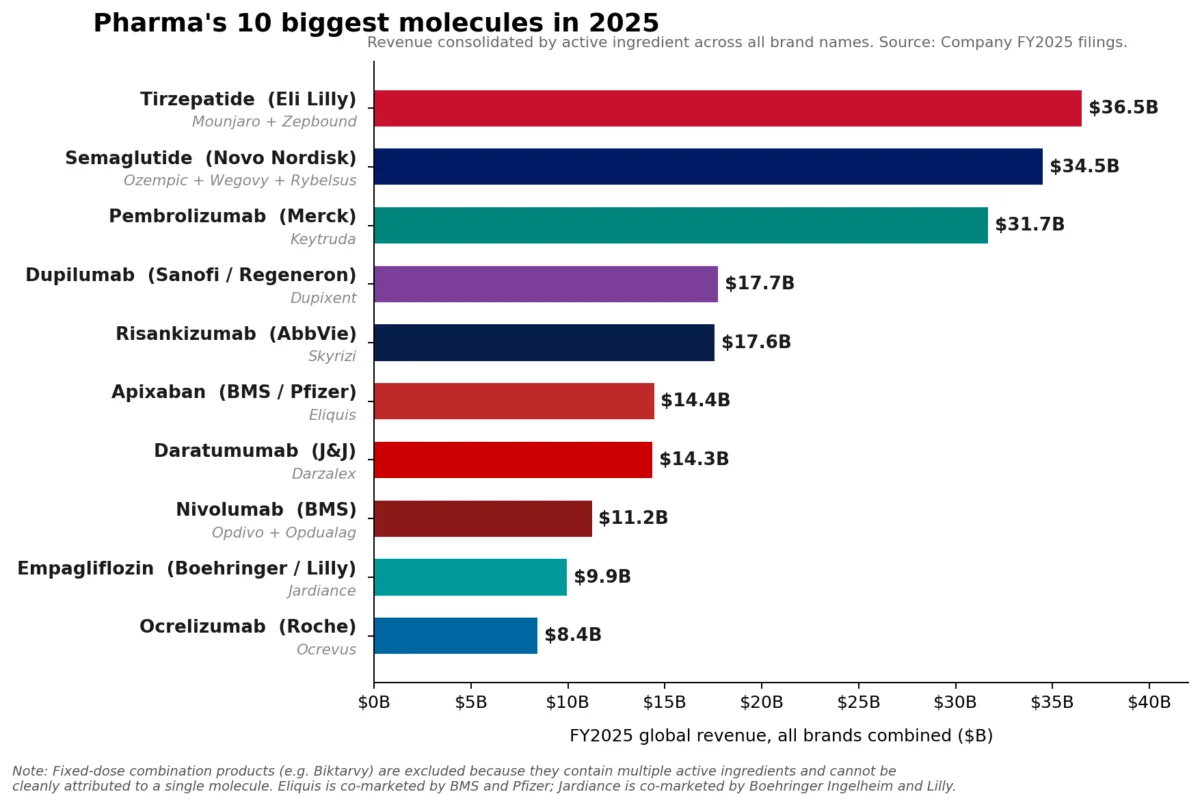

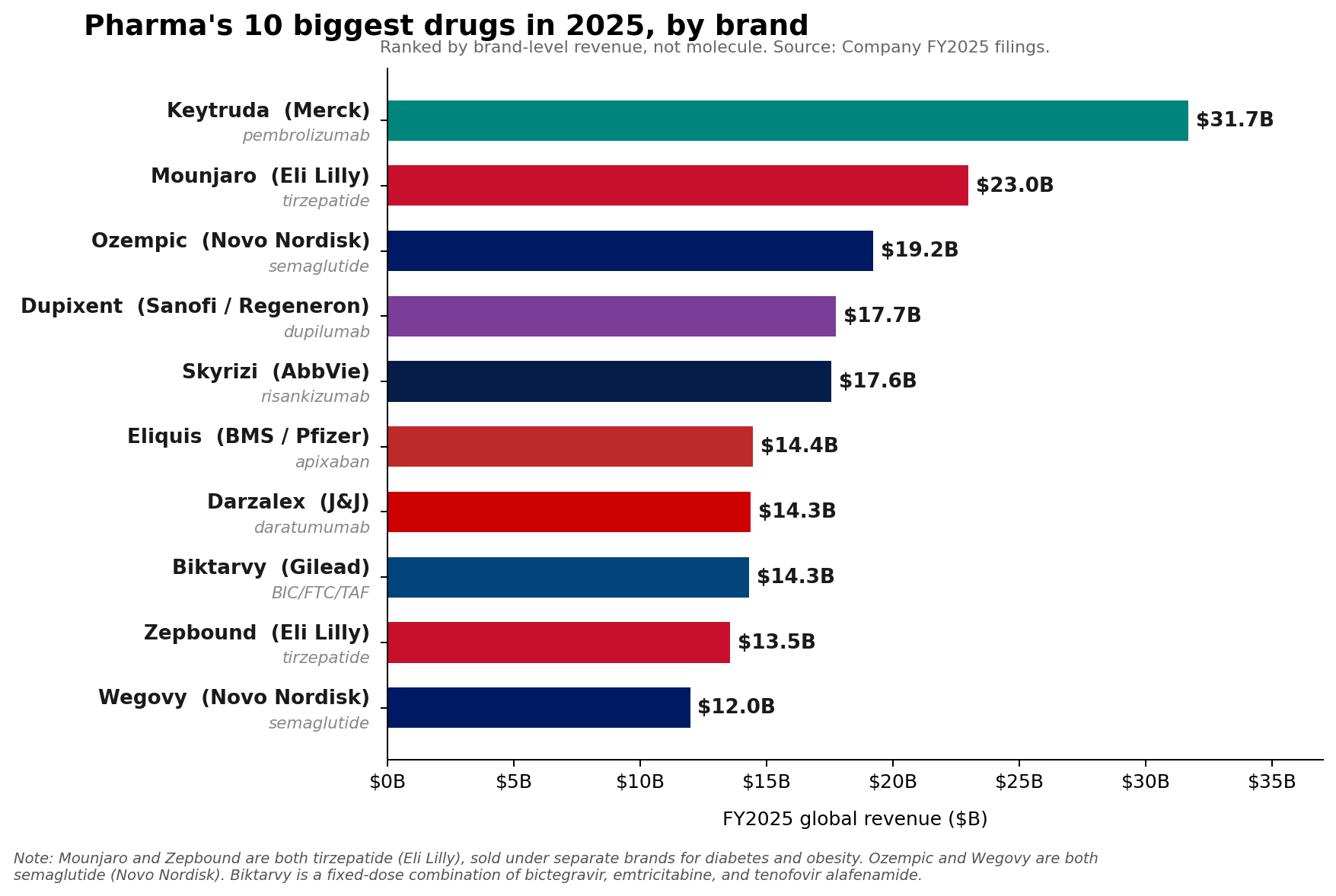

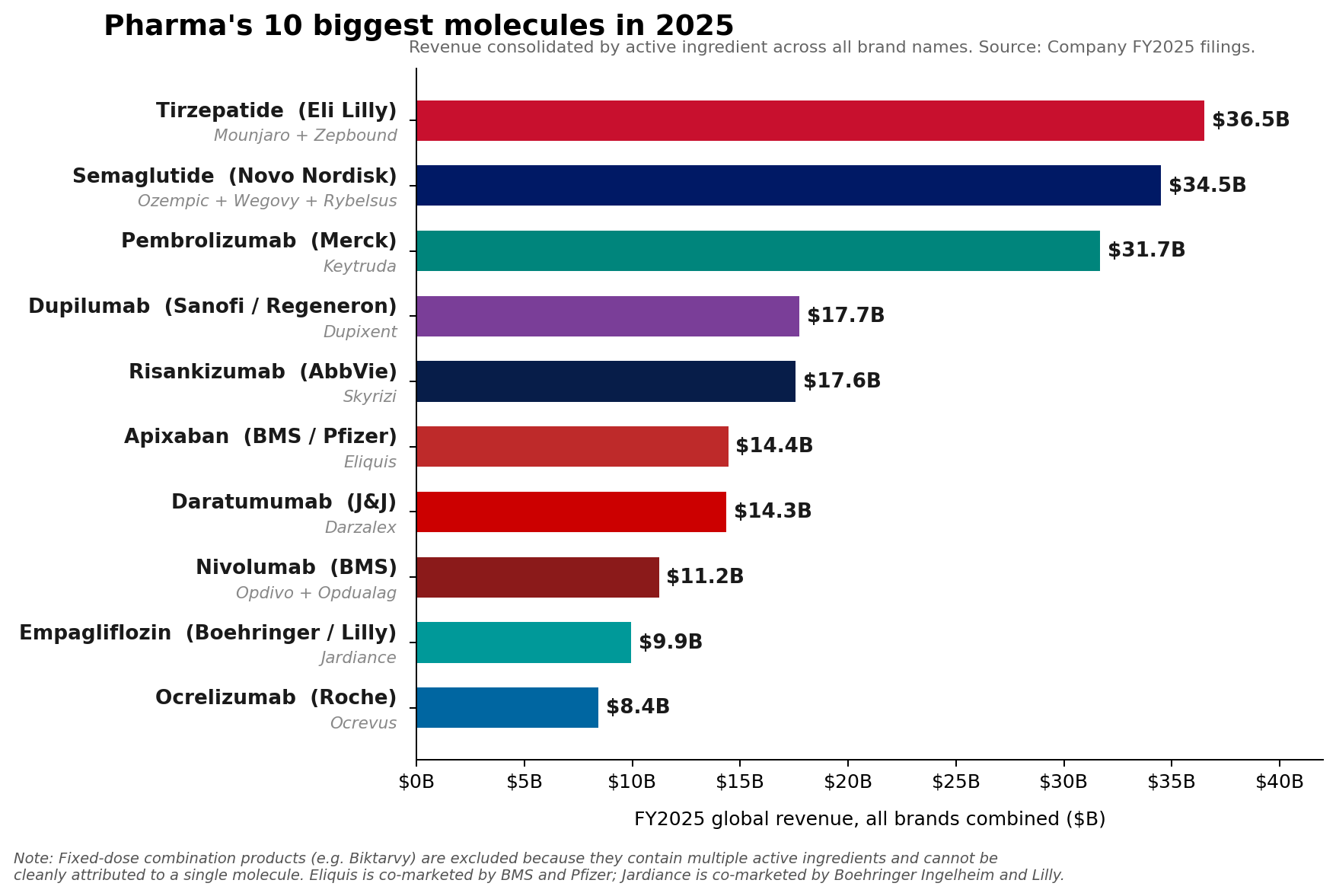

Merck’s immunotherapy blockbuster, Keytruda (pembrolizumab), maintained its dominant position as the pharmaceutical industry’s leading brand in Fiscal Year 2025, recording an impressive $31.7 billion in sales. This figure underscores Keytruda’s continued, albeit slowing, growth and its critical role in Merck’s portfolio. However, a significant shift has occurred at the molecular level, signaling a new era in pharmaceutical revenue generation. The combined sales of Eli Lilly’s tirzepatide franchise—encompassing Mounjaro for diabetes and Zepbound for weight loss—surpassed Keytruda, reaching approximately $36.5 billion in 2025. Similarly, Novo Nordisk’s semaglutide franchise, comprising Ozempic, Wegovy, and Rybelsus, collectively generated roughly $34.5 billion, also exceeding Keytruda’s molecular sales. This marks a pivotal moment, as the burgeoning market for metabolic disease treatments begins to redefine the pharmaceutical industry’s top-earning molecules.

Keytruda’s Enduring Brand Strength Amidst Shifting Tides

Keytruda’s achievement of $31.7 billion in sales in FY2025 represents a robust 7% growth compared to the previous year. This performance solidifies its status as a cornerstone of modern oncology, having revolutionized cancer treatment across numerous indications. Since its initial FDA approval in September 2014 for advanced melanoma, pembrolizumab, a programmed cell death protein 1 (PD-1) inhibitor, has expanded its therapeutic reach to over 30 indications, including lung cancer, head and neck cancer, classical Hodgkin lymphoma, and renal cell carcinoma. This broad utility and efficacy in activating the immune system against cancer cells have been central to its commercial success.

Merck has proactively sought to extend Keytruda’s lifecycle and commercial viability, investing heavily in research and development to secure new indications and innovative formulations. One such strategic move is the development of subcutaneous Keytruda QLEX, designed to offer a more convenient administration method for patients. This effort is particularly critical as the industry looks towards Keytruda’s impending loss of exclusivity (LOE) in the coming years, a phenomenon often referred to as the "patent cliff." Merck CEO Rob Davis has publicly addressed this challenge, characterizing the anticipated revenue drop-off as "more of a hill than a cliff," suggesting a belief in the company’s ability to manage the transition through portfolio diversification and continued innovation.

Despite Keytruda’s impressive sales, Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion reportedly fell below Wall Street expectations. This cautious outlook likely reflects the broader competitive landscape, the impending LOE for its flagship product, and the significant investments required to develop new revenue streams. The pharmaceutical giant is actively working to build a pipeline that can absorb the impact of Keytruda’s eventual patent expiration, focusing on areas like cardiovascular disease and oncology with new modalities.

The Ascendance of GLP-1 Receptor Agonists: A Metabolic Revolution

The narrative of FY2025 is unmistakably shaped by the meteoric rise of GLP-1 receptor agonists, particularly Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide. These molecules have not only transformed the treatment landscape for type 2 diabetes but have also ignited an unprecedented global demand in the anti-obesity market.

Tirzepatide, a dual GIP (glucose-dependent insulinotropic polypeptide) and GLP-1 receptor agonist, has demonstrated superior efficacy in both glycemic control and weight reduction. Lilly’s Mounjaro, initially approved for type 2 diabetes in May 2022, rapidly became a commercial success. Its subsequent approval for chronic weight management as Zepbound in November 2023 further amplified its market potential. In FY2025, Mounjaro alone generated $22.965 billion, while Zepbound, despite its more recent launch, contributed a remarkable $13.542 billion. The combined $36.5 billion for tirzepatide represents a staggering market penetration and underscores the immense unmet need in obesity treatment.

Similarly, Novo Nordisk’s semaglutide, a GLP-1 receptor agonist, has carved out a substantial market presence across its various brand formulations. Ozempic, approved for type 2 diabetes, and Wegovy, specifically for chronic weight management, have become household names. Rybelsus, the oral formulation of semaglutide for diabetes, offers an alternative for patients preferring pills over injections. Together, these brands propelled the semaglutide franchise to approximately $34.5 billion in revenue in 2025. Novo Nordisk has been a pioneer in the GLP-1 space, and the continued expansion of semaglutide’s indications and formulations has allowed it to capitalize significantly on the growing demand.

The success of these molecules is rooted in their mechanism of action: they mimic the effects of natural incretin hormones, stimulating insulin release, suppressing glucagon secretion, slowing gastric emptying, and promoting satiety, leading to improved glycemic control and substantial weight loss. The societal burden of obesity and related metabolic disorders has created a fertile ground for these therapies, driving unprecedented sales figures and prompting massive investments in related R&D.

Orforglipron: Lilly’s Oral Wildcard and the Future of Obesity Treatment

The competitive landscape in the obesity market is intensifying rapidly, and Eli Lilly is positioning itself to further dominate with innovative offerings. A significant strategic move came on April 1, 2026, with the FDA approval of Foundayo (orforglipron), Lilly’s once-daily oral small-molecule GLP-1 receptor agonist. Foundayo, initially licensed from Chugai in 2018, became commercially available as early as April 9, 2026, marking a pivotal moment in the convenience of obesity treatment.

The introduction of an effective oral GLP-1 offers a distinct advantage in patient accessibility and preference, potentially broadening the market significantly beyond injectable therapies. While analysts hold differing views on its immediate revenue impact for 2026, its strategic importance is undeniable. Lilly’s own guidance for 2026 revenue, projected at $80 billion to $83 billion, reflects strong confidence in its overall portfolio, heavily driven by the continued growth of Mounjaro and Zepbound. As Foundayo’s approval came after the close of Q1 2026, its financial contributions will primarily manifest in the latter half of the year.

Despite Mounjaro and Zepbound starting 2026 with substantial sales bases of $22.965 billion and $13.542 billion respectively from 2025, Foundayo represents a strategic long-term play. It targets a segment of the market that may be hesitant to adopt injectable therapies, potentially expanding the overall pool of patients seeking medical weight loss solutions. Citeline’s 2026 Pharma R&D Annual Review highlights the fervent activity in this space, noting that the anti-obesity pipeline surged by a "gut-busting 30.7%" to 588 active compounds, even as the overall pharmaceutical pipeline experienced a contraction. This robust R&D pipeline underscores the industry’s belief in the sustained growth of the obesity market and the fierce competition for novel, more convenient therapies. Orforglipron, while entering behind Lilly’s already blockbuster injectable products, is a testament to this strategic push for market diversification and enhanced patient options.

Novo Nordisk is also active in the oral GLP-1 space, with its oral semaglutide formulation, Rybelsus, already on the market for type 2 diabetes. More recently, the company launched the new Wegovy pill in January 2026, aiming to capitalize on the convenience factor for weight loss. Novo Nordisk expects a broader rollout of Wegovy and the introduction of a 7.2 mg dose in various countries throughout 2026, alongside the recent launch of Wegovy HD in the U.S. However, Novo Nordisk’s own 2026 guidance for adjusted sales growth is a more modest negative 5% to negative 13% at constant exchange rates (CER). This forecast reflects anticipated pricing pressures, increased competition from new entrants like Lilly’s orforglipron, and complex U.S. market access dynamics. While oral semaglutide is strategically important for widening market access and patient choice, it does not yet appear poised to be the primary driver of Novo Nordisk’s absolute revenue growth in 2026, which will likely still be dominated by the injectable forms of semaglutide.

Beyond GLP-1s: The Enduring Power of Immunology and Oncology Franchises

While the spotlight is firmly on GLP-1s, the pharmaceutical landscape is far from a "monoculture." Other scaled specialty brands in immunology and oncology continue to demonstrate remarkable growth and remain critical revenue drivers for their respective companies. These therapeutic areas, characterized by high unmet needs and complex disease mechanisms, continue to attract significant investment and innovation.

AbbVie, for instance, has successfully navigated the post-Humira era by building a formidable immunology engine with Skyrizi (risankizumab) and Rinvoq (upadacitinib). In 2025, Skyrizi, approved for plaque psoriasis, psoriatic arthritis, and Crohn’s disease, reached an impressive $17.562 billion in sales. Rinvoq, indicated for rheumatoid arthritis, psoriatic arthritis, atopic dermatitis, and ulcerative colitis, achieved $8.304 billion. Together, these two drugs generated $25.866 billion in 2025, accounting for approximately 42% of AbbVie’s total net revenue of $61.160 billion for the year. AbbVie’s 2026 adjusted EPS guidance of $14.37 to $14.57 underscores the continued confidence in these growth drivers, positioning them as an immunology powerhouse comparable in scale to the industry’s largest single brands.

Sanofi’s Dupixent (dupilumab), a blockbuster biologic for atopic dermatitis, asthma, and chronic rhinosinusitis with nasal polyps, continued its upward trajectory, rising to €15.714 billion (approximately $17 billion USD based on average 2025 exchange rates) in 2025. This sustained growth highlights the increasing understanding and effective targeting of underlying inflammatory pathways in a range of immunological conditions.

In oncology, Novartis’s Kisqali (ribociclib), a CDK4/6 inhibitor for breast cancer, climbed a remarkable 58% to reach $4.783 billion in sales. This significant growth reflects its expanding use and strong clinical profile in the competitive breast cancer market. Johnson & Johnson also reported robust 2025 Innovative Medicine growth, primarily driven by key products such as Darzalex (daratumumab) for multiple myeloma and Tremfya (guselkumab) for psoriatic arthritis and plaque psoriasis.

Citeline’s 2026 R&D review reinforces this commercial picture, noting that immunologicals were among the few large therapeutic areas that continued to expand their pipeline, rising by 20.6% even as the overall pipeline count dipped. This indicates ongoing innovation and market potential in immunology. These figures collectively demonstrate that the leaderboard below Keytruda is not succumbing to a "GLP-1 monoculture" but is instead becoming more crowded with large, durable franchises in immunology and oncology that are still compounding their growth.

Broader Implications for the Pharmaceutical Industry

The shifts observed in FY2025 carry profound implications for the pharmaceutical industry. The dethroning of oncology’s leading molecule by metabolic therapies signals a significant reorientation of R&D investment and commercial focus. The sheer scale of the obesity and diabetes markets, coupled with the proven efficacy of GLP-1s, suggests that these molecules will continue to drive substantial revenue for years to come.

For companies like Merck, the looming patent cliff for Keytruda necessitates aggressive pipeline development and strategic acquisitions to mitigate future revenue loss. Their ability to transition smoothly from a reliance on a single blockbuster to a diversified portfolio will be a key determinant of long-term success. The "hill not a cliff" strategy implies a phased approach, leveraging existing indications and new formulations while simultaneously nurturing emerging assets.

The rapid entry and commercial availability of oral GLP-1s like orforglipron and the new Wegovy pill underscore the industry’s commitment to patient convenience and market expansion. While injectables have paved the way, oral formulations have the potential to unlock new patient populations and disrupt established market dynamics, presenting both opportunities and competitive pressures. The race for differentiated oral therapies, along with next-generation injectables, will define the future of metabolic disease treatment.

Furthermore, the sustained growth of immunology and specialized oncology drugs highlights the enduring value of innovation in areas with high unmet needs. These complex conditions often require highly targeted, high-cost therapies, ensuring their continued commercial viability. The pharmaceutical industry is demonstrating its ability to simultaneously pursue multiple blockbuster categories, adapting to evolving scientific understanding and patient needs. The future of pharma appears to be one of dynamic competition, rapid innovation, and a diverse array of therapeutic breakthroughs.

Leave a Reply